Here’s my snapshot on global markets for Aussie investors – including my Top 5 factors moving markets.

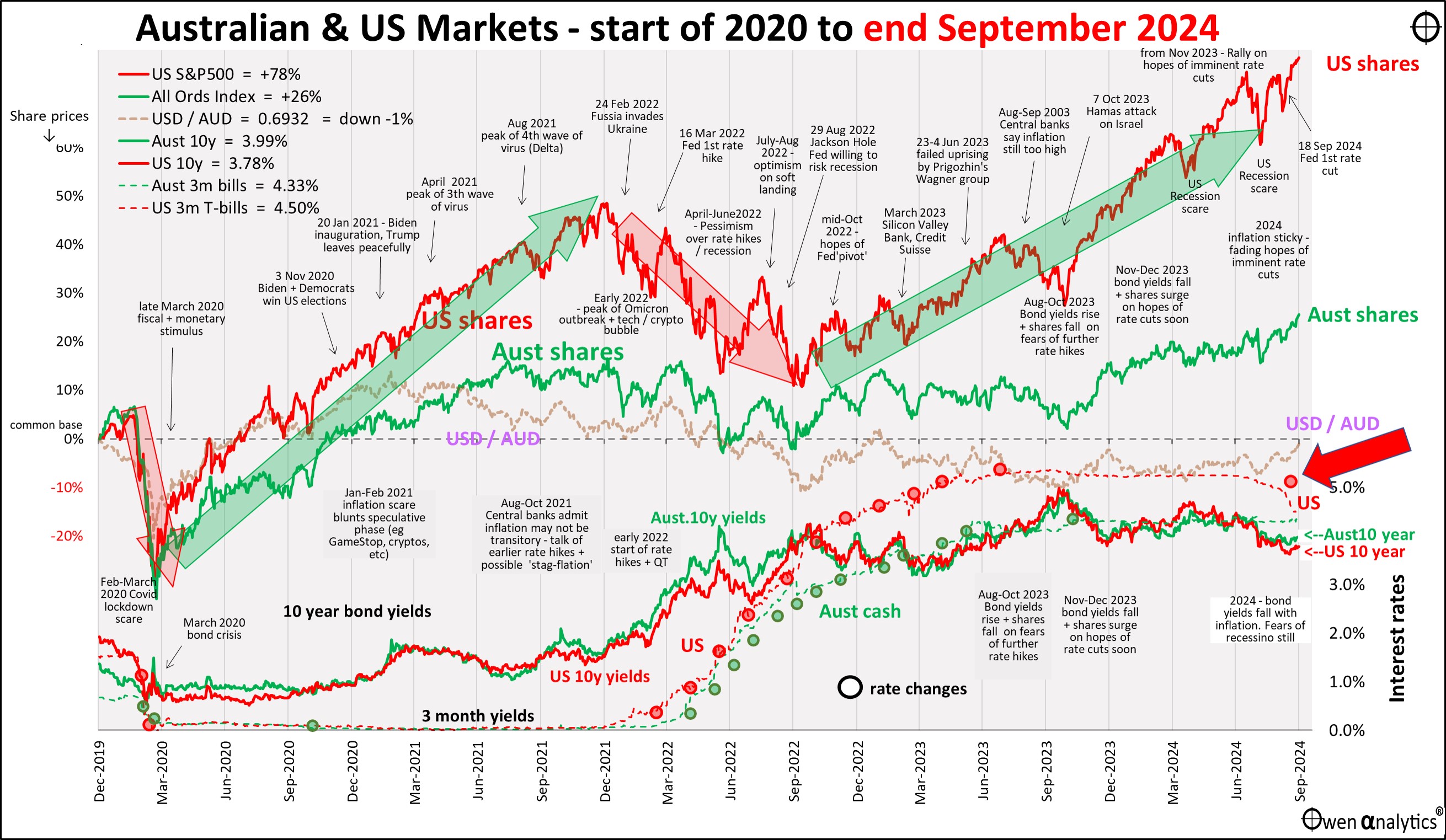

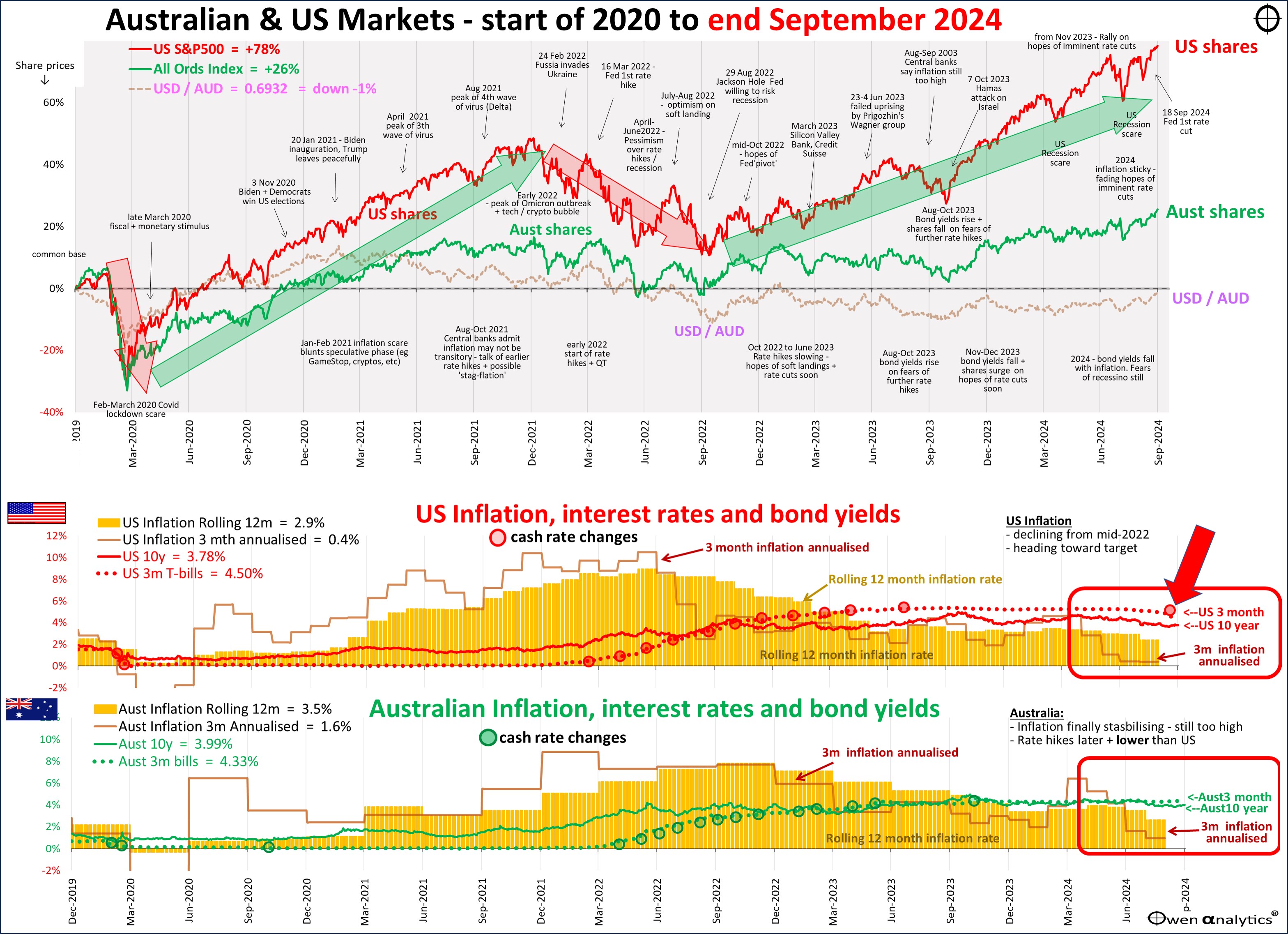

First - my essential 1-page snapshot chart - covering Australian and US share markets, short and long-term interest rates, inflation, and the AUD/USD exchange rate.

There are two versions – first is the traditional version on a single chart:

Also the alternate version below, requested and used by several advisers - showing inflation in the lower sections -

Here are my Top 5 factors moving investment markets in September:

1. US Fed’s first rate cut and inflation

The first was the US Federal Reserve’s much anticipated first interest rate cut – a half of one percent cut in the Fed Funds rate, from a range of 5.25 to 5.5%, to a range of 4.75% to 5% (The Fed as adopted a ‘range’ target since the ‘global financial crisis’ in 2008). This was the first Fed rate cut since the depths of the Covid lockdown recession in March 2020, when rates were cut to zero.

What allowed the Fed to cut rates was US inflation continuing to fall back toward its 2% target. US annual inflation for August came in at 2.4% (down from 2.9% for July). More importantly, the annualised 3-month inflation rate was just 0.4% (highlighted in the red box in the US inflation chart above). The monthly rate for August was zero.

A mild slowing US economy and rising unemployment (from 3.4% in January 2023 to 4.2% in August 2024) have effectively brought price inflation to a near-halt, giving the Fed leeway to start cutting interest rates. Although money markets are still pricing in several more rate cuts in the coming month, Fed chair Powell at the end of the month said he was in no hurry for further cuts at the moment.

While global share markets were bullish on the news of the Fed rate cut, I was not so positive. For my story on the history of rate cut cycles (and rate hike cycles) and their impacts on US shares, see:

The Fed rate cut lifted global share markets by an overall average of 2% for the month. US stocks were ahead by 2%, where the US tech giants were up only modestly.

The exception was Tesla, up +22%, after the US government announced an import ban on Chinese made internet-enabled EVs, which ironically will mostly affect Tesla’s Chinese made EVs. Tesla’s price rebound merely brought its share prices back to around square for the year, and still down 30% from its 2021 peak. (Oracle, apparently re-born as an ‘ai’ stock, was also up 20%).

The star share market in September was China/Hong Kong, but that was because of the second factor -

2. Chinese stimulus reboot at last

The second major event affecting global markets in September was the belated and somewhat muted stimulus announcements from the Chinese government in the last week of the month. There were a range of measures including cuts to lending rates, cuts to bank reserve ratios, a boost to bank lending to ailing property developers, loosening of housing deposit requirements, and even loosening of restrictions on second home ownership (one of Xi Jinping’s long-held signature policies – ‘Housing should be for living, not for speculation!’).

Xi has been reluctant to support the ailing property / construction / finance market. Instead he has been trying to re-direct the engine of China’s economic growth away from construction and toward high-tech export industries like EVs, batteries, solar panels, and wind generators.

These are gathering steam but are not yet large enough to offset the severe negative domestic impacts of the property / construction collapse, which has been driving deflation in prices, wages, and jobs. The problem is not a lack of money, it is depressed consumer confidence, which is being manifest in declining wages, rising unemployment, and social unrest.

Will the latest stimulus measures be enough? Probably not. Will Xi need to do more? Probably yes, despite him seeing it as a diversion from his main aims.

For a snapshot of China’s all-important steel production and construction industry, see:

In any event, the announcements were enough to lift Chinese share markets by around 20%, including heavyweights Meituan +45%, Alibaba +35%, Tencent +16%, Baidu +14%. It seems global investors are now piling back into Chinese shares.

Australian shares – rotation from banks to miners

The Chinese stimulus announcements gave an immediate boost to commodities prices, which in turn boosted the local share market. As a result, the ASX market was one of the better ‘developed world’ markets in September, climbing 2% to new highs. The All Ordinaries index is now 2% ahead of its previous all-time high posted on 1st August of this year, and up 9% so far in 2024. Not bad, but well behind the US market (S&P500 up 21% this year).

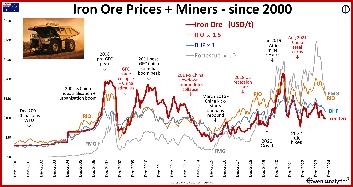

By far the most important commodity for the overall ASX market is iron ore, and iron ore futures jumped 15% at the end of the month (but is still only half its mid-2021 peak price).

This lifted share prices for the big-3 iron ore miners: BHP was up +8% for the month, RIO up +16%, and FMG up +13%. These share price gains sound good, but they are all still down for the year to date: BHP down -9%, RIO -5%, FMG -29%.

For my story on the close relationship between our big-3 miners, iron ore prices, and the Chinese boom-bust cycle, see:

Outside of the big-3 miners (all driven by iron ore prices), most other miners were also stronger, for two main reasons. The first is the fact that the Chinese stimulus announcement lifted battery metals prices (copper, nickel, lithium), which lifted stocks like S32 (+20%), Pilbara Minerals (+10%), Min Resources (+30%). It has been a very long wait for a rebound, and this may be the catalyst, although on fundamentals, supply still outstrips demand.

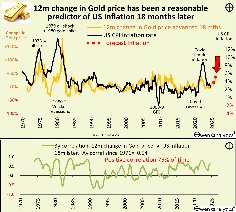

The second reason was the completely unrelated continued rise in gold prices, which lifted gold stocks almost across the board. On rising gold prices – see:

Offsetting the rise in gold miners was the ongoing slide in fossil fuel producers, as oil prices continued to decline on weak outlooks for US and European growth.

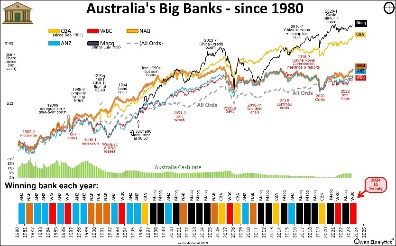

Australian bank shares

On the other side of the banks -v- miners see-saw in September were the big banks, which took an over-due breather.

CBA ended the month down -3%, NAB down -1%, with WBC and ANZ more or less flat. Mind you, they are all still up strongly for the year for no apparent reason: WBC up +38% for the year, CBA +21%, NAB +22% and ANZ +18%. (I say ‘for no apparent reason’ since earnings and dividends for the big-4 retail banks peaked a decade ago, and that’s before inflation.)

Macquarie was up the strongest of the big banks in September: +8% (and up +26% for the year), after adding to its growing collection of fines and penalties for a variety of illegal activities.

For my rundown on the performance of the big banks (including Macquarie) – see:

Retail cartel

The other big story that moved the local market in September was in the big oligopoly retail cartel - Woolworths (down -7%) and Coles (down -4%), as the regulator was finally stirred into action by a bewildering array of price gouging examples. (Hint: a ‘discount’ sign in Woollies and Coles is code for an under-handed mark-UP.)

For a run-down of the recent rather ordinary half-year ASX reporting season, see my last monthly snapshot -

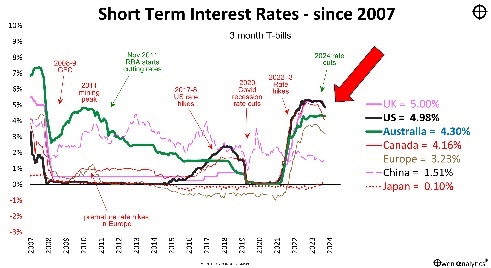

3. RBA’s hands still tied on rate cuts

In Australia, the inflation picture is not as good. The RBA’s rate hikes to tackle inflation were later, slower, and lower than in the US and other countries. The result is that inflation is still a problem here, so no local rate cuts yet. Adding fuel to the fire we have strong jobs and wages growth, driven by federal and state government spending sprees.

August annual inflation for Australia came in at 2.7% pa, but this was artificially depressed by some tricky sleight of hand by Federal and State governments with their temporary power bill subsides. Inflation will jump back up again when the temporary subsidies expire, and the RBA has said specifically that it is not fooled by such political trickery.

Despite money markets, local economists and commentators continually predicting imminent and multiple rate cuts here, I have been saying for a couple of years that the RBA was not going to be able to follow the rate cuts by central banks in other countries any time soon – see:

4. Labor Government re-opening ‘negative gearing’ reform

One significant development for one million Aussie investors was the Labor government re-opening the controversial debate on a possible winding back of tax concessions on negative gearing on investment properties. Some 2.2 million individuals own rental properties in Australia, of which one million claim rental losses that reduce their taxes on other income.

Various governments in recent decades have tried (or promised) to wind back the tax benefits of negative gearing, but all attempts have failed to date. This one will impact a lot more people than the proposed new tax on unrealised gains on SMSFs over $3m.

5. Escalation and widening of wars

Worryingly, there has also been an escalation and widening of the wars in the Middle East and also in Ukraine. For investors, the main impacts are likely to be on commodities prices (feeding ultimately into inflation). Thus far, oil prices have continued to drift down due to ample supply and weakening US and European growth outlooks.

While not directly impacting investment markets, the US presidential race continues to fascinate. It appears Kamala Harris has maintained the momentum she initially gained on being handed the Democratic nomination in August. There has been little in the way of further policy promises from either side.

A second Trump term would probably see more tax cuts, more tariff hikes, more subsidies for local manufacturing, and less international engagement and funding/participation in foreign wars.

Harris is less of a known quantity. She has given little away on policies, but appears to have some long held ambitions to increase social spending, control grocery prices, and raise taxes. Trump cut the main corporate tax rate from 35% to 21% in his last term and has promised to cut it further to 15%, while Harris has promised to increase it to 28%)

Both sides appear to have completely abandoned any pretence of fiscal responsibility, so we can expect more huge budget deficits and government debt issuance in the coming years, plus escalating trade protectionism and industry subsidies, regardless of whom is in the White House.

The other big factor in the mix will be which side controls the House and Senate.

November 5 is closing in. I am not buying nor selling anything, nor changing investment strategy based on what might happen in November. However I will be in New England and New York for the week before the election, to get a first-hand feel for sentiment on the ground.

For my current views on asset classes and asset allocations - see:

‘Till next time – happy investing!