Greetings friends! - Here’s my snapshot on global markets for Aussie investors – including my Top 5 factors moving markets.

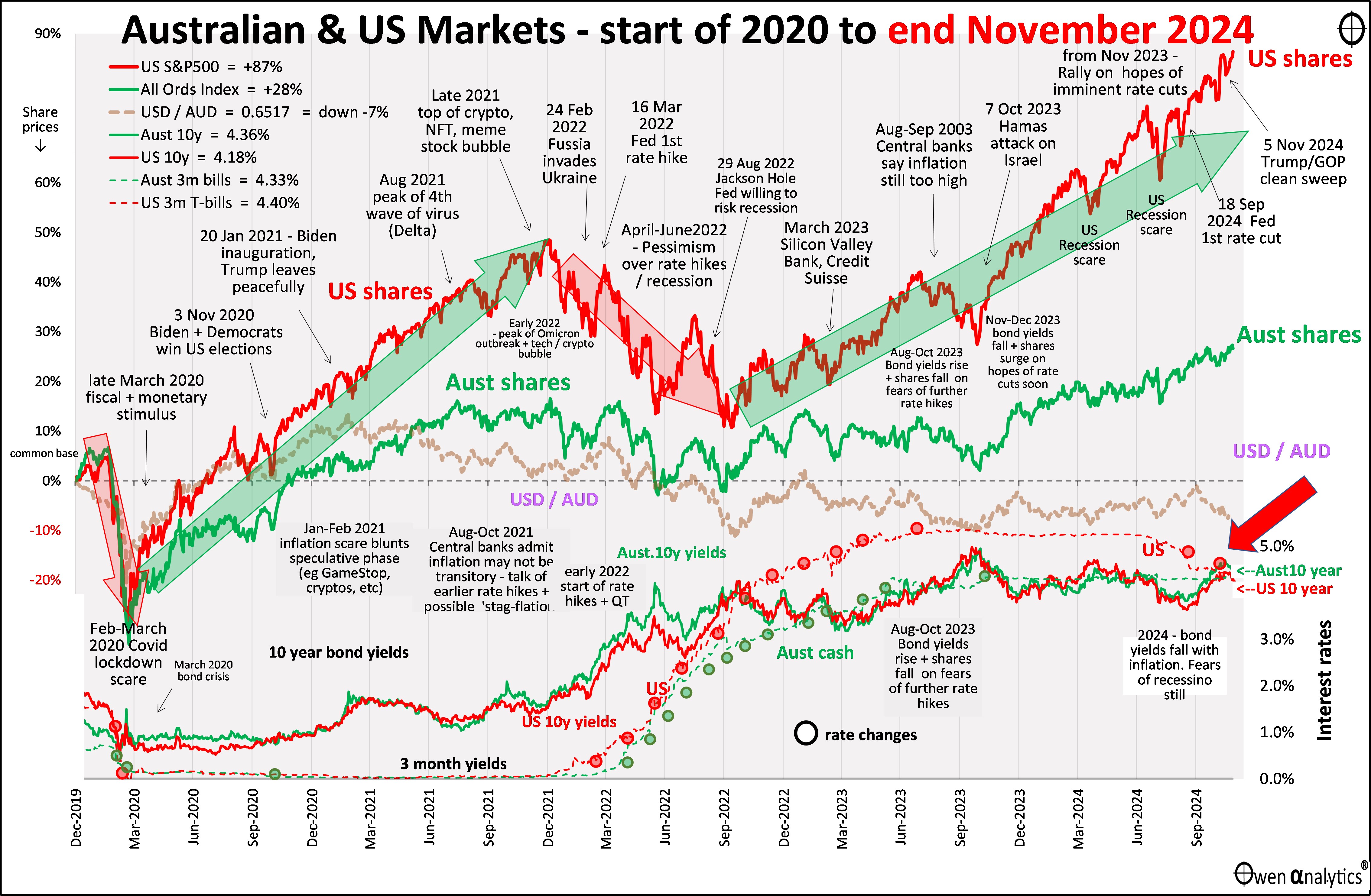

First - my essential 1-page snapshot chart - covering Australian and US share markets, short and long-term interest rates, inflation, and the AUD/USD exchange rate.

As usual, there are two versions – first is the traditional version on a single chart:

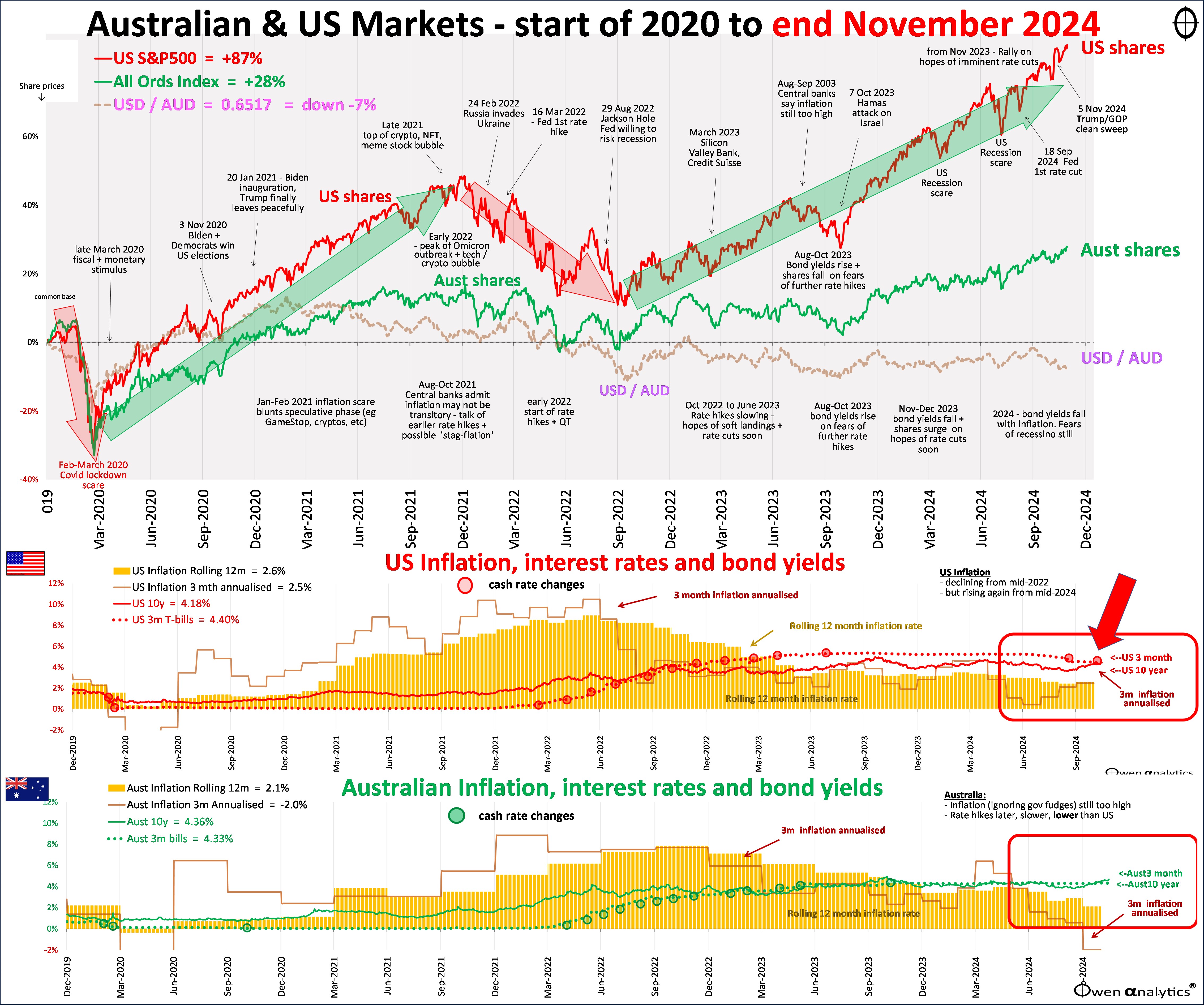

Also the alternate version below, requested and used by several advisers - showing Australian and US inflation in the lower sections.

Here are my Top 5 factors moving investment markets in November:

1. Trump

The stand-out event that dominated all headlines and investment markets in November was the US election outcomes – with a Republican clean sweep of the White House, Senate, and House of Reps. With this, Trump’s policies will probably have few challenges or difficulties being legislated by Congress.

Equally newsworthy were Trump’s early nominations for key cabinet posts, and also his statements outlining early policy proposals. Much has been written about these by myself and others, so I will not cover them here. This report is about what happened in investment markets and why. My only comment and prediction would be that Trump’s second term will probably be a continuation of the revolving door circus he presided over in his first term. It will be a laugh-a-minute circus, just like last time.

Trump’s Tariffs

Probably the most market-moving announcement was Trump’s plan to slap 25% tariffs on all imports from Canada and Mexico (apparently linked to measures to reduce the cross-border drug trade), plus 10-20% tariffs on every other country in the world, plus an additional 10% tariff on China (presumably on top of the 60% already announced).

[In breaking news, I heard just now that Trump has promised 100% tariffs on BRIC countries (Brazil, Russia, India, China) plus a handful of other emerging nations. It’s going to be a wild ride!]

Share markets appear to have completely brushed off Trump’s proposed tariff hikes. However, while studying US company results over the past couple of weeks I have observed some broker/analyst earnings outlooks for the US tech giants come off a little late in the month. These downgrades have yet to factor into share prices.

US dollar policy versus tariffs

Bond yields also fell back toward the end of the month – a sign of possible slower US and global growth ahead. This was mirrored in a surge in the US dollar on currency markets. The last thing Trump needs is a strong dollar. That would increase pressure for even more tariff protection to assist US companies. The US dollar has risen 7.5% so far this year against its trading partner currency basket – that effectively neutralises three quarters of the proposed 10% tariff across the board. Tariffs lose their power if the dollar keeps rising. All tariffs do is increase domestic prices and inflation, and invite retaliation which could trigger a deep global recession.

Instead of increasing tariff barriers and protective subsidies, a much more effective solution would be to abandon the ‘strong dollar policy’ America has adopted since the late 1990, which has hurt America’s competitiveness, driven huge trade deficits, and hollowed out US manufacturing (contributing to the rise of Trump’s disaffected working class voter base in the rust-belt states). But that is another story for another day!

2. Share markets up + set for another great year

After a weak October due to election uncertainty, November was another strong month for share markets around the world, resuming the strong general run-up this year. Best for the month were Canada (TSX Comp +6.5%) and USA (S&P500 +5.7%), but European markets were mostly down on continuing weakness in demand for luxury brands, especially in China.

In the US it was very much the ‘Trump Trade’. The biggest gainer was Tesla (up +38%) following Trump’s nomination of Elon Musk to head a new government cost-cutting department. This is the start of a whole new era of crony capitalism that would make Ferdinand Marcos envious!

Oil & gas stocks were up on Trump’s ‘drill, baby, drill!’ rhetoric. Banks, industrials, tech, and social media were up on hopes of widespread cuts to regulations. The only negative sector for the month was health care, following Trump’s appointment of an anti-vaxer, anti-flouride, anti-big-pharma RFK Junior to head Health and Human Services.

The local Australian share market was also up 3% for the month. Continuing this year’s theme, the big banks were stronger (led by CBA up another 11% into genuine la-la land), while miners were down virtually across the board.

With only one month to go, 2024 looks like being another cracking year for global share investors. A bunch of markets are up by more than 20% so far this year - including the US, Canada, Taiwan, Slovenia, Croatia, Hungary, Cyprus, Turkey, Egupt, Nigeria, Kenya, and Pakistan. A couple of dozen more are up between 10% and 20%.

One of those is Australia, placing well behind the leaders for the year, but still on track for a moderately above-average year in 2024. The big drag on the local ASX market this year has been the big miners, hurt by collapsing commodities prices, mainly due to a combination of over-supply and weak global and Chinese demand.

There are only a few countries posting negative share market returns this year – notably Russia, its close neighbours Latvia, Estonia and Finland, and also down are Mexico, Brazil, South Korea, Slovakia, Portugal and France.

3 - Interest rates and inflation – down everywhere but here

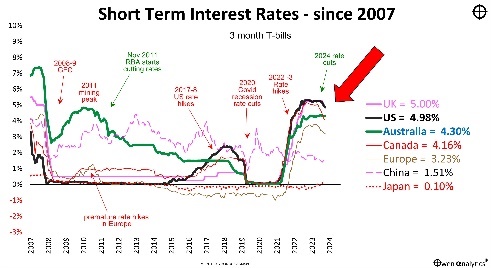

Rate cuts contine around the world as inflation eases, economies show signs of slowing, and jobs markets weaken. On 7th November the US Fed made its second rate cut for the cycle. Over the past couple of years, most economists everywhere have been predicting a US recession and rapid Fed rate cuts, but they have been consistenly wrong with both of these predictions. (They are related of course – a deep recession would normally be the trigger for rapid and aggressive rate cuts). But the US economy has remanied robust and the Fed has been cautious in cutting rates. (This year I have been bullish on global shares and US in particular.)

On the same day the Bank of England also made its second rate cut. Canada has had 4 rate cuts so far.

Meanwhile in Australia the RBA is still not going to start its long predicted rate cuts until into next year. Why? Simple. It’s not rocket surgery! As I have pointed out many times, the RBA does not need to cut rates! Rates are currently not ‘high’, inflation is still above target range, the economy is still running above capacity, and unemployment is not high enough to slow spending. Why would it cut rates in those conditions?

Despite several rate cuts in US, UK, and Canada, their cash rates are still higher than Australia, but their inflation is lower than ours. Why?

Again its simple. When the RBA eventually woke up and started hiking interest rates to attack inflation here, it went too late, too slow, and too low with rate hikes. The RBA chose to allow inflation to run higher for longer, and therefore interest rates will also need to be ‘higher’ for longer.

(Actually they are not really ‘high’ at all, relative to historical averages, nor relative to inflation, nor relative to the rest of the world.)

See my recent report on inflation and interest rates in Australia versus other major countries, see:

Adding to the problem now is the Labor government’s attack on the RBA. The government rushed through new legislation a couple of nights ago that splits the current RBA board function into two separate boards – one for setting interest rates, and one for governance. We wait with keen interest to see whom Smiling Jim Charmer (without doubt Australia’s worst Treasurer since Jim Cairns) nominates for the roles. So far during his term as Treasurer, 100% of his RBA Board appointments have been union bosses to appease Labor’s union masters / funders. Fact.

3 - Bonds

Treasury yields rose early in the month, then headed back down again late in the month. Yields ended down a whisker in Australia, virtually flat in the US, and down by between -0.1% to -0.2% in Europe. The most likely cause was a ratcheting up of fears over economic slowdowns, in parallel with Trump’s ratcheting up his proposed tariffs.

Government bonds are heading for another poor year in 2024, but probably not as bad as 2021 and 2022, which was the worst year for bond returns in a century.

Corporate bonds have done better, posting modest positive returns as credit spreads have tightened even further to very tight levels now (reflecting declining perceived risk of recessions). This is not consistent with the tariff war fears!

4 - Commodities slump continues

While each commodity has its own uniqe cycle, most industrial commodities prices are down this year. On the demand side – demand has been weak due to slowing economies after the aggressive rate hikes in 2021-2 to tackle inflation, plus weakening demand for EVs in Europe and the US. On top of that we now have the very real prospect of a trade-war induced global slowdown.

Adding to slow demand, on the supply side we have over-production and/or over-investment in several commodities markets, especially nickel and lithium. Specialist ASX mining shares are down heavily this year.

There have been two main exceptions in this generally gloomy commodities picture – gold and bitcoin. So far in 2024, gold is up 28%, but Bitcoin is up 128%!

One bitcoin is now the same price as 1 kilogram of pure gold!

5 – Gold & Bitcoin shine – which is better?

I can see at least four common themes driving the strong interest and demand for both gold and Bitcoin this year:

- Fear of US gov deficits / debt (US is still running 6% decifits and federal debt just hit $36 trillion!)

- Fear of US inflation – especially if Trump heavies the Fed into cutting rates lower than it otherwise would

- Fear of US political unrest (could be a range of triggers under Trump)

- Fear of a declining US dollar (due to debt, default, inflation)

These are genuine fears (but I personally don’t share the 4th fear on the list), and they are no doubt behind the rise of both gold and bitcoin over the past year.

Bitcoin has also had the added boost since Trump’s election as he has promised to make America crypto-friendly, whatever that means. Some brief comments about each:

Gold

I have studied gold in great depth over the past 40 years, and I have found that it is mostly not the ‘inflation hedge’ it is believed to be. At times the gold price has gone through massive bubbles and busts that have taken decades to recover in past cycles. However, gold does have valuable uses in portfolios from time time, and I have used it in client portfolios (and my own) on occasion with great effect.

For example, I have had a gold ETF in my ’All-weather 10-4 ETF portfolio’ this year, and it has been the best performing asset class for the year, further boosted by the 5% decline in the AUD against the USD.

This is certainly NOT a recommendation to buy gold now. All I am saying is that there are times it makes sense, and one of those times was in 2024. See my recent paper on gold:

Bitcoin

The flood of money into the numerous new Bitcoin ETFs approved since the beginning of 2024 has no doubt accelerated the price rise this year. I don’t own any Bitcoin (nor any other crypto or crypto-related things).

However the idea of Bitcoin does have legs. The ideas behind Bitcoin are very powerful and compelling – the idea of keeping your financial affairs like income and payments secret and anonymous, completely outside the reach of banks, intermediaries, governments, police, taxes, regulations, and away from the prying eyes of countless meddling agencies and departments across all levels of government.

That would certainly be a wonderful idea. The problem is that operating outside the reach of governments also means no regulations, no consumer protection laws, no fidelity funds, and no deposit guarantees. It’s back to a wild west world where hackers, thieves, scammers, fraudsters, and market maniputors can operate with secrecy and impunity. Countless people have lost money in the crypto universe and they have no idea where to start looking nor where to go for help.

Who knows how Bitcoin will turn out? It may end up as a new form of money that is used widely by everyday folk around the world for everyday transactions, instead of using government fiat paper money.

Or it may turn out like the every other speculative bubble in history – from Dutch tulips in the 1630s, to dot-com shares in the 1990s. I am happy to sit and watch from a safe distance for now!

Meanwhile, ask yourself – would you rather own 1 Bitcoin, or one kilogram (32.15 troy ounces) of pure gold?

(Personally, I would go for gold)

Question2: if you had a spare A$150k lying around, would you buy 1 Bitcoin, or one kg of gold, or something else?

(Personally, I would do something else – add it to my ‘All-weather 10-4 ETF portfolio’ of course!)

‘Till next time – safe investing!

Some further reading:

Here is my fact-based assessment of the actual economic outcomes under the Trump and Biden presidencies, see:

For my current views on asset classes and asset allocations in my actual long-term ETF portfolio - see:

Plus check out my web site for 100+ of topical articles on a host of issues affecting investors and investing.