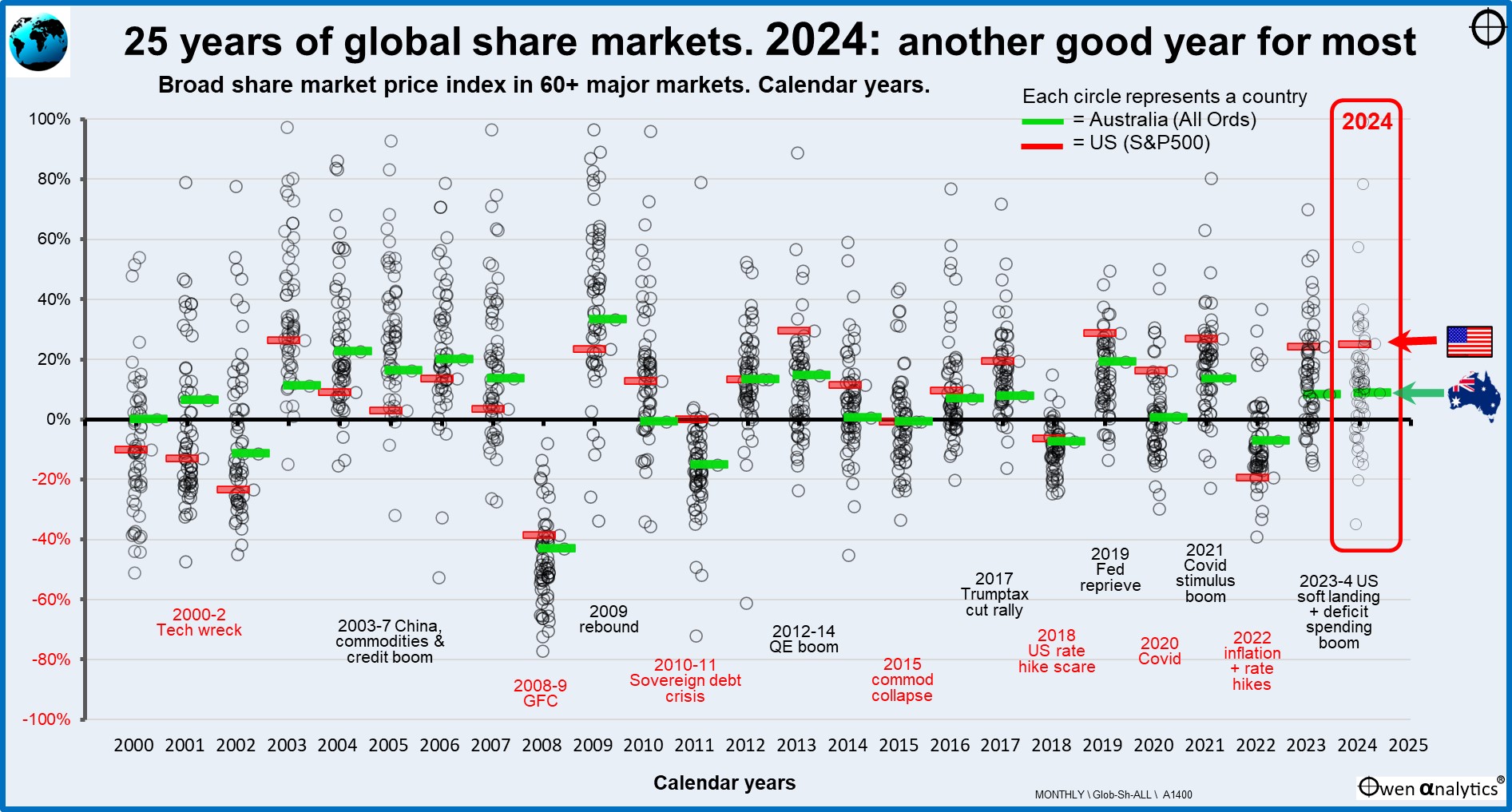

- 80% of share markets were up again in 2024, and most were above their historical averages.

- This is despite the constant chorus of dire predictions by economists everywhere of imminent recession and rapid rate cuts, and equally tiresome predictions by commentators of imminent market crash,

- So was NOT just ‘US big-tech’ lifting the world’ which is the current media nonsense.

- Almost everywhere is up in the broad global rally!

Today’s chart shows gains/losses per calendar year since the start of this century for the main broad share local market price index in local currencies for 60+ major global share markets I cover.

Each circle represents a country share market. In each year I have highlighted the US (S&P500) as red bars, and Australia (All Ordinaries index) as green bars.

2024 – another great year

2024 was another great year – with 80% of share markets in positive territory, and most were above their historical averages. So it is NOT just a case of the ‘US big-tech lifting the world’ which is the current media nonsense. Almost everywhere is up in the broad global rally.

Recall that the majority of economists around the world have been repeatedly predicting US/global recessions over the past two years. Fortunately, we don’t let economists manage actual money!

Best & Worst

Best in 2024 were Pakistan +84% and Cyprus +57% (although Cyprus is still well below its pre-GFC and pre-2014 banking crisis peak, but is now recovering at last).

Off the chart (literally and figuratively) are Argentina +177%, and Venezuela +99% but those are affected by high inflation (around 160% and 25% inflation respectively).

Worst in 2024 were Latvia -35%, Russia (RTS) -20%.

Only a handful of countries were negative in 2024 – mainly for reasons main affecting the dominant stock/s in each country. Brazil (weaker iron ore & oil), South Korea (Samsung Elec scandals, plus political crisis), Saudi Arabia (oil down), Estonia & Finland (Russian orbit), Denmark (Ozempic maker Novo Nordisk down on disappointing weight loss results), France (weak luxury brands in China).

The US has had another cracking 20%+ year after a similar result in 2023.

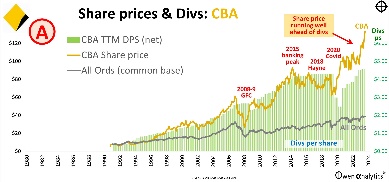

Australia is heading for another (slightly) above average year (price index up +8%, total returns +12%) – with weak miners (falling iron ore price) offset by strong banks (Why did banks soar? Who knows!) see: CBA in 7 charts

Australia has lagged the US again in 2024, and has lagged the US in nine out of the last ten years (2022 was the only exception when Australia sold off less than the US in the 2022 rate hike sell-off).

Can the boom extend into another year in 2025?

With two very good years in 2023 and 2024 in the bag, led by the strong US market, surely we can’t expect the rally to last into a third year? (Even after two years of bad forecasts, market commentators are still falling over themselves predicting an imminent crash!)

Why not? We’ve seen plenty of prior booms that ran for longer – for example:

- 2019-20-21 - three great years for the US market, despite the fact that 2020 had the sharpest and deepest US and global economic recessions since the 1930s.

- 2012-3-4 - another recent rally of three good years in a row (thanks to QE & ZIRP).

- 2003-4-5-6-7 – four positive years (China/credit boom).

Going back further –

- 1995-6-7-8-9 – five positive years in a row – each 20% or better (‘dot-com’ boom).

- 1982-3-4-5-6-7-8-9 – eight positive years in a row (deregulation, take-overs, despite the 1987 crash).

Big booms always end in big collapses

Each of those long multi-year rallies was followed by a big crash of course, but that is what happens. Booms never deflate slowly and return calmly back to ‘fair price’. Financial markets always lurch from wild swings on the upside to wild swings on the downside because they are run by humans driven by wild emotions, not rational logic.

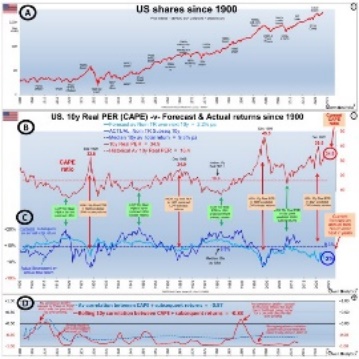

Yes, we all know the US market is very expensive, but share market booms don’t collapse because, or when, they are expensive. Booms can run on for many years into even more expensive territory before they eventually collapse. The longer and higher the boom, the bigger the eventual collapse. We are into one of those long, over-priced booms now.

Will 2025 be the year the current boom collapses (Trump trade wars? inflation revival? military flare-up? US defaulting on debt?), or will US tax cuts, deficit spending, and deregulation keep the rally going for another year?

What to do?

What NOT to do is easy - Don’t listen to pontificating economists (they are downright dangerous. Economists can’t even predict the past, let alone the future!). Don’t listen to shrill market/media commentators (they don’t have actual money on the line and/or are pushing a product). Don’t follow the crowd – in either panic buying/gearing-up/doubling-down if prices suddenly rise ('FOMO' - Fear of Missing Out), or panic selling if prices fall suddenly ('FOLE' - Fear of Losing Everything).

What to do? Stick to your/(client) strategy, re-assess and re-confirm goals, needs, risk tolerance, cash flow requirements, adjust for any material changes in personal/family circumstances (health, births, deaths, marriages, divorces, etc), continually re-assess pricing against underlying fundamental value, be prepared to take profits and/or pick up bargains when opportunities present themselves. This is what volatility is for!

‘Till next time, safe investing!

For more on the over-pricing of the US share market – see:

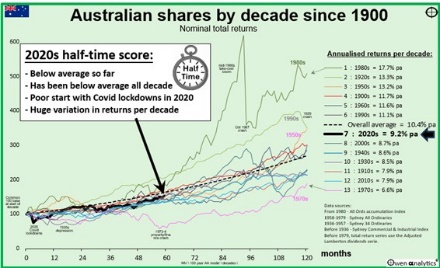

On Australian share market – see:

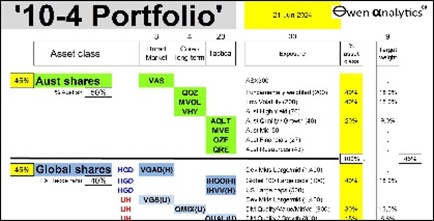

For my current portfolio views and asset allocation in my own long term ETF portfolio (I have been over-weight US / global shares) – see