On 22 May, RBA Deputy Governor Andrew Hauser gave a key-note address outlining his observations from his trip to China in the middle of April, days after Trump launched his ‘Liberation Day’ tariff war on the world, aimed primarily at China.

As China is by far our largest export buyer, it is our largest source of export and tax revenues, and has been the largest source of wealth and prosperity for Australians so far this century, he was keen to assess first-hand the likely flow-on effects of the trade war on the Australian economy, and the RBA’s monetary policy thinking.

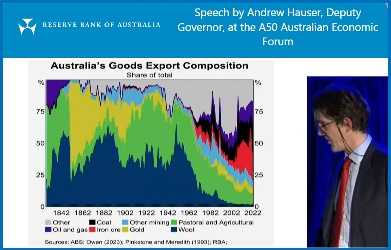

The Dep Gov needed a killer chart to open his address, and I am once again incredibly honoured that he contacted me for permission to use another of my charts.

The chart was from an article I wrote in 2024 about Australia’s changing trade patterns and their geo-political implications - Geopolitics case study - China: our largest export customer but also perhaps our greatest potential military threat? Is this a problem? (3-July-2024)

The title of Hauser’s address this week was from an old Mandarin saying:

“Open the Door and See the Mountain: Reflections from a Recent Trip to China”,

or Hauser’s punchier summary: “Don’t count China out!”

Link to speech transcript

Link to speech video

In it he outlines four key themes –

-

-

- The first is that, before Trump’s Liberation Day tariffs, there was a general feeling of optimism in China that the economy was finally turning the corner, after the traumas of the extended Covid lockdowns and the collapse of the property / construction market.

- Second - the ‘Liberation Day’ tariff onslaught came as a genuine shock to the Chinese people and government. There are expectations that the economic result could be in the order of a 1.5% to 2% drop in overall Chinese GDP in 2025. In Hauser’s words, “These are big numbers”, and his take is that there is a widespread view across China that the CCP will be highly motivated to do almost anything to prevent such a slowdown.

- Third – there is a strong belief within China that China is relatively well-placed to weather the tariff war storm. It has ample capacity for fiscal stimulus, and there is a strong belief in the willingness to use it to stimulate activity if necessary.

There is also a view that the US needs China more than China needs the US (in trade terms anyway), so that the burden of the tariffs will probably be borne mostly by US importers and/or consumers, rather than Chinese exporters.

Graph 2 (RBA’s not mine) highlights the differences in market power of US-China for the different types of items the US imports from China. It is a very powerful and truly remarkable chart (although I would like to see more colour!)

-

-

- The fourth theme is that Australian companies (at least for the firms that took part in the discussions in China) are seeing more upside than downside for Australia. They see Chinese steel production (and demand for Australian iron ore and coking coal) holding up at around 1 billion tonnes per year, with a continued shift from residential construction to infrastructure. In addition, they see flow-on benefits for many types of Australian firms, from continued monetary and fiscal policy stimulus from Beijing.

The tariff war is an ever-changing drama of course, and it is early days yet. There will probably be a lot more drama and whip-saw changes ahead, so only time will tell how the implications for Australia unfold.

But it was good that the RBA is keeping close to the action on the ground, and that I was a small part of it!

‘Till next time. . . .safe investing!

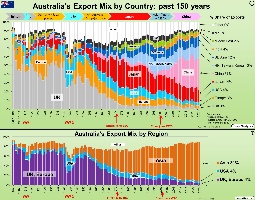

My original article on Australia’s changing trade patterns and geo-politics

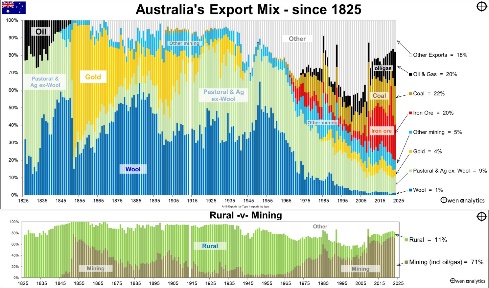

For my big picture on Australia’s changing patterns of exports by type:

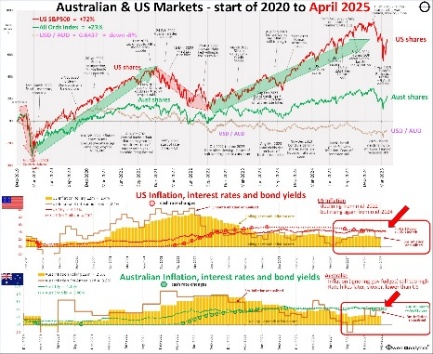

For my most recent monthly update on global markets for Aussie investors: