My first story in this series My ’10-4 all-weather’ ETF portfolio – Intro (25 Jun 2024), outlined the background, rationale, and role of my ’10-4 all-weather ETF portfolio’.

It’s my long-term diversified ETF-based portfolio aimed at generating moderate returns, with low costs, low maintenance, an acceptable level of volatility, but minimal risk of permanent loss of capital.

It has three specific and measurable long-term goals:

-

- a total return target of 10% pa after taxes and fees, averaged over 10 years,

- an income target of 4% average (as part of the 10% total returns),

- and a volatility limit (setbacks no deeper or longer than the All Ords).

Today’s story is part 2 – what is actually in the portfolio.

But first - a few very important warnings!

It is NOT a list of ‘best’ ETFs.

It is NOT a ranking of best to worst, or top 10, or top 30.

There is no ‘best’ ETF for all purposes. Nor is there a 'best' set of ETFs for all purposes.

Do NOT buy one or more of these ETFs just because they are on my list.

Everyone has different circumstances, needs, and goals, and mine are probably very different to most readers.

In particular, the volatility is probably higher than most people can tolerate. It is only part of my overall assets, and I don’t use this to meet any specific capital or income goals or needs, although it does have an income target (but that is a risk control measure, not an income need).

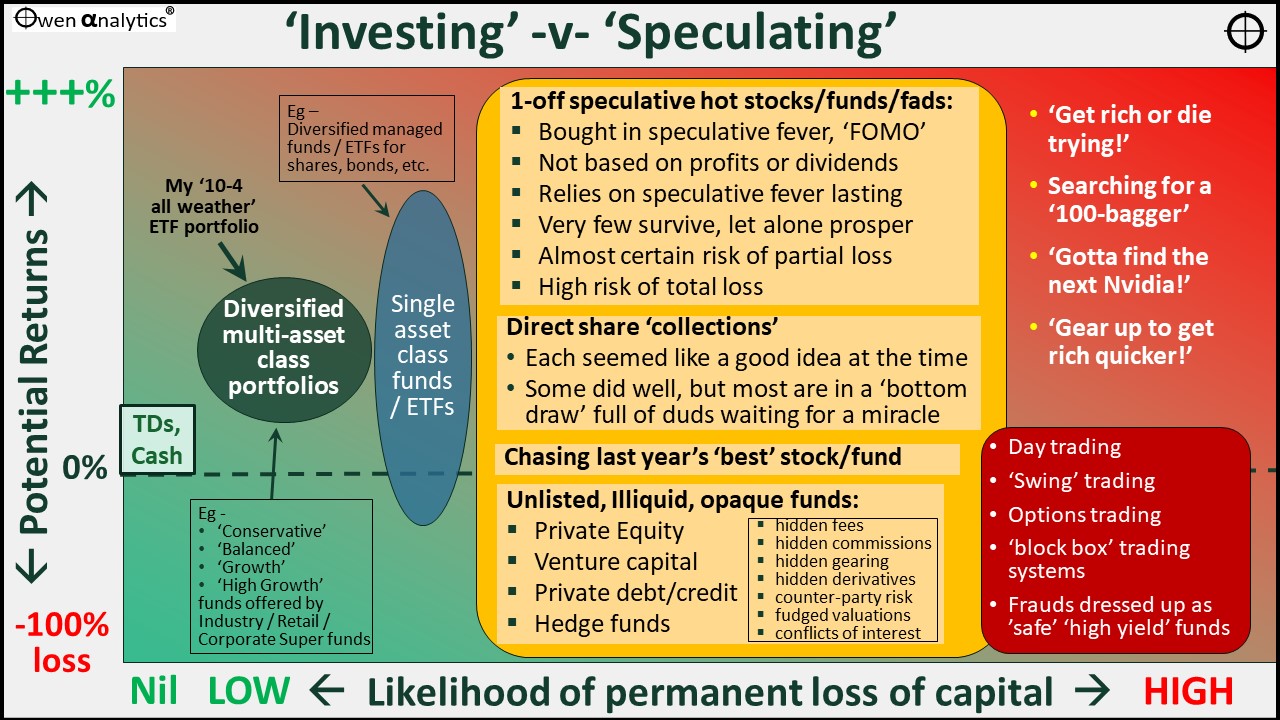

ETFs are like bricks or Lego blocks

ETFs are NOT the magic pill solutions they are often made out to be.

ETFs are like bricks to an architect, or Lego blocks. By themselves they are just bricks. Using exactly the same bricks, you can build an award-winning masterpiece, or you can also build an engineering disaster.

It’s not about the bricks, it’s about how you put different types of bricks together to create a portfolio that does what you want it to do.

There is no ‘best brick’ or ‘best ETF’ for all purposes.

How many ETFs?

Of the 348 ETFs listed on the ASX, I have only approved 30 for use in the portfolio, and I am currently using just nine to get all the exposures I want at the moment, across Australian and global asset classes.

(The first story in the series outlined how I whittled the list down from 348 to 30).

Team sport

This portfolio is run like a team sport. I have several players in the full squad (30 ‘approved’ ETFs at present). From these, I select which players I want to use in what conditions (9 are on in the field at the moment, ie in the portfolio), and the rest are ‘on the bench’.

No one strategy (ETF) or combination of strategies (ETFs) is a ‘one-size-fits-all’ solution for all conditions. Different strategies (ETFs) behave differently in different conditions. When conditions change fundamentally, I make adjustments, to the weights and to the ETFs.

I would never use them all on the field at the same time (too many, and some work against each other). Nor would I ever use just one.

For example - no matter how good Sam Kerr or Pat Dangerfield are in their chosen sports, they could not possibly take on an entire opposition side single-handedly. (Ok maybe those two could, and 'Danger' in a wheelchair could probably beat Collingwood on a good day, but you get the point!)

It takes a team – an optimal combination of strategies (ETFs) to suit the particular set of challenges at hand.

Of the 30 ETFs currently approved in the squad, at any one point in time I would probably use no more than a dozen, and no less than around half a dozen.

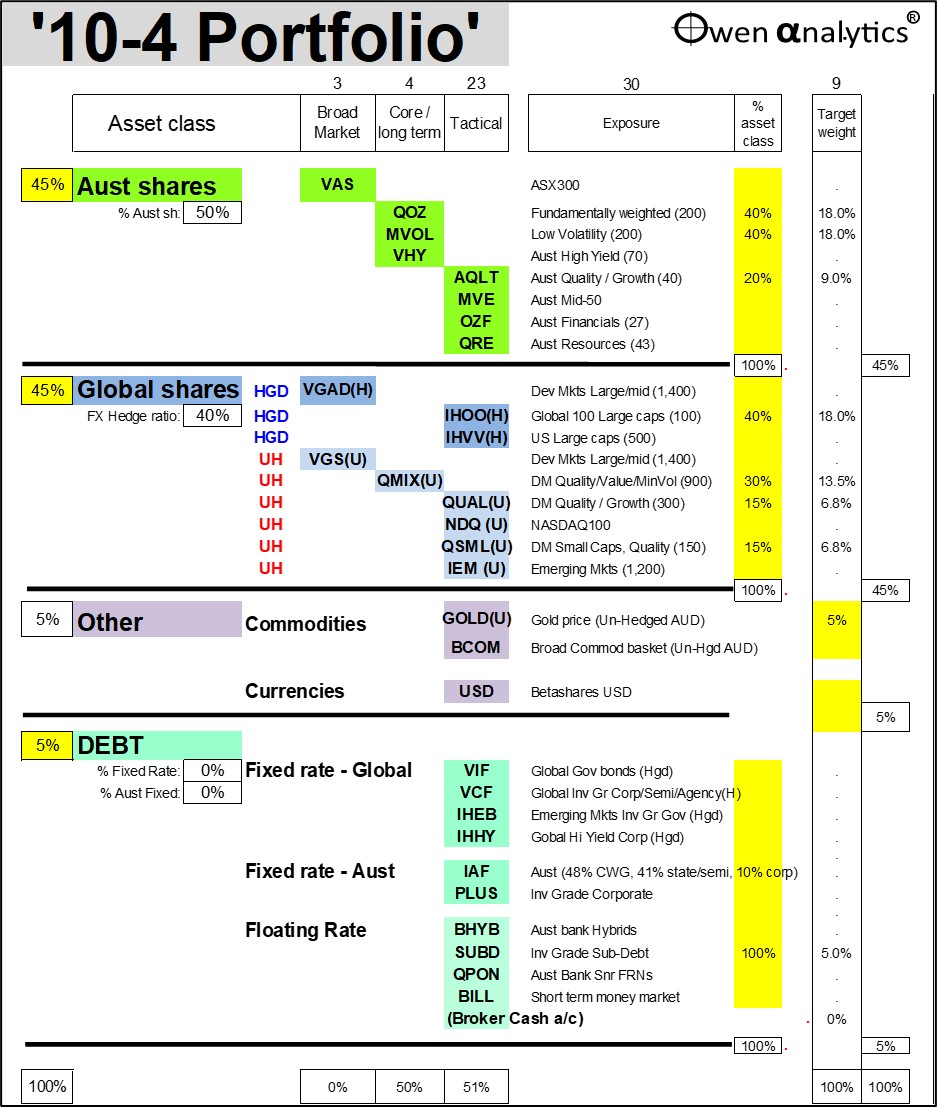

Approved ETFs and the portfolio structure

Here are the 30 ETFs in the current squad – organised into four main asset classes (Australian Shares, Global Shares, ‘Other’, and Debt).

The ETFs are also organised into three categories (columns) – what I call ‘Broad Market’, ‘Core/long-term’, and ‘Tactical’ (more on this below).

The current target weights are in the far-right column. The ‘Exposure’ column briefly describes the strategy for each ETF, with the approximate number of underlying holdings in brackets.

Three categories of approved ETFs - for three different purposes

The 30 ETFs in the ‘approved’ squad fall into one of three categories:

‘Broad market’ ETFs

These cost-effectively cover their whole asset class.

I would be happy to hold these long-term through cycles as my only exposure to that particular asset class (although I adjust their weights from time to time depending on market conditions, and I may switch to a better and/or lower cost broad market ETF for that asset class if one comes along).

There are 3 ‘broad market’ ETFs in the squad, but none in play (in the portfolio) at present.

‘Core / long-term’ ETFs

These do not aim to cover their whole asset class, but adopt a specific strategy within the asset class.

I use them to increase portfolio yield, with minimal negative impact on total returns, cyclicality, or volatility, and I accept that their return patterns will be different from their broad asset class.

I would be happy to hold these long-term through cycles (although I adjust their weights depending on market conditions, and I may switch to a better and/or lower cost ETF for that strategy if one comes along).

There are 4 ‘core/long-term’ ETFs in the squad, of which I am using three at present.

‘Tactical’ ETFs

These also do not aim to cover their whole asset class, but focus on a specific strategy, sector, or segment within their asset class.

These are not long-term holds through cycles. I use these from time to time depending on market conditions to increase total returns, with accepted consequences of lower yield, higher volatility, and greater cyclicality.

Their returns can be significantly higher or lower than their overall asset class, depending on timing. Timing is critical, based on market conditions/outlooks.

There are 23 ‘Tactical’ ETFs in the squad, of which I am using five at present.

(NB. These are just my classifications. Each investor will have their own views on which ETFs and how/when to use them.)

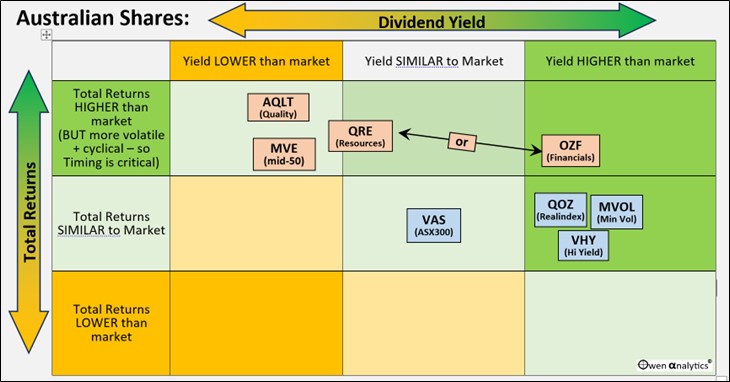

Australian Shares –

There are 8 ETFs in the squad. There is one ‘Broad Market’ ETF (VAS), three ‘Core/long-term” ETFs, and 4 ‘Tactical’ ETFs. Currently I am using 2 of the Core/long-term ETFs and one ‘Tactical’.

The main drivers of returns within the asset class are:

-

- asset class weight in overall portfolio (especially Australia -v- global)

- mix of sectors (essentially banks -v- miners), size (large/mid/small)

- different strategies (eg. 'growth', 'value', 'quality', 'minimum volatility', 'fundamental weighting', etc).

Here's the game plan for Australian shares -

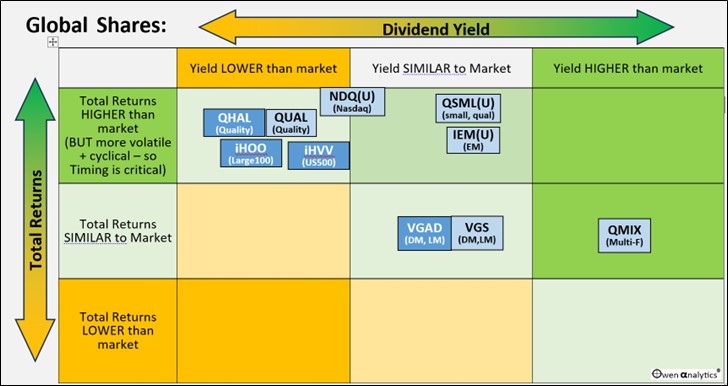

Global shares –

There are more ETFs in the squad here because it is a much larger and more complex asset class.

There are two main sub-asset classes – ‘Hedged’ and ‘Un-hedged’ (indicated by the H or U after the ETF name). Hedged and Un-hedged shares behave very differently, so I regard them almost as two separate asset classes, and there is a ‘broad market’ ETF for each (although neither is in use currently).

The main drivers of returns within the asset class are:

-

- asset class weight in overall portfolio

- mix of hedged -v- un-hedged (ie the FX ‘hedge ratio’)

- mix of 'developed/emerging' markets, regions, countries, sectors, size, strategies

Here's the game plan for global shares:

Debt -

There are 10 ETFs (plus the residual cash in the broker cash account). I regard them all as ‘Tactical’ because I regard none of these as core long-term holdings in this long-term 10-4 portfolio (ie this is not a ‘balanced’ portfolio).

(What I call the ‘Debt’ asset class is often labelled ‘Fixed Income’ or ‘Bonds’, or ‘Defensive’. The problem is that many of the things that are found in this asset class are not ‘fixed’, not ‘bonds’, and not ‘defensive’.

But they are all forms of contractual debt (with contractual obligations to pay principal and interest), so I call them ‘Debt’, as opposed to shares, which are ‘Equities’.)

The main drivers of returns within the asset class are:

-

- asset class weight in overall portfolio – in particular when I want to be ‘defensive’ in the debt/equity mix

- mix of fixed rate -v- floating rate

- mix of government/credit, Aust/global, credit grade

‘Other’ asset class -

I only have three ETFs in the squad, and one is in with 5% weight at the moment.

I do not have separate asset classes for things like ‘REITs’ or ‘Infrastructure’. They are just subsets of share markets.

There are also no unlisted assets like private equity, private credit, venture capital, etc - as this portfolio is only for liquid ETFs that hold primarily liquid assets.

NB – active management/‘alpha’ is not a major driver of returns. In this portfolio I ignore potential value-add from active funds and just use low-cost ‘passive’ ETFs.

It’s not about the ETFs

You can see from the above that it's not about the ETFs, it's about the game plan - ie the strategy - how and when to use different ETFs in what conditions.

The ETFs by themselves are not ‘all-weather’. Nor is the current combination of ETFs. What is ‘all-weather’ is the game plan, the portfolio strategy. The ETFs are just pawns in the game plan.

I could use different ETFs to execute the game plan, but the current squad is what I am using at present.

For example, instead of VAS I could use A200 or IOZ or STW, which are all quite similar but not as broad as VAS. This is not a 'recommendation' or 'advice' to use VAS, just a statement of fact that it happens to be useful in my game plan at the moment.

The actual ETFs themselves are not that important. They are just bricks after all. But it is certainly good to have a large range to use these days - a lot more than when I started out building and writing about ETF-based portfolios 20 years ago, and their fees have come down dramatically.

NB - I select ETFs not just on lowest fees. I also take into consideration their operations, speed of paying distributions, how they handle FX, quality/speed of customer service, AMIT/tax statements, which index they use, and other factors.

Frequency of changes?

This is not a ‘trading’ portfolio. Nor is it ‘set & forget’. I am fairly lazy. Generally, I only adjust portfolios once or twice per year at the most, when there is a significant change in conditions.

Sometimes I retain the same allocation for two or three years without making any changes. The aim is for a low-maintenance, low-hassle portfolio. Most of the adjustments are usually just re-investing the distributions, and regular re-balancing of holdings back to their target weights.

I do not sweat over the portfolio values or performance every day or week or month. The process I use for my roles on Investment Committees is for quarterly reviews of all asset classes and holdings. In most quarters, I recommend no changes, but there are occasions when changes are needed.

Current views in current portfolio

From a quick look at the current portfolio, some obvious features stand out:

-

- There are no fixed rate bonds (I have avoided fixed for the past three years, preferring high grade floating rate debt instead).

-

- There is an even mix of Australian -v- Global shares (global has the US tech growth story, but Australia is better value and is likely to fall less when the tech bubble deflates).

-

- 40% FX hedge ratio on global shares.

-

- There is an allocation to GOLD (gold in un-hedged AUD).

I cover these themes in more detail in other stories.

Fairly boring – as promised!

You will notice that there are no ETFs chasing hot themes like renewables, battery metals, rare earths, ‘a.i.’, crypto, and so on.

Therefore it will not double or treble my money in a year or two or three. Nor will it run the risk of blowing up. It is designed to just be there, and keep delivering on its stated goals, decade after decade. That is its role.

Many advisers will recognise several of these ETFs that I have been using for many years in portfolios (although there are some new ones I have added as costs have come down, and the range has broadened).

People will look at the portfolio and say: ‘Is that it? Any 10 year old with a broker account could to that!’

Well, that’s exactly the whole point!

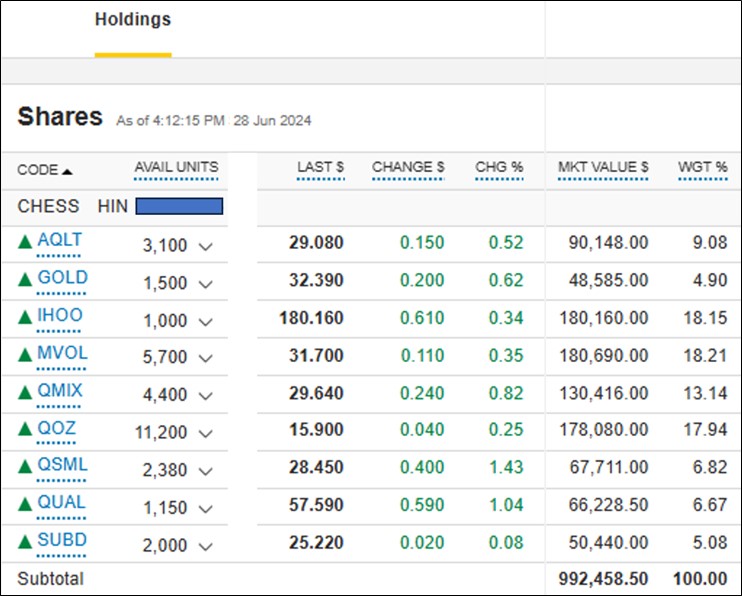

Online broker account

The online broker account is rather mechanical and doesn’t show my structure or strategy or categories like my table above. It's just an alphabetical list of holdings, the current values and weights.

This is how it looked at the end of June 2024:

The total is less than $1m because there is residual cash in the linked cash account. Also, one of the ETFs (QMIX) went ‘ex-’ before June 30, so the cash comes in July.

Apart from that, the actual portfolio weights (right column) are more or less in line with current target weights in my main table above.

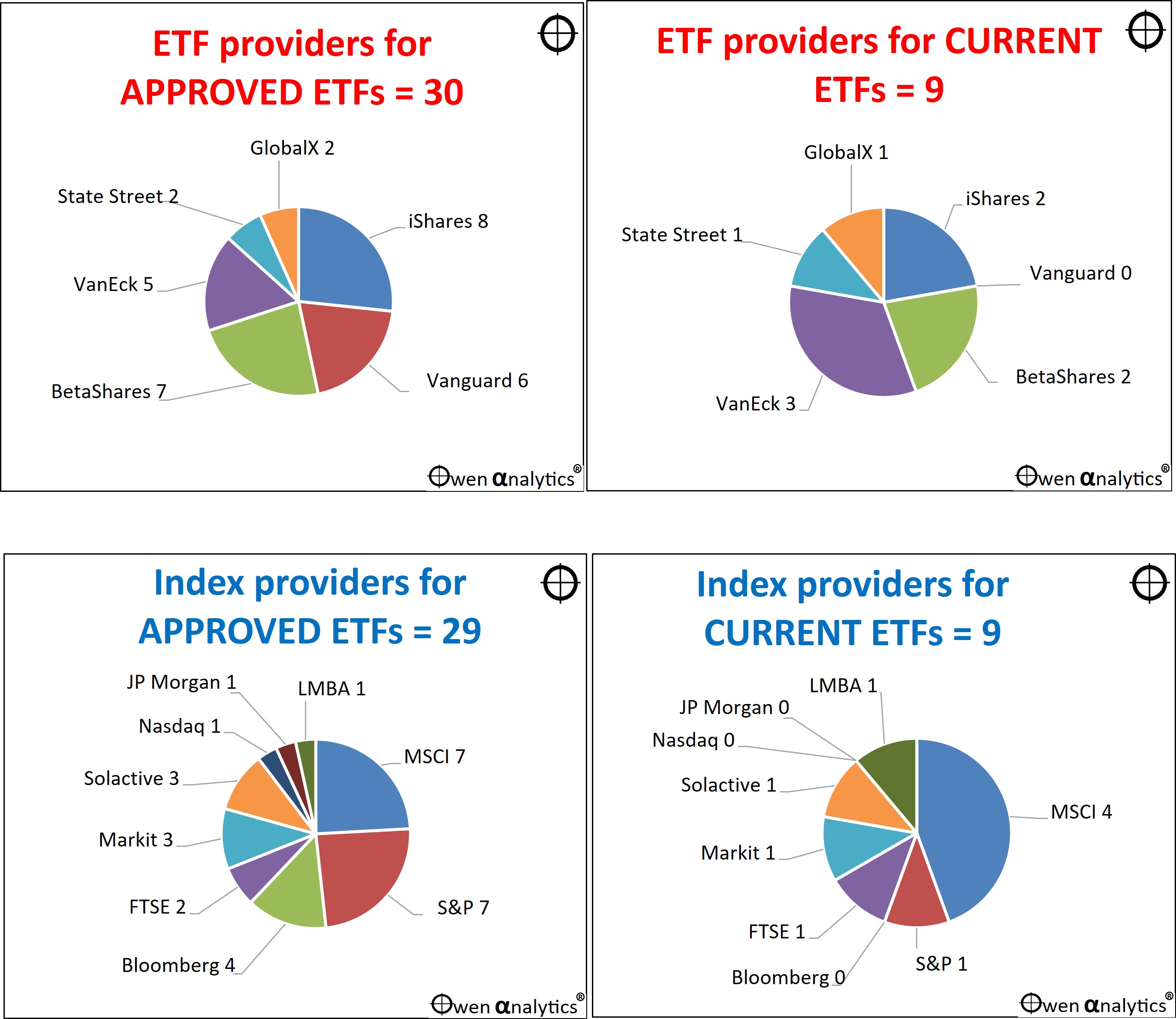

ETF houses and Index houses

For completeness, here is a breakdown of ETF providers and index providers for my approved and current ETFs (because I know I will receive a lot of emails from ETF providers and index providers).

(There are only 29 index providers because 'USD' uses just the USD/AUD FX rate.)

There is no grand plan here. This is just the way it turned out, based on my selection process.

I have no allegiances and receive no benefits from any ETF provider or index provider.

That’s it! – but please remember that this is NOT FINANCIAL ADVICE!

It is just my current portfolio for my specific circumstances, needs, goals, and risk tolerance – so it is for me and only me (and my beneficiaries).

Over the past twenty years, I have built and run ETF portfolios (and active fund portfolios for that matter) for to suit a host of different sets of goals, needs, purposes, and risk tolerances - from perpetual charities to grandkids.

The particular portfolio strategy outlined in this story is just one specific portfolio for one specific set of goals and constraints. With the ever-expending range of ETFs available, you can build a portfolio to suit any given set of goals and constraints, from the most conservative to the most aggressive.

I am not expressing any opinions about anything. I am just stating facts about actual holdings in a specific portfolio.

Readers should seek their own advice for their own individual circumstances, needs, goals, and risk tolerance.

Also remember that this portfolio is not static. I add/switch ETFs in the squad from time to time, and I also make changes to portfolios as conditions change.

Here is a link to the first story in this series – explaining the rationale, its role, and where it fits into my overall plan:

· My ’10-4 all-weather’ ETF portfolio – Intro (25 Jun 2024)

‘Till next time – happy investing!

Thank you for your time – please send me feedback and/or ideas for future editions!