Key points:

- Here's my monthly wrap-up of financial markets for Australian global investors.

- Profit reporting season wrap-up & share price winners & losers.

- Shares still ahead for the year, Bitcoin down, Gold up.

- Progress on inflation, interest rates, recession fears, and plenty more.

February 2025 – what happened in markets and why

Greetings friends! - Here’s my monthly snapshot on global markets for Aussie investors.

It was Trump’s first full month back in office, and what a month it was! As expected, it was a blizzard of bizarre tweets, policy backflips, and laugh-a-minute entertainment - from a safe distance anyway. Who needs fiction when we have this sort of stuff in real life? Even the most creative fiction writers on speed could not make up this stuff!

For my fact-based assessment of the actual economic outcomes under the Trump and Biden presidencies, see:

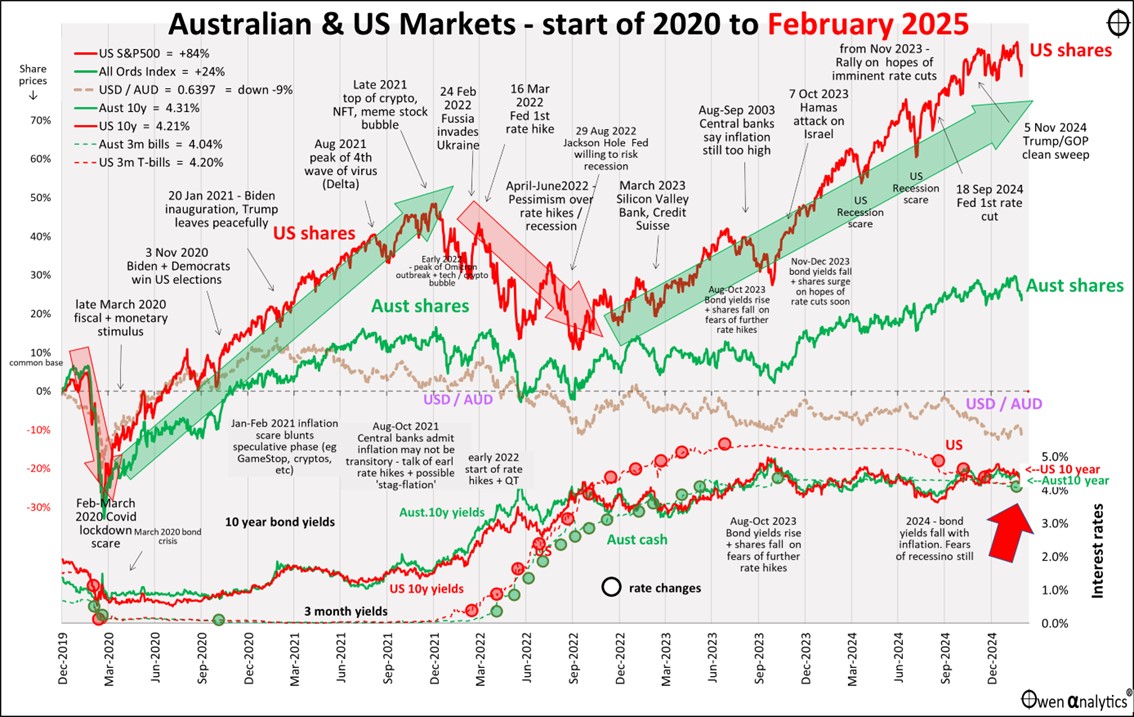

First - my essential 1-page snapshot chart - covering Australian and US share markets, short and long-term interest rates, inflation, and the AUD/USD exchange rate. As usual, there are two versions – first is the traditional version on a single chart:

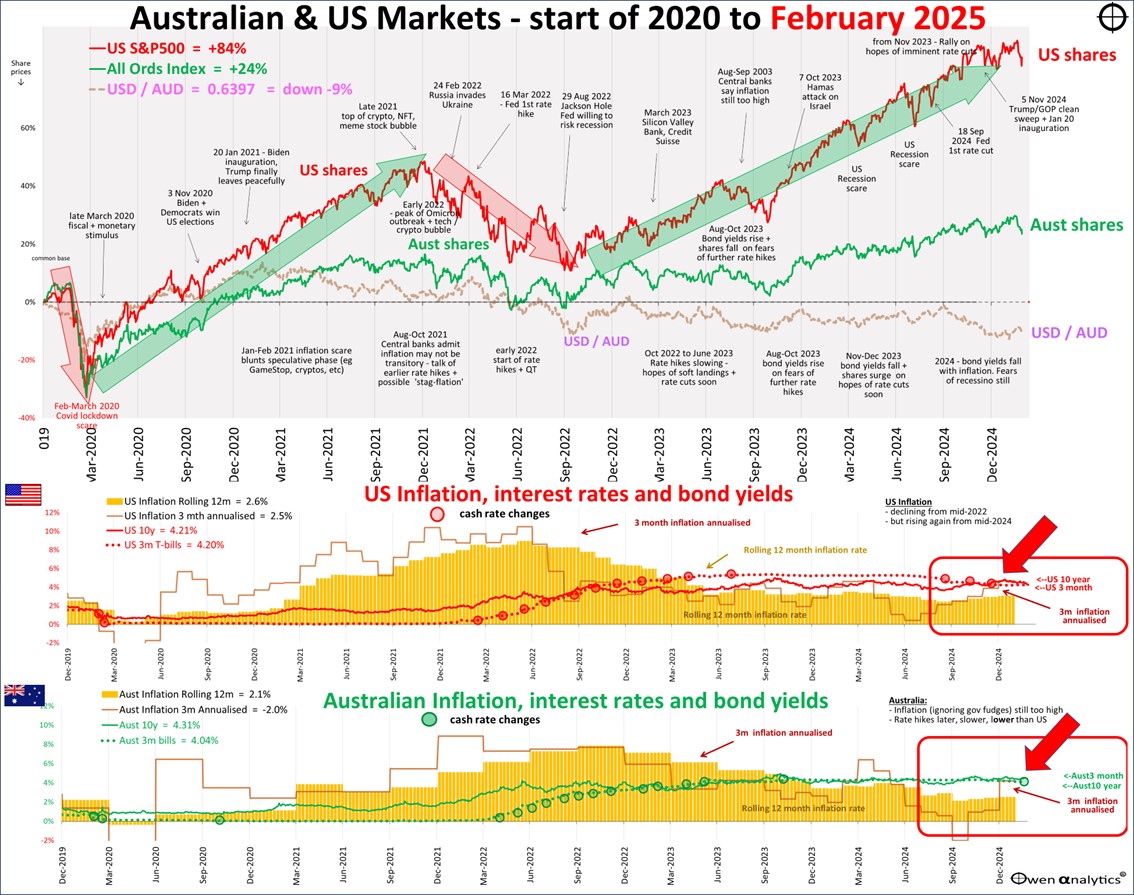

Also the alternate version below, requested and used by several advisers - showing Australian and US inflation separately in the lower sections (I deal with inflation in greater detail below):

(Last month I promised to simplify these charts a little as we are now getting into the SIXTH year since Covid. I will do more next month!)

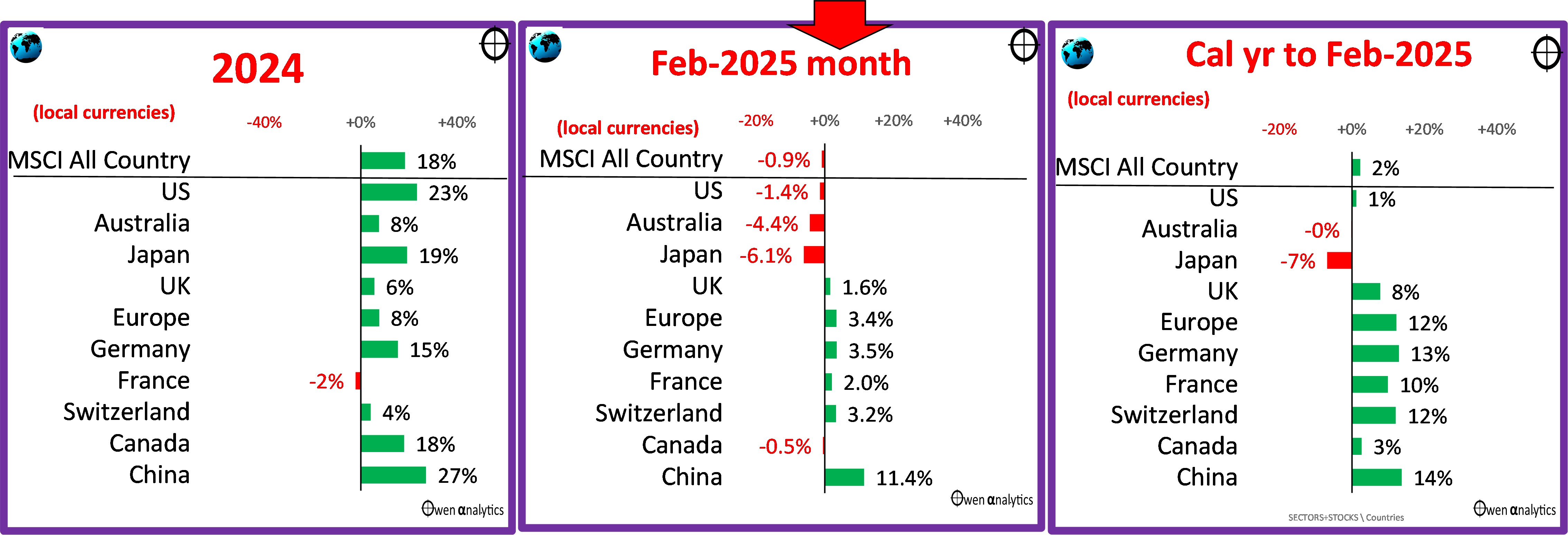

Global share markets

The overall global market ended down 1% in February, after a gain of 3% in January, so shares are still ahead more than 2% for the year. The mini-sell-off at the end of the month can be seen at the top right end of the red and greens for the US and Australian share markets. It was just another in a long line of mini-corrections along the long upward march.

In the five year period of these charts, we have also had a couple of more serious corrections – the Covid lockdown crisis in 2020, and then the 2022 rate hike sell-off which killed the speculative tech / meme-stock bubble (or took the winds out of its sails anyway. There is a good chance we will have another serious-ish correction in the coming year.

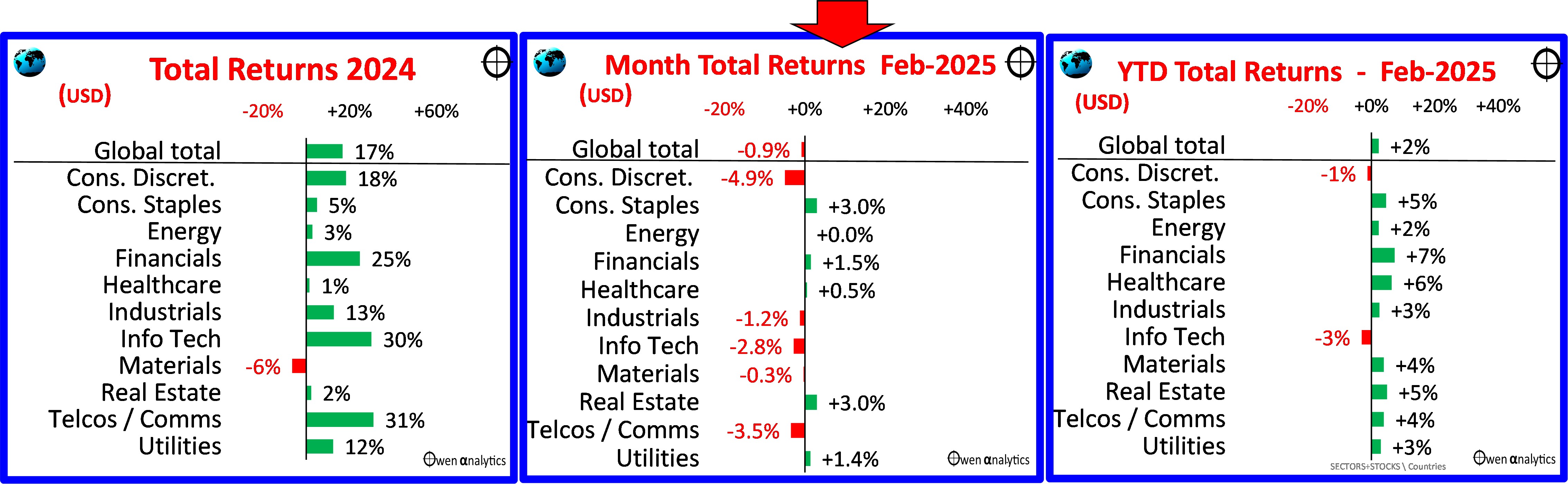

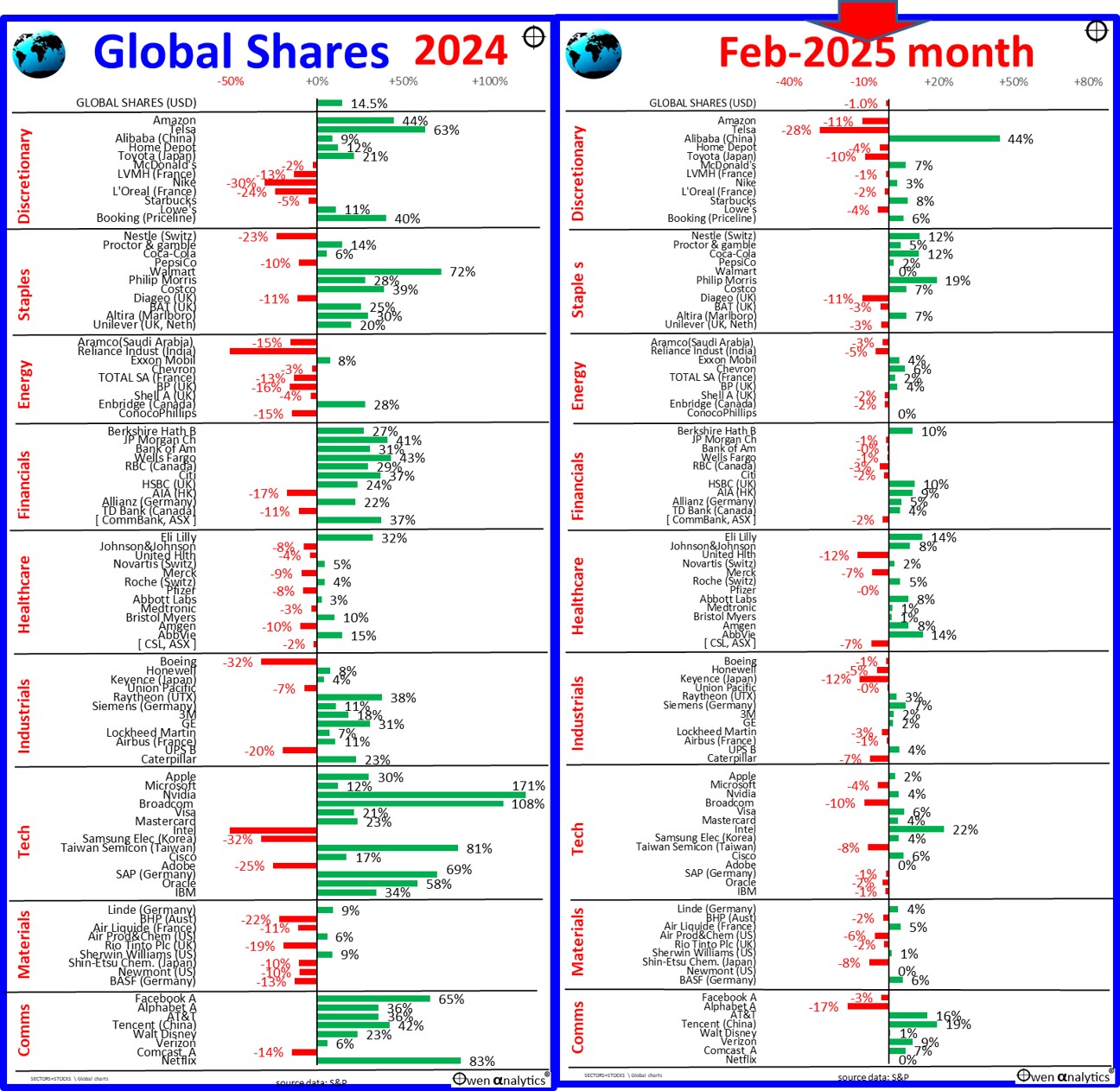

Industry Sectors

After all sectors were stronger in January (except Tech, hit by the DeepSeek shock), February was more of a mixed outcome for the main sectors. US tech giants dragged down Discretionaries (Tesla, Amazon), Tech (Microsoft, Broadcom), and Comms (Alphabet/Google, Meta/Facebook), the rest of the market was more or less flat or a little higher.

Here are the global sector returns for February (middle chart), compared to calendar 2024 (left chart), and February year to date (right chart):

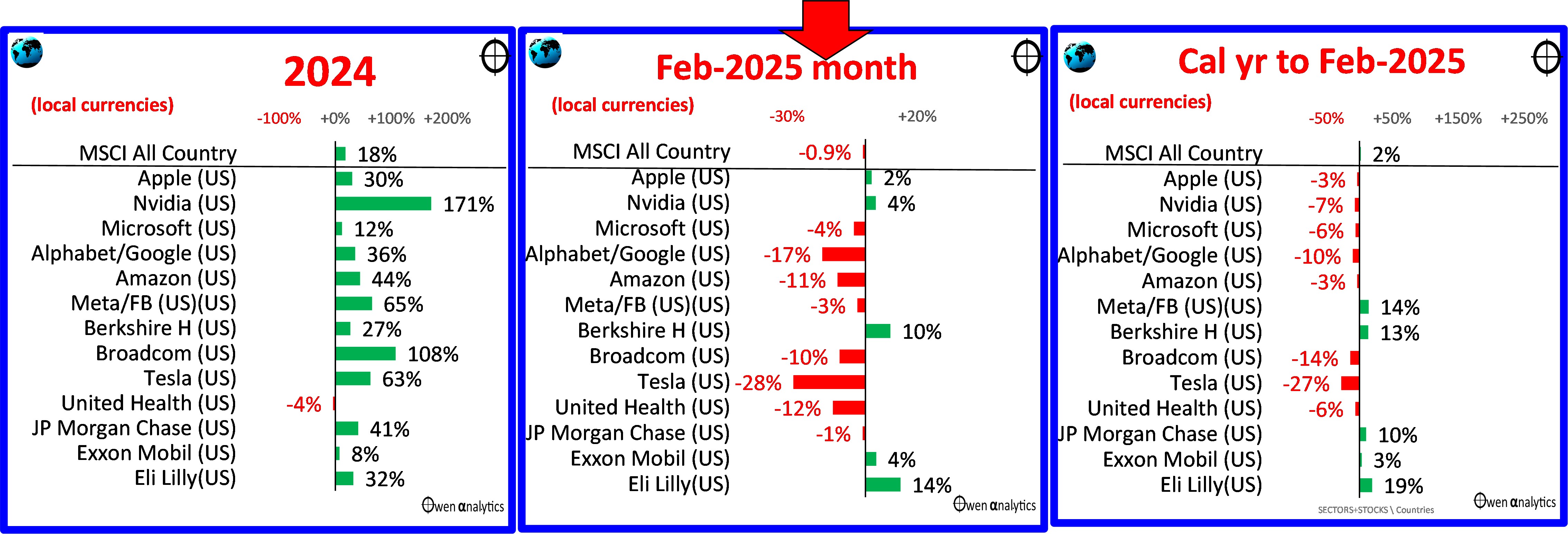

Major stocks

Here is the picture for the major global stocks (all of which are US based) – again showing 2024 (left), February month (middle), and 2025 calendar year to date (right):

US market (S&P500) also made two new all-time record highs in February, but ended down 1% for the month.

For a fuller picture of Feb versus calendar 2024, here are the main global stocks I cover, organised by sector:

US earnings season very strong overall

US earnings season for the 4th quarter 2024 was mostly in January, but wrapped up in February. 76% of the S&P500 companies beat their earnings expectations, which is a little higher than historical average.

US profits are doing just fine. Aggregate 4th quarter 2024 earnings per share were 22% higher than 4th quarter 2023, and calendar year 2024 earnings were 9.5% above calendar 2023. So US profits are growing strongly.

However, the share prices of US tech giants were mostly down in February, despite all but one beating earnings expectations:

-

-

- Tesla was down -27% in February – after earnings came in just below expectations

- Amazon, Alphabet/Google, Broadcom, Microsoft and Meta/Facebook were all down for the month despite all beating earnings expectations

- Nvidia, Apple, and Intel were stronger in February after beating earnings expectations.

The tech giants are still very expensive on a range of metrics. See my recent report -

Major country share markets

The US market (65% of the overall global share market value) was down just 1% in February, after hitting new all-time highs during the month.

The Japanese market fell -6%, mainly due to Softbank and Keyence (factory robotics) and Toyota (slowing global sales momentum).

European markets were particularly strong, with the prospect of further rate cuts and recession rebounds. Apart from Germany’s CDU conservative Frederich Merz replacing SPD socialist Olaf Scholz as Chancellor, the main theme in Europe has been a surge in urgency to arm up in anticipation of a US withdrawal from funding NATO and Ukraine’s defence.

UK and Swiss markets in particular were boosted by the global rally in healthcare stocks, in the face of Trump’s’ war on ‘big pharma’. So far, Trump’s new health secretary RF Kenedy has been far less vocal and active than some of his other lieutenants, like Elon Musk, JD Vance, and Scott Bessent.

Despite China’s domestic economic quagmire, Chinese stock markets were boosted by Xi Jinping welcoming previously exiled tech oligarchs back into the fold. Xi has suddenly realised he needs them for China to dominate world markets - ai, surveillance tech, EVs, solar panels, wind turbines, etc. Alibaba soared +44%, Tencent +19% on the news.

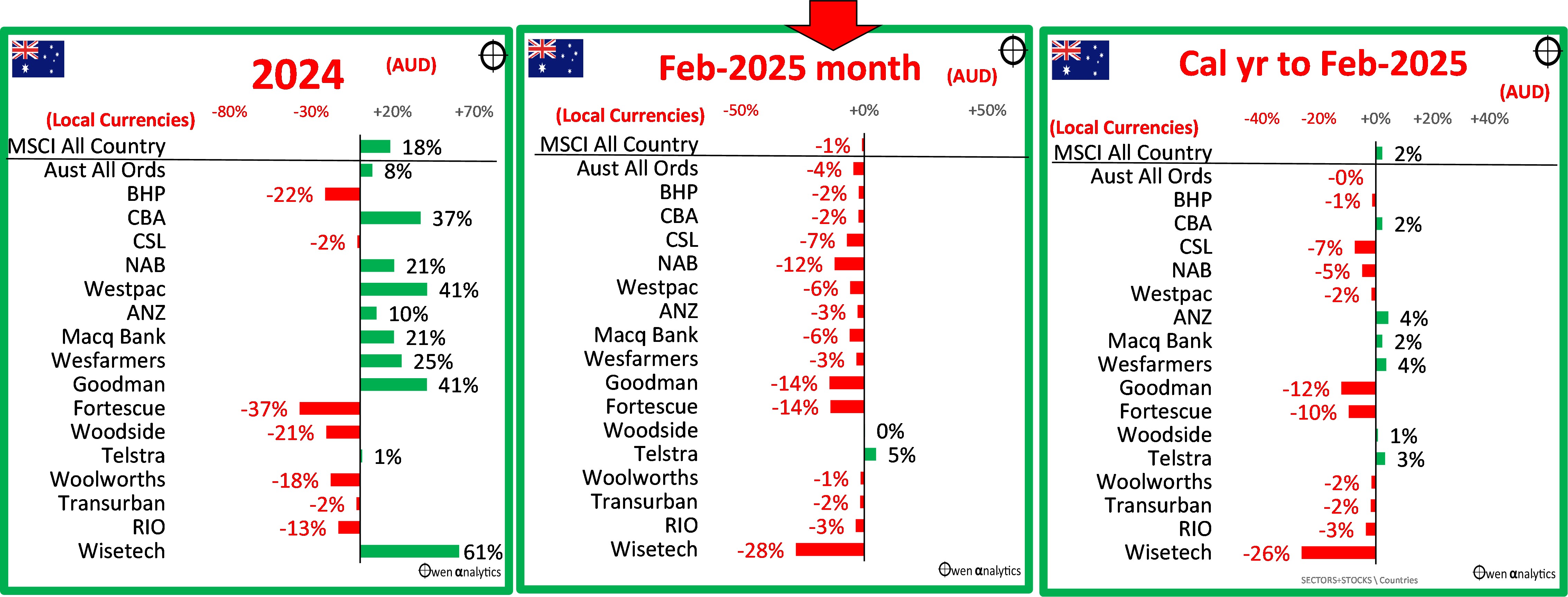

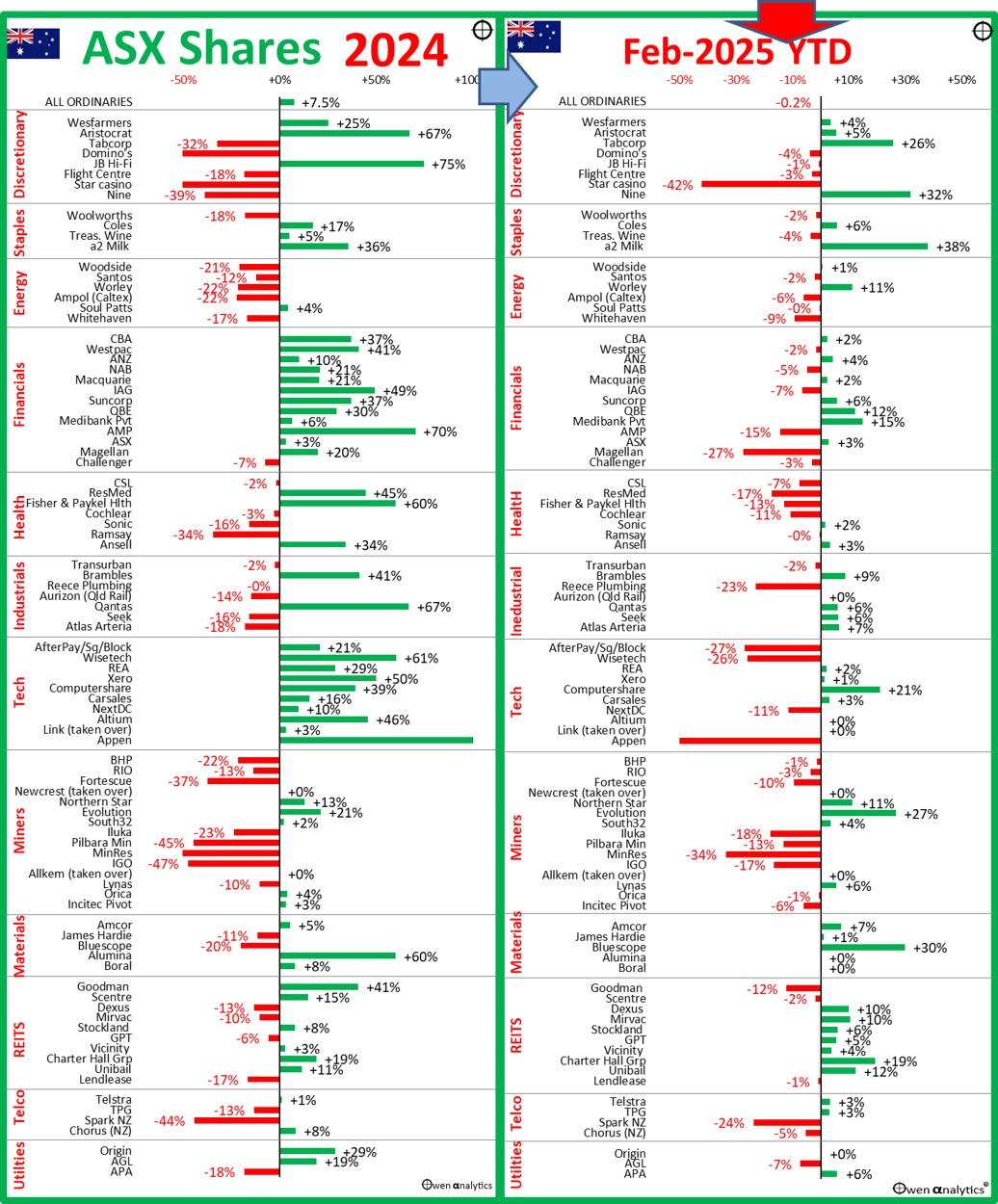

Australian shares

The local share market soared and hit four new all-time highs in February, but ended the month down 4%. But that was really only giving back January’s gain, so we are only back to the start of year for the market as a whole.

In contrast to other global markets, it was a sea of red ink for the main ASX stocks in February (middle chart):

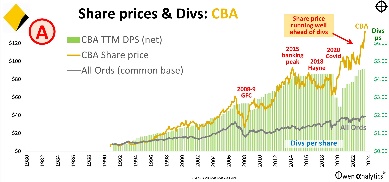

The largest sector, the big banks, were all down in February with uninspiring results (NAB was worst, down -12% for the month), but they are more or less flat for the year to date. Banks had a very strong year in 2024 (and also 2023), and it is hard to see how they can sustain their record levels of over-pricing despite stagnant growth and a truckload of problems, mostly of their own making.

For more on CBA’s pricing and prosects, see:

The other main sector of the local market – miners - are mostly down this year with the continued slide in commodities prices – mainly iron ore, industrial metals, and battery metals. Mineral Resources has had added problems with founder Chris Elison’s shenanigans.

Gold miners were the only bright spot with the continued surge in the gold price (see below).

In the local tech sector, Wisetech was dumped by institutions after founder Richard White forced out the chairman and four other directors who were trying to oust him for his various shenanigans. Square/Block/XYZ was also down on slowdown fears in the US.

Star Casino took more heavy share price losses. Unfortunately for tax-payers, this sordid gambling den and money laundering mecca is looking like being yet another government (tax-payer) bailout because for some ridiculous reason it is deemed ‘too important to fail’!

On the positive side, Nine got a boost when it received a takeover bid for Domain.com, its main asset.

The February earnings season saw an unusual number of companies beating expectations (Aussie companies average around 40% earnings ‘beats’ per year, well below 70-75% average in the US market).

Share prices of several companies were impacted by deteriorating US outlooks. For example – perennial out-performer Reece Plumbing once again beat earnings expectations but was hammered by comments about slowing US construction activity.

Here are the main ASX stocks by industry sector – year to date calendar 2025 (right) compared to calendar 2024 (left):

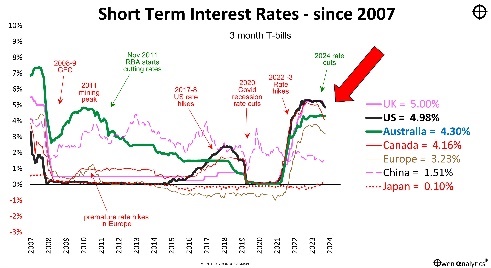

Inflation & interest rates

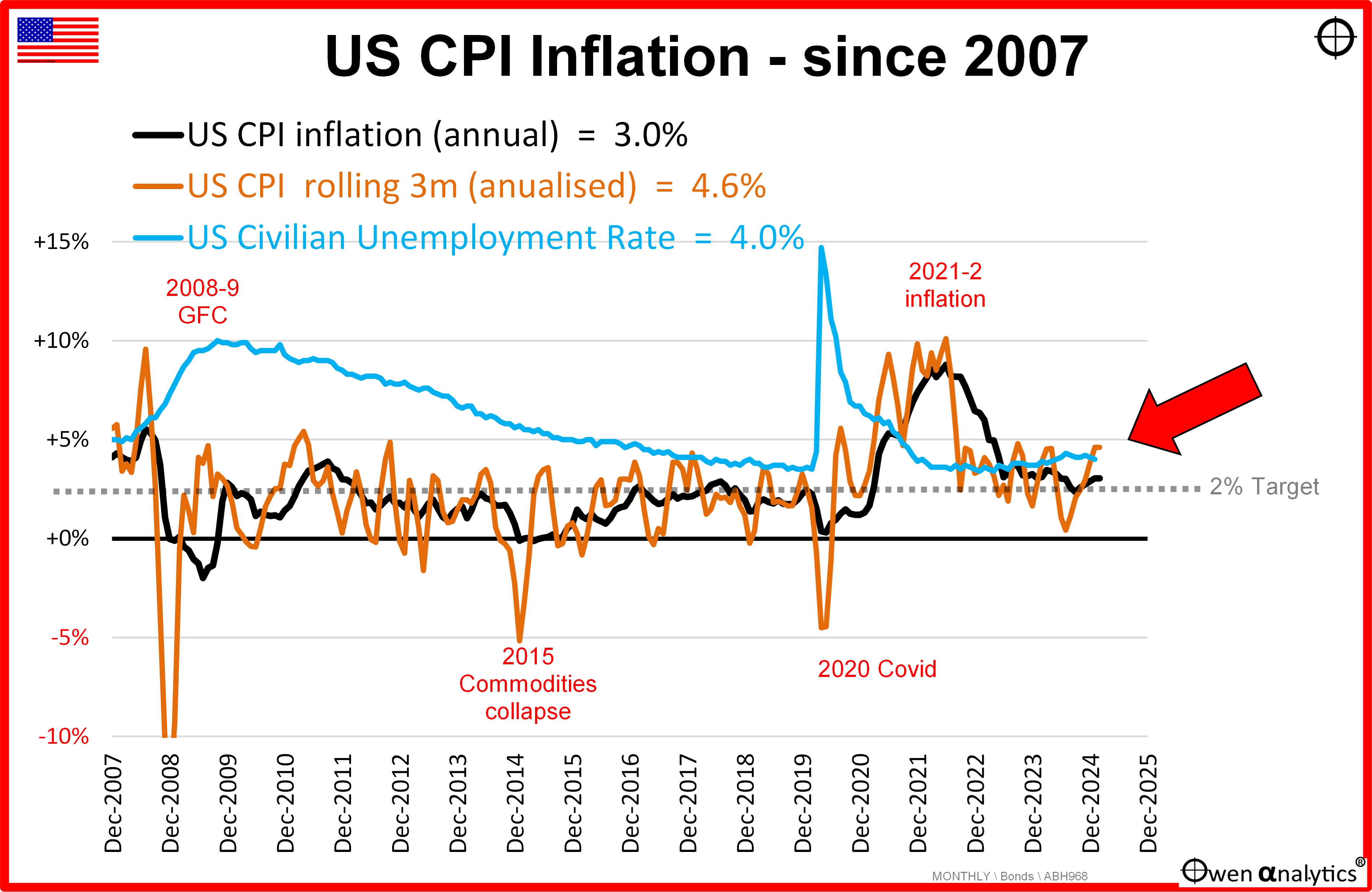

After three rate cuts in September, November and December, the Fed hit the pause button and said they are in no hurry to cut rates further. The problem is that US inflation is on the rise again – the 12-month rate rising to 3.0%, and annualised 3-month running rate rising to 4.6%. On top of that, the jobs market remains strong, with unemployment falling back to 4.0%.

Here is the US picture:

With emerging signs of slowdown in confidence, spending, and business investment, the Fed will not be able to cut rates unless inflation falls and/or unemployment rises. An economic recession would do both.

Australia

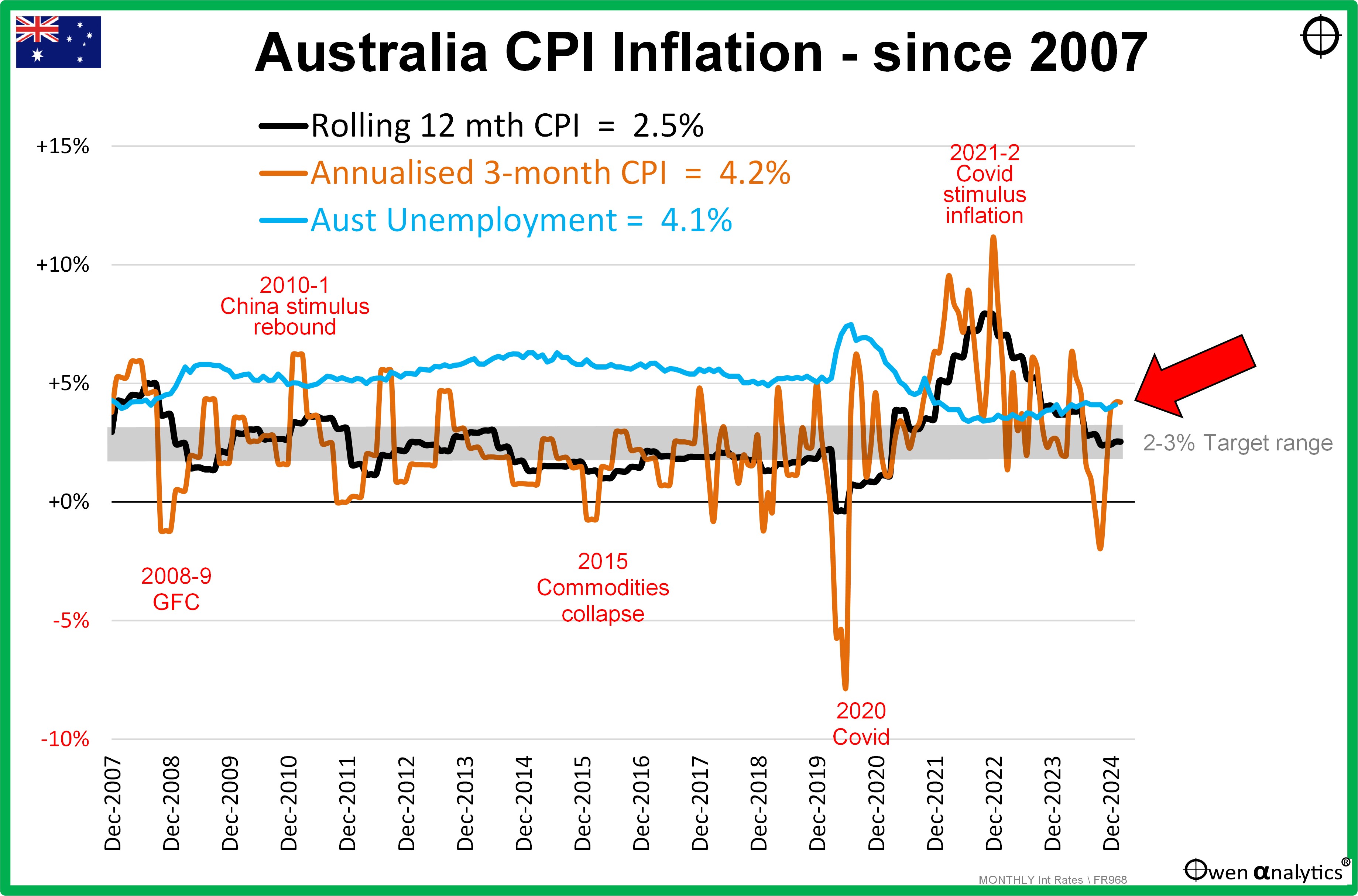

The RBA finally made its first reluctant rate cut on 18 February – down by 0.25% to 4.1%. The RBA rate hikes were later, slower, and lower than the rest of the world in attacking inflation, plus we have a more centralised wages system here and a pro-wage inflation government, so inflation has remained stickier here than elsewhere.

There is no doubt the RBA has lost some of its ‘independence’ under smiling Jim Charmer, and there also is a lively debate about the extent of political pressure on the RBA chief to change her wording on the causes of the sticky inflation problem, and to deliver a rate cut before the election. She did, but the stated reasons were far from compelling.

Here is the Australian picture:

The CPI numbers are still being artificially depressed by temporary government power and rent subsidies. As with the US, the most obvious reason for rate cuts would be a local recession, which would lift unemployment and probably soften inflation pressures, allowing (or necessitating) rate cuts.

See my recent report on inflation and interest rates in Australia versus other major countries, see:

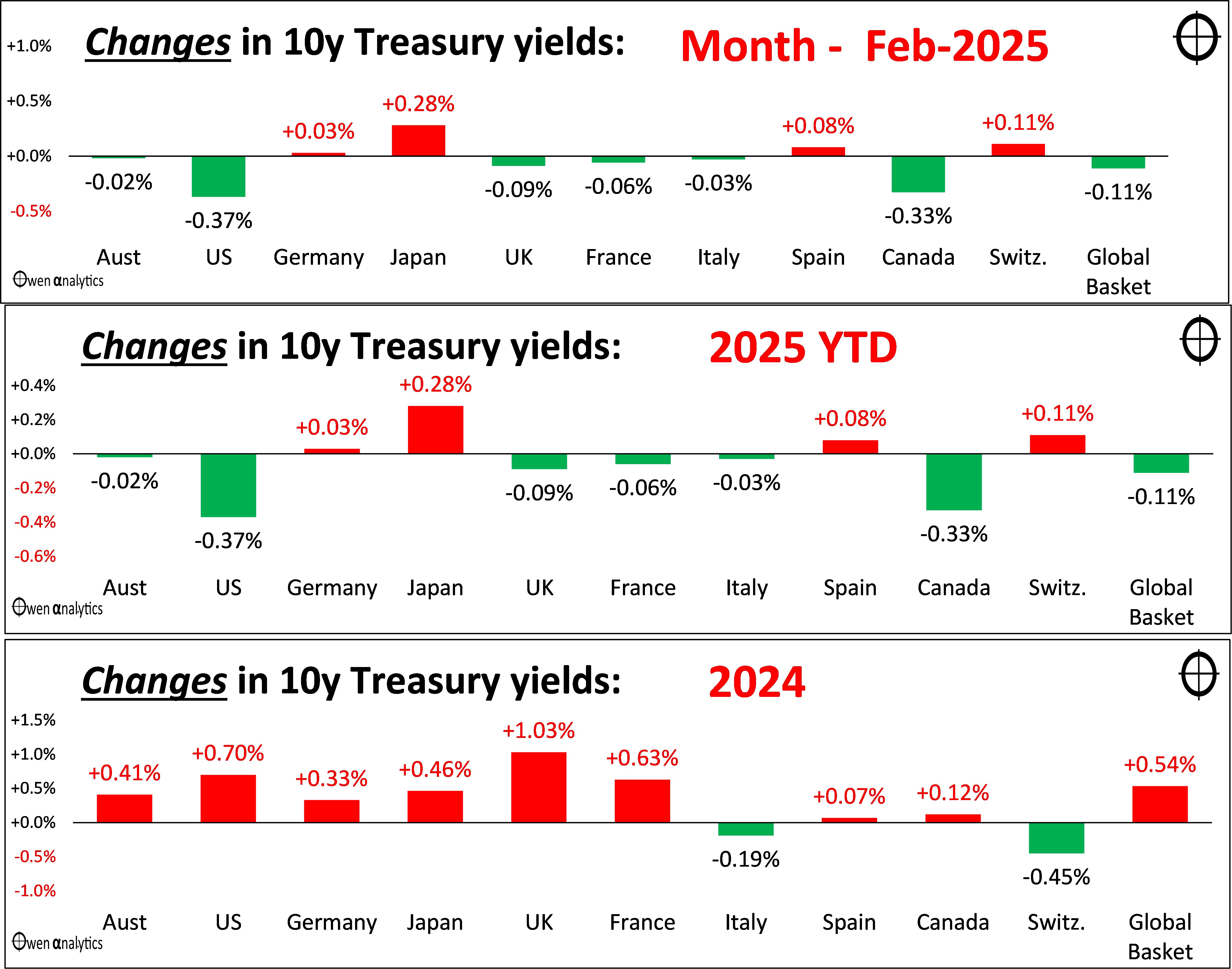

Bond yields

Bond yields have travelled more or less in a sideways band since late 2022 after the initial aggressive rate hikes. US yields fell in February, after the yield spike on Trump’s re-election in late January. The decline in yields in February, despite a revival of inflation to well above target range, is probably a sign of gathering fears of economic slowdown.

These fears are probably related to Trump’s tariff wars with America’s largest trading partners – Canada and Mexico because the countries with the largest yield declines have been the US, Canada and Mexico.

The next trio of charts show changes in 10-year treasury yields in the major world markets – in February (top chart), and calendar 2025 to date (middle), and calendar 2024 for comparison (lower chart).

Yield rises are in red (as they cause capital losses), and yield declines are green (capital gains on bonds).

Mexico is not on the charts as it is not a bond market I study, but Mexican 10-year yields have also fallen by 0.6% in February (from 10.4% to 9.8%). It looks like tariff/trade related slowdown fears for the US-Canada-Mexico trading bloc.

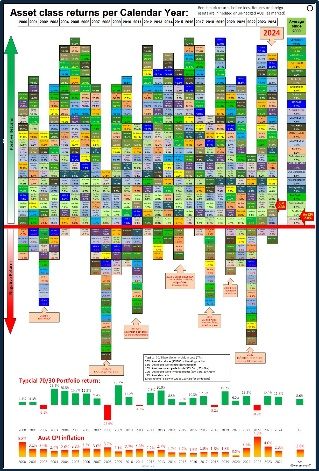

Bonds in portfolios?

(Most Aussie direct investors don’t get bonds, but I study them and comment on them regularly because professional and institutional diversified funds (like Super funds and advice groups) are required by their mandate rules to have sizeable allocations to bonds. Personally, I am not governed by mandates, but I do have to use them in my roles on Investment Committees, and they do have legitimate roles in long-term portfolios.)

Government bonds often do well in economic slowdowns that are usually (but not always) accompanied by falling bond yields as inflation falls – a prime example was the 2008-9 GFC. But the gains on bonds on the way into recessions are quickly lost again on the way out.

You need to be extremely good to time getting in and out of bonds on the way into and out of recessions! I have done it successfully when I was younger and more nimble, but I am happy to sit out the bond market in the current conditions of problematic medium term inflation.

Bond markets have had a terrible time since 2021 with the return of inflation, including the worst losses on bond markets in a century in 2022. I have been out of fixed rate bonds in portfolios since 2020 (preferring high grade floating rate instead). I remain bearish on fixed rate this year as well, with inflation remaining sticky in Australia and the US.

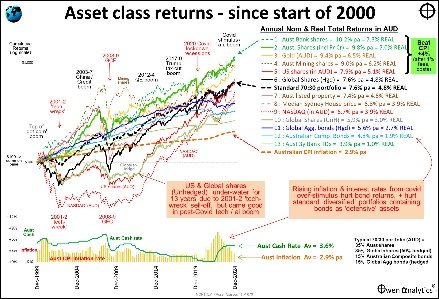

In other news – Bitcoin down, Gold up

-

- Bitcoin is down 21% from its peak the day Trump was re-elected in January. There was another massive hacking/theft in a major crypto exchange (ho hum – BuyBit this time), but that is par for the course.

- I know very little about Bitcoin but I did find Satoshi’s October 2008 paper very compelling, and I like the philosophy behind the idea - complete and absolute freedom from governments, regulators, central banks, commercial banks, taxes, intermediaries, public scrutiny and surveillance, anti-money-laundering laws, freedom from centralised computers or databases, etc, etc. Who wouldn’t want that? I do not own any Bitcoin or other cryptos.

- Meme-coins are out (I think) after a brief flurry in January. I know even less about these, and I probably should keep it that way!

- Gold is up. I have been studying gold (and buying judiciously in various forms) over the past 25 years since the 1980 gold frenzy (no, I was not a buyer in the 1980s gold frenzy, nor the 2011 gold frenzy – never buy anything in a buying frenzy!).

- I put gold into diversified portfolios last year and it is up 35% in USD terms since the start of 2023 (mainly strong buying by central banks and Chinese nationals), and it is up 50% in AUD terms because of the decline in the Aussie dollar. (In portfolios I have the un-hedged ETF version, so we get the AUD returns.)

- But that does not mean rush out and buy it now! Every year we face a whole new set of challenges.

- Stay tuned. .

‘Till next time – safe investing!

Some further reading for insomniacs:

For my current views on asset classes and asset allocations in my actual long-term ETF portfolio - see:

Plus check out my web site for 100+ of topical articles on a host of issues affecting investors and investing.