Key points:

- Many or most retirees live more frugally than necessary, and die with as much Super as they had at retirement. One possible reason may be a rising fear that the current government age pension system is not sustainable. They don’t trust it to be there for life.

- Despite our aging population, Australia is probably best placed of any country in the world to maintain its government age pension system. Fears of its demise are probably over-done.

- However, it is probably inevitable that the current age pension, and/or the generous tax-breaks and benefits that go with it, will need to be scaled back or limited in future.

- If you want to build welfare dependence, bank on receiving the government pension and take the risk that it may be scaled back in future. On the other hand, if you want to build financial independence, base your plans on not having to rely on the generosity of future over-burdened taxpayers.

Unquestioned assumption that the age pension will always be there

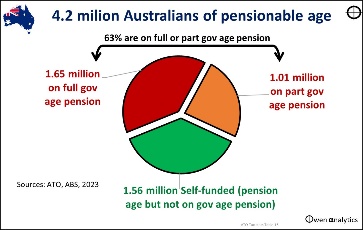

For the past 115 years, Australia has had a comprehensive government age pension system that pays inflation-indexed pensions for life (it is means tested, with generous tests). Australia was one of the first countries to offer this (Germany was first). Today, nearly two-thirds of retirees are on a full or part government age pension – even after more than 30 years of ‘compulsory super’, and it is still the bedrock of the retirement system.

Every retirement calculator and planning tool provided the government (eg moneysmart), retirement industry associations (eg ASFA), consumer organisations (eg, Super Consumers Australia), Super funds (eg AMP, AusSuper, UniSuper), and financial planning firms - assumes that the government age pension, and all of the generous tax breaks and benefits that go with it, will remain intact in future as the ultimate guaranteed, indexed-for-life, safety net for the rest of your life.

None of them pose questions like: ‘What if it is scaled back some time in the future?’, ‘Do you have a Plan B?’ Disclosure and disclaimer documents have pages and pages of ‘Risks’ like inflation risk, market risk, credit risk, currency risk, and so on, but none of them mention this risk: ‘What if future tax-payers are not as generous as they are today?’

What’s the problem?

Despite this long history of indexed-for-life age pensions, surveys show that a significant (and possibly growing) portion of Australians fear the age pension may be scaled back sometime in the future, and this is a major source of stress to many people. (eg. ‘Workers fear retiring’, NAB Wellbeing survey Q4 2024).

In addition, many super funds have reported that most members end up dying with a similar level of assets they had when they retired, citing a lack of trust in the pension as one possible reason retirees are overly frugal in their spending.

With continued aging population, rising aged care costs, and rising government debt levels, will future governments be able to afford to pay the pensions and benefits at current levels? Or will they need to reduce, or restrict access to, government age pensions and benefits, and/or reduce the generous tax benefits, or offset them with higher taxes?

How real is this fear? Let’s take a look at what is behind it.

Aging population

Australia started out as a young country (in terms of the age mix of its population anyway), but it has steadily grown old.

At Federation in 1901, only 4% of the population was 65 or over. Today this has risen to 17%, and is still rising.

We are not growing or importing enough young people to slow or stop this aging process. At Federation, 35% of the population were under 15 (future taxpayers in training!). This proportion has halved to 17% today, and is still declining.

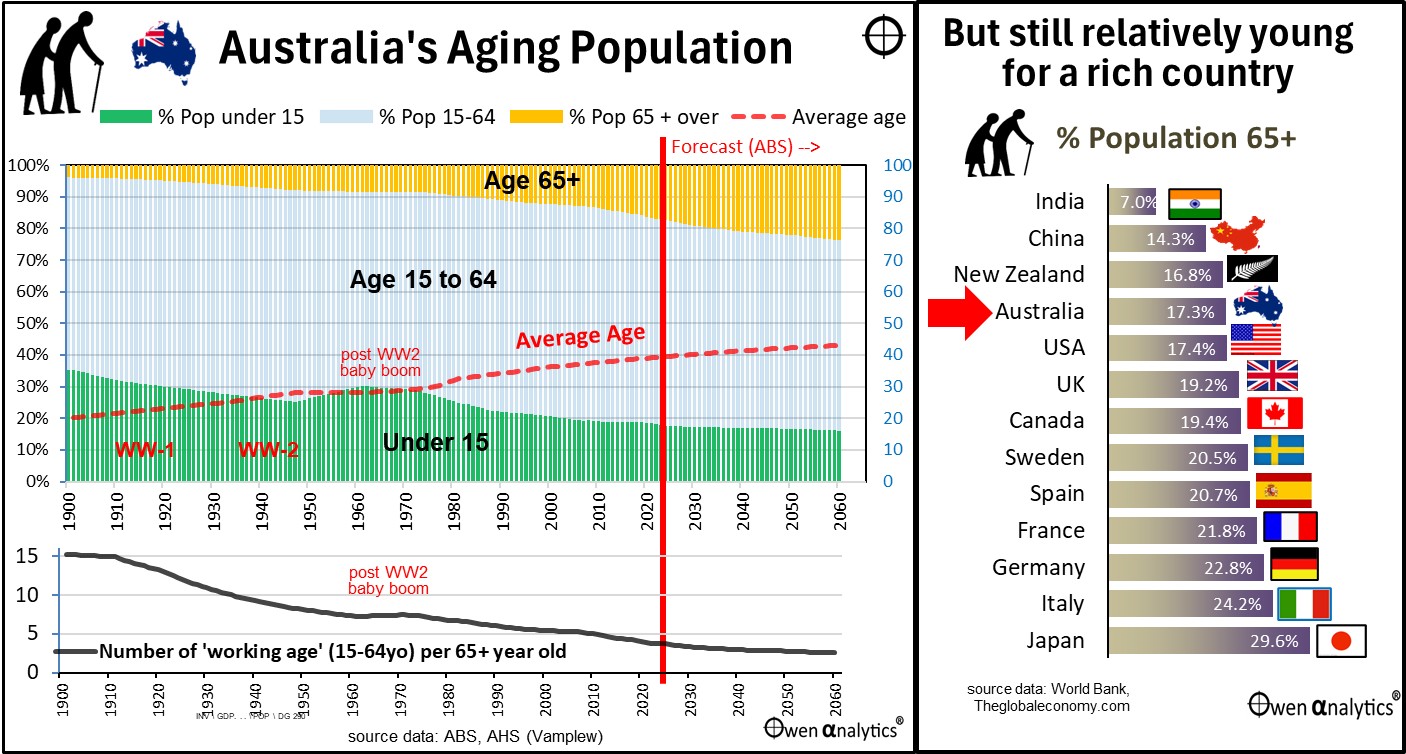

Today’s chart shows how Australia’s population has aged since 1900. The main chart shows changes in the proportion of the population in three age groups: - under 15 years old (green bars), 65 and over (orange bars), and aged 15-64 (light blue in the middle).

(NB. By global convention, 15-64 year olds are considered ‘working age’, but this is well and truly out of date in ‘rich’ countries where most 15 year olds continue in education until at least their late teens or early 20s.).

Meanwhile, the average age of Australians (red dotted line in main chart) has doubled – from 20 in 1901 to 40 today.

In the lower section of the main chart - at Federation there were 15 working-age people (defined as 15-64 year olds) for every one person 65 or older. Now there are less than 4, and the government is forecasting this to reduce to just 2.5 in the next 30 years.

Every working couple will ‘adopt a pensioner’ financially

This means that every working, tax-paying couple in Australia will effectively ‘adopt a pensioner’ (fund one pensioner) – in addition to supporting their own parents and kids if they have any. (It may even get to be like World Vision, where you receive a nice picture of your adopted/supported pensioner in their natural habitat!)

I suspect taxpayers will revolt well before it gets to that point. Reform is inevitable.

Why is this relevant to us today? Because, when planning to retire, we need some confidence that the ultimate safety net will still be there if things go wrong. If we don’t have that confidence, people feel the need to build an extra buffer - ‘just in case’ – by saving more, spending less, working longer, and/or setting lower lifestyle budgets and expectations in retirement.

Australia’s age pension system

The Federal government introduced the age pension in July 1909 at the rate of £1 per fortnight (£26 per year, or $4,500 in today’s dollars). This is less than one sixth of the current single age pension in today’s inflation-adjusted dollars.

The qualification age was 65 for males (as it was in Germany in the 1870s where aged pensions were first introduced) and 60 for females. There was also a residency test (20 years, not the 10-year test today), an income test, an assets test, and there was also a ‘good moral character’ test!

In its first year, although 190,000 people passed the age tests, only 70,401 people received the age pension (1.6% of the population) because of the other qualification tests. It was essentially a simple scheme to provide a dignified retirement income for the genuinely destitute – the people who really needed it.

Today, the current pension rate is $29,956 per year for singles and $45,161 per year for couples (combined). Even after more than 30 years of compulsory superannuation (which was intended to get people off the government pension), 64% of people of pension age are on a full or part government age pension, 2.7 million people in total.

It’s the gift that keeps on giving! (or for tax-payers, it’s an ever-expanding hole in your pocket!)

How real is the fear over future pensions?

With the rising proportion of elderly, rising aged care costs, rising range of services demanded of governments, and rising government debt levels, it seems something has to give.

It is at least enough to raise doubts about the sustainability of the age pension system that was introduced at a time when virtually nobody lived old enough to quality for it, and pass all of the tests.

Baby boom / immigration boom

Although the big shift in the population mix over the whole period certainly has been dramatic, it has not all been a one-way street. There is a possible solution.

The post WW-2 baby boom and immigration boom resulted in an increase in the proportion of under 15 year olds (green bars) in the 1950s and 1960s. This caused a levelling off of the proportion of 65+ year olds (orange), a similar levelling off in the average age (red dotted line), and also a levelling off of the number of 15-64 year olds per 65+ year old (black line in lower section.

So all is not lost. The trend can be paused and perhaps even reversed! But that would require another rapid and sustained boost to immigration and fertility, with immigration probably again doing most of the work.

Is this likely in future? One common trap investors (and humans in general) fall into is the assumption that current conditions will remain forever. They never do. Things can and do change in dramatic ways.

For example, it is quite possible to see such a sudden rise in immigration – for example in the event of sustained civil war in China, or a sustained China/Taiwan war, or another major war in Europe. Those could quite possibly result in large scale immigration at least on the scale of the post-WW2 population boost.

How does Australia compare?

Despite our rapidly aging population, Australia is actually one of the youngest ‘rich’ countries in the world. The right chart shows the percentage of population 65 and above lined up against a dozen other major countries, based on latest data.

Of the ‘rich world’ countries, only New Zealand has a younger population, but only by a faction.

One great advantage is that our population is still growing (mostly through immigration, as it has always been). In contrast, Japan, China, and most of Europe have declining populations, so they are in a (probably irreversible) death spiral – literally, with rising aged care costs, rising numbers of aged, and declining workforces and taxpayer bases to pay for it all.

Implications

Australia is probably in the best position of any country in the world to maintain its government age pension system.

-

-

- We have a relatively young population,

- relatively low federal government debt levels (see: The Debt Olympics – How do we rate),

- a growing population,

- an immigration system that is geared toward young workers and work-ready families.

- Australia has not yet suffered the extent of political unrest and resistance to immigration that we have seen in the US, UK, and Europe.

- Australia is probably far enough way from global conflicts, so the risk of invasion and occupation by a foreign hostile power is probably low (30-40 years is a long time and a lot can happen in the world that might upset our plans – just look at Eastern Europe, Asia, Africa, South America, Middle East over the past few decades!)

Probably most important of all is the fact that an increasingly aging population means an increasing proportion of grey voters (two thirds of whom are still on government age pensions), and it would be political suicide for a government to scale back welfare benefits to such a large and expanding voter bloc.

The bottom line is that if we can afford it (we probably are best placed in the world), then there would be enormous electoral pressure to retain the current system of age pensions and benefits in more or less the same shape and form.

The future?

I believe there is more than a good chance Australia will retain the same kinds of economic, social, and political conditions that will support its ability and willingness to continue the age pension system more or less in its current form. Fears of its demise are probably over-done.

However, I believe there is also more than a good chance that growing fiscal and political pressures will mean future governments will be forced to scale back to a more targeted system. Changes might include, for example - lifting the age of eligibility, raising the assets and income test thresholds, reducing some of the tax breaks, limiting exempt assets, and so on.

Paring back the pension system is inevitable economically and politically. What started out as a simple system to provide a dignified retirement for the destitute, has morphed into unaffordable bonanza of middle-class welfare.

Two thirds of retirees (2.7 million people) are on the teat, including folk who own multi-million dollar houses and have up to $1.047 million in assets (for couples) in addition to their house, and/or earn taxable income up to $99.7k pa (2025 rules).

Investment earnings on their Super accounts in ‘pension phase’ up to $1.9m in assets are tax free forever (and this threshold also rises for inflation), and pension payments from their Super accounts are also tax-free forever.

On top of the pension benefits and tax breaks, Federal, State, and local governments also have hosts of other benefits and discounts for ‘Seniors’, many of which are not means tested - see - Opal Card Survey - Black or Gold? Am I and ‘Adult’ or a ‘Senior’? (11-3-2025)

The purpose of Super?

Several large Super funds have reported that a large proportion of people die with more money than they had when they retired, and that doesn’t include the increased value of their house!

So it is not that unfair to say that the ‘Super’ system is basically a tax-advantaged estate planning tool. (eg ’Richer on death than retirement’, and ‘Super – tax-payer funded inheritance scheme’.)

On the other hand, around half of all retirees use their Super balance to pay down debt on retirement, so it could also be said that Super is a tax-advantaged mechanism for pushing up house prices.

Political pressure?

Workers may not begrudge working two jobs to pay taxes to fund a dignified retirement for the genuinely destitute, but if they knew the true extent of the largesse they were funding, they would revolt!

Reform will be politically difficult given the ever-increasing power of the grey vote and the number of people on the teat, but it will no doubt come to a head one day.

An additional problem with the system to date has been the enormous complexity (and costs of advice) created by continually fiddling with the rules – and there is no sign of this ending. This will fuel further cautiousness and uncertainty in the minds of current and future retirees.

What to do?

When running retirement portfolios for thousands of investors (pre-retired and retired), I have never been comfortable basing retirement planning tools and processes on the unquestioned assumption that the current government age pension and accompanying system of benefits and tax breaks will continue indefinitely. I have always built in a decent margin of safety for things to change – and they always do. Am I being too cautious?

Putting myself in the shoes of impending and current retirees (including clients of the advisers I advise), if that means I spend less than I theoretically (in hindsight) could, and that I die with more assets than I theoretically (in hindsight) need, then that is the price of peace of mind. When things change or go wrong - and they always do - we can’t always ‘go back to work’, or ‘save more’, or ‘sell some other assets’.

This is it. This is all we’ve have to live off for the rest of our lives on this planet, and it could be a lot longer than we planned! It pays to be cautious.

The bottom line –

If you want to build welfare dependence, then bank on receiving the government pension and take the risk that it may be scaled back in future. On the other hand, if you want to build financial independence, base your plans on not having to rely on hand-outs. That way you don’t have to worry about the sustainability of the government’s age pension system and the generosity of future over-burdened taxpayers.

Just food for thought. . .

‘Till next time. . . . safe investing, for a financially-independent future!

See also –

My latest monthly market snapshot for Aussie investors -

Plus check out my web site for 100+ recent, topical fact-based articles on a host of issues for inquisitive, independent-minded investors.