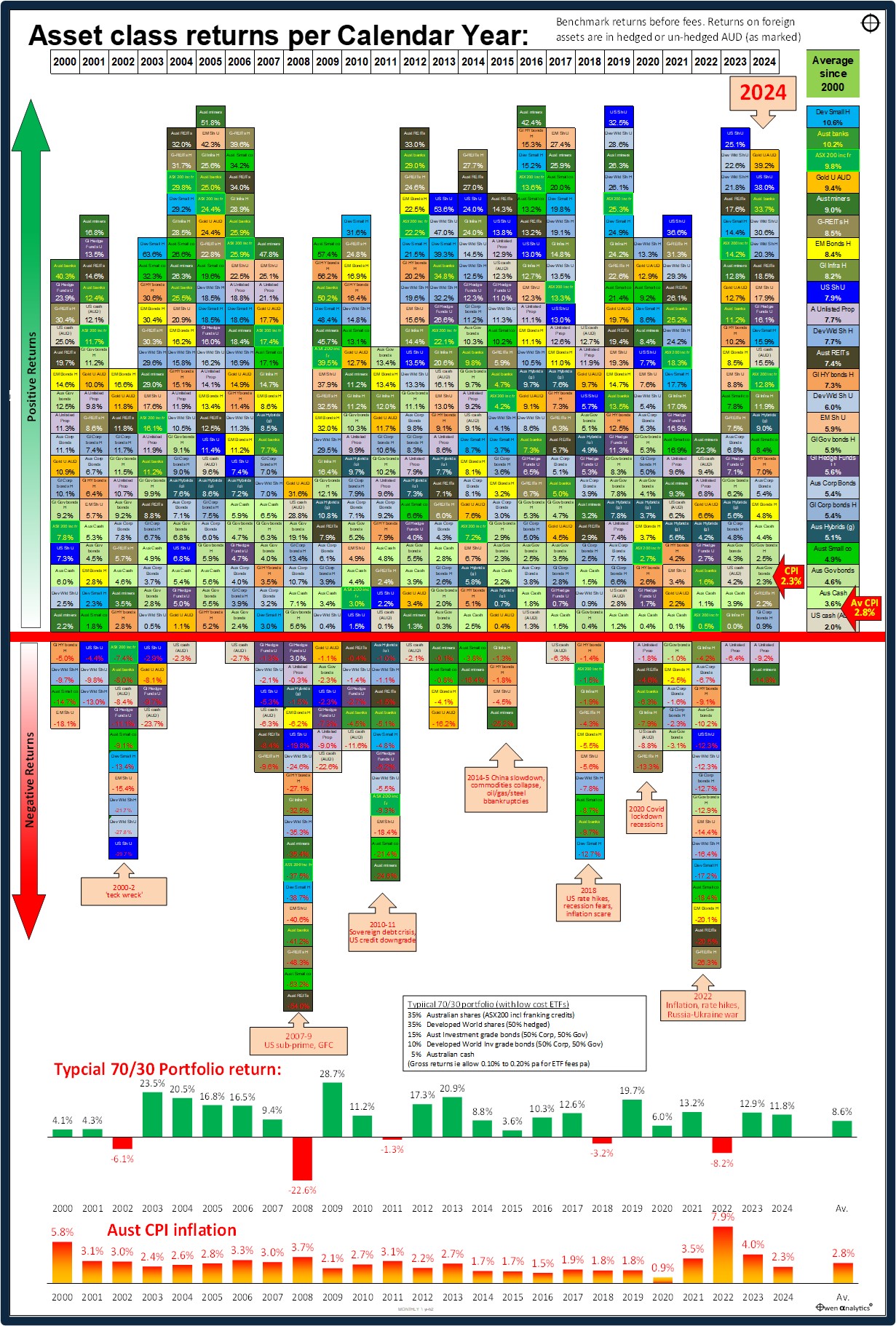

Despite continual tiresome warnings of an imminent US-led global recession from economists and market 'experts', plus a host of other threats - including widening of wars in Ukraine and the Middle East, stagnation in China, mounting deficits and debts in the US and around the world, an on-going confidence-sapping ‘cost of living crisis’, and high political drama in the US - almost all of the main asset classes did well in 2024, beating inflation, and most did better than their long-term averages.

Today’s chart shows total returns (ie price gains/losses plus income) from two dozen of the main types of investment assets per calendar year since the start of the century. Returns above the red line are positive, below are negative.

This is designed primarily for Australian investors, so returns from international assets come in two flavours – hedged AUD, and un-hedged AUD, as marked.

(A table of benchmarks for each asset class/segment is included at the end of this article.)

2024 – another bumper year for almost all asset classes

Almost all of the main asset classes were positive in 2024 (above the red line), and ahead of inflation (red arrow). CPI inflation in Australia is still running at 2.3% (or around 3% if you back out the government fudges with temporary power bill subsidies that will end in early 2025).

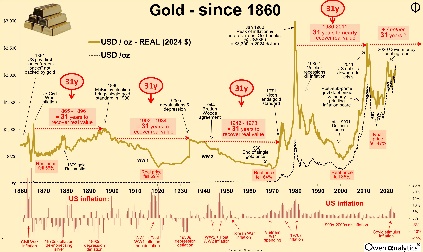

The winner is. . . . . Gold!

At the top of the 2024 column is Gold in Australian dollars. The gold price was up 26.5% in US dollar terms in 2024, but it was up a whopping 39% in Aussie dollar terms thanks to the 9% decline in the Aussie dollar against the US dollar over the year.

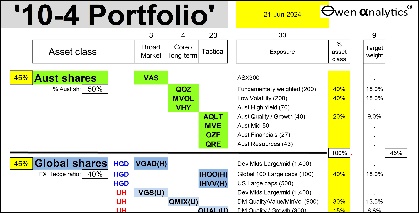

My own personal long term portfolio – my ‘All-weather 10-4 ETF portfolio' - has an allocation to unhedged AUD gold – see My ‘10-4 all-weather ETF portfolio’ – Part 2: What’s in it? (7 July 2024)

Gold has hardly been an inflation hedge. The gold price rose +5% in 2020 when inflation went negative in the Covid lockdowns. In 2021, the gold price fell as inflation soared in the US and around the world. Then gold was virtually flat in 2022 and 2023 when inflation remained worryingly high. But in 2024. inflation fell back toward target ranges in the US and around the world, but the gold price soared. This is the opposite of what an inflation hedge would do.

If not an inflation hedge, why has the gold price surged? - and why have I been bullish on gold?

Three main reasons. First, strong central bank buying, as dictators are reducing their reliance on US dollars after the US confiscation of Russian US dollar assets following Russia’s invasion of Ukraine. Second, strong buying from Chinese nationals as property prices continue to collapse. Third, people everywhere (including me) have been buying gold as a hedge against rising geopolitical tensions and political unrest, as elections around the world lurched toward populist, nationalist, xenophobic, racist parties, including Trump in the US.

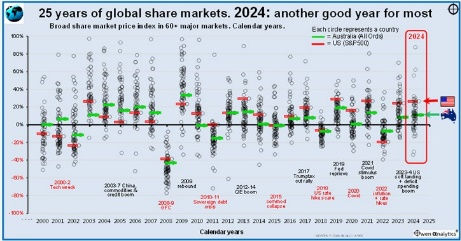

80% of share markets were also up in 2024, in defiance of continual and tiresome forecasts of economists everywhere of imminent recession and market crashes - see

Negative returns

Only two asset classes/segments posted negative returns in 2024 - Australian miners and Australian unlisted property.

Mining stocks are essentially just leveraged bets on commodities prices (they have operational leverage via their fixed costs bases, and financial leverage via gearing). In Australia’s case the only commodity that really matters is the iron ore price, which fell -28%, more than wiping out the windfall gains in 2023. As with many other industrial commodities – expanding supply swamped weak demand, resulting in price falls.

There were also dozens of battery metals stocks (mainly lithium and nickel) that were down heavily in 2024, but they are tiny and have virtually no impact on the mining index or the overall market index.

The gold price was up in 2024 but the ASX lost Newcrest to Newmont (US) in October 2023, so the rising gold price no longer has much of an impact on the overall local market index.

Commercial property woes continue

Australian unlisted property funds had another negative year in 2024, with the two main sectors – office and retail shopping centres continuing to suffer long-lasting negative effects of the Covid lockdowns – the rise of online retailing affecting shopping centres, and the ‘work from home’ revolution raising office vacancy rates, and depressing rents and capital values.

On the other hand, listed property trusts (A-REITS) had a reasonably good year in 2024, recovering from their over-sold levels in 2021 and 2022, boosted by industrial giant Goodman.

Bond markets posted low single-digit returns in 2024 as bond yields rose with ‘higher for longer inflation’ fears. I have been out of fixed rate bonds in advised portfolios since 2020.

Asset class annual returns since 2000

The table on the whole looks like a random patchwork quilt of returns, with no apparent rhyme or reason. Each year has different winners and losers, with returns from every type of asset jumping around from year to year.

Some quick observations:

- In most years, most types of investments post positive returns, and ahead of inflation.

- There are occasional years when everything is positive – like 2005, 2016, and 2019.

- But the rest of the time there are some types of assets that go backwards, while most are positive.

- In the big bust years (like 2008 and 2022), most asset types post negative returns.

- But even in the worst years, several asset types still manage to post positive returns, although the winners are different each time.

Most frequent highest returning assets

The asset types with the most years with the highest returns are:

- Australian miners = 5 years – mostly thanks to iron ore in the post-2000 China boom, which is now over.

- US shares (Unhedged) = 4 years – mainly in the recent tech/online boom.

- Australian REITS = 3 years – mainly recovering from their savage sell-off in the GFC.

- Global REITS (hedged) = 2 years

- Gold (unhedged AUD) = 2 years (2008, the year of the GFC sell-off, and 2024)

- Developed world small companies (hedged) = 2 years

- Developed world shares (hedged) = 1 year

- Australian banks = 2 years (including 2024)

- Australian small companies = 1 year

- Emerging Markets shares (unhedged) = 1 year

- Emerging Markets bonds (hedged) = 1 year

- Australian government bonds = 1 year

- USD cash (unhedged) = 1 year

Most frequent lowest returning assets

Asset types with the most years with the lowest returns are:

- USD cash (unhedged AUD) = 8 years as the lowest returning asset type – so much for the ultimate ‘safe haven!’

- Global REITS (hedged) = 3 years – mostly in Covid lockdowns and the post-Covid inflation spike

- Australian miners = 3 years, when commodities prices collapse, including 2024

- Australian unlisted property trusts = 2 years (2023 and 2024)

- Gold (unhedged) = 2 years

- Emerging Markets shares (unhedged) = 1 year

- DM shares (hedged) = 1 year

- US shares (unhedged) = 1 year

- Global Hi Yield bonds (hedged) = 1 year

- Australian REITS = 1 year

- Developed world small companies (hedged) = 1 year

- Australian government bonds = 1 year

- Global infrastructure (hedged) = 1 year

- Australian cash = 1 year

Average returns since 2000

The far right column shows average annualised returns so far this century since the start of 2000.

So far this century:

- every type of asset has generated positive total returns (above the red line)

- everything except USD cash (in the hands of un-hedged Aussie investors) has beaten inflation

- 1st place with highest average total returns this century = Developed world small companies (in hedged AUD)

- 2nd = Australian banks (but they only overtook Australian miners in 2024)

- 3rd = Australian shares (ASX200 including franking credits)

- 4th = Gold in AUD, after the surge in 2024

- 5th = Australian miners (were coming 2nd place until overtaken by gold in 2024)

US and global share markets are well down the overall league table so far this century because they suffered badly in the 2001-2 ‘tech wreck’. However, we can see that US shares have been at or near the top of the returns table in recent years. But US and global shares are certain to fall heavily again when the current US-led global tech boom collapses (always have, always will – this time is not different!)

What to do? Portfolio construction

Good portfolio construction is not about trying to pick the best asset classes each year, or trying to avoid the worst.

Nor is it about chasing last year's winners (hoping for a ‘momentum’ effect), or chasing last year's losers (hoping for a ‘contrarian’ or ‘reversion’ effect). These strategies almost always destroy wealth.

Good portfolio construction is about selecting the appropriate mix of assets so the portfolio as a whole has the greatest probability of achieving each investor’s long-term goals, within their tolerance for risk and volatility (ups and downs along the way), and their liquidity requirements. Because each investor has different goals, needs, risk tolerance, and cash needs, each investor has a different ‘ideal’ portfolio.

Sample '70/30' portfolio returns

Having said that, on our simple ‘70/30’ portfolio (70% ‘growth’, 30% ;’defensive’ - second bottom panel in the chart), returns are before fees, assuming no ‘alpha’, and no asset allocation changes, just setting the initial ‘strategic’ asset allocation and then re-balancing to the target allocations each year.

Key outcomes for our simple 70/30 portfolio:

- Overall average returns of 8.6% pa this century (before fees). That’s better than the Future Fund, Australian Super, and even the best of the ‘industry funds’. It's tax effective and transparent - you know exactly what's in it and how it is valued - which is more than can be said for industry funds with their opaque holdings and fudged valuations. Anybody with a few hundred dollars can invest in our simple 70/30 fund using low-cost ETFs.

- With inflation averaging 2.8% pa this century, our simple 70/30 portfolio would have returned well above CPI+5% pa (even after allowing for ETF fees of say 0.1% to 0.2% pa), which is a typical target return for long-term ‘growth’ portfolios.

- There have been five years of negative 70/30 portfolio returns this century (2002, 2008, 2011,2018, and 2022), but four out of five of these negative years were followed by very strong rebounds in the following years.

Crypto?

Crypto spruikers will no doubt notice that I have not included bitcoin or other crypto’s in this chart of asset class returns. I have not included bitcoin as it does not have a return history over the period covered, and it has not yet lived up to its lofty promise of being a legitimate payment system for general use (apart from drug dealers, ransomware hackers, illegal arms dealers, and money launderers).

I will report on full year returns for 2024 in more detail in a few days.

Thank you for your time – please send me feedback and/or ideas for future editions!

See also:

For my current views on asset classes and asset allocations - see:

Or visit my web-site for 100+ recent fact-based articles on a wide range of relevant topics for inquisitive long-term investors.

Asset classes and sectors, and benchmark index for each:

|

Asset Class

|

Sector / Segment

|

Benchmark index

|

|

Australian Shares

|

ASX 200 (including franking credits)

|

S&P/ASX200 Franking Credit Adjusted Tax-Exempt TR

|

|

Australian Financials (‘banks’)

|

S&P/ASX 200 Financials Ex-A-REIT TR

|

|

Australian Resources (‘miners’)

|

S&P/ASX 200 Resources TR

|

|

Aust Small companies

|

S&P/ASX Small Ordinaries TR

|

|

Global shares

|

Developed World Shares Hedged

|

MSCI World 990100 net TR Hgd AUD

|

|

Developed World Shares Unhedged

|

MSCI World 990100 net TR AUD

|

|

Developed World Small companies Hedged

|

MSCI World Small Cap 106230 net TR

|

|

US Shares Unhedged

|

S&P500 TR AUD

|

|

Emerging Markets Shares Unhedged

|

MSCI Emerging Markets 891800 net TR in AUD

|

|

Property & Infrastructure

|

Australian REITs

|

S&P/ASX 200 A-REIT TR

|

|

Aust Unlisted Property funds

|

MSCI Mercer Australian Core W/s PFI and predecessors

|

|

Global REITs Hedged

|

FTSE EPRA Nareit Developed ex Australia Rental Index AUD Hedged - TRAHRA

|

|

Global listed Infrastructure Hedged

|

FTSE Developed Core Infra 50/50 Hgd AUD FDCICAHN

|

|

Alternatives

|

Global Hedge Funds Unhedged

|

HFRI Fund-weighted Composite index AUD

|

|

Gold Unhedged AUD

|

London PM Fix in spot AUD

|

|

USD cash (unhedged AUD)

|

US 3m T-Bills in AUD

|

|

Fixed/floating income (debt)

|

Australian Government bonds

|

Bloomberg AusBond Treasury 0+ Yr Index

|

|

Australian investment grade Corporate Bonds

|

iBoxx AUD Corporates Yield Plus Mid Price Index

|

|

Global Government bonds Hedged

|

Bloomberg Global Treasury Scaled Index Hgd AUD

|

|

Global investment grade Corp bonds Hedged

|

Bloomberg Global Aggregate Corporate and Government-Related Scaled Index Hgd AUD

|

|

Global High Yield bonds Hedged

|

Markit iBoxx Global Developed Markets Liquid High Yield Capped Index (AUD Hedged)

|

|

Emerging Markets Bonds Hedged

|

J.P. Morgan EMBI Global Core Index (AUD Hedged)

|

|

Australian Hybrids (grossed up)

|

Solactive Australian Hybrid Securities Index (Gross)

|

|

Cash

|

Australian Cash

|

RBA cash target

|

‘Till next time, happy investing!