China’s 4-year trade war with Australia is over. What was the impact? Very positive overall!

- It was a much-needed wake-up call for Aussie exporters to quickly diversify into other markets to reduce their heavy reliance on China.

- China’s share of Australia’s exports has fallen from 42% to 32%, taken up by increasing exports to the rest of Asia, and the USA.

- Australia’s exports continued to boom, delivering record dividends to Australian shareholders, and enormous boosts to tax revenues for Federal and State governments in 2022, 2023, and 2024.

Trade attack from our biggest export customer!

China is Australia’s largest export customer, and exports to China have been the single largest contributor to our national revenues, wealth, and living standards this century.

But then suddenly, our largest export buyer slapped trade bans on $20b per year of our exports. The trade war lasted four years. Plus there was Covid, during which China’s lockdowns where the longest and harshest in the world. China’s property / construction / finance boom collapsed, and its economy has stalled.

What was the impact of all this on Australia’s exports? Despite early fears of impending doom & gloom (‘it’s the end of the world’ – again!), the overall result for Australian exports has been better than anybody could have expected. This is the story of what happened and why.

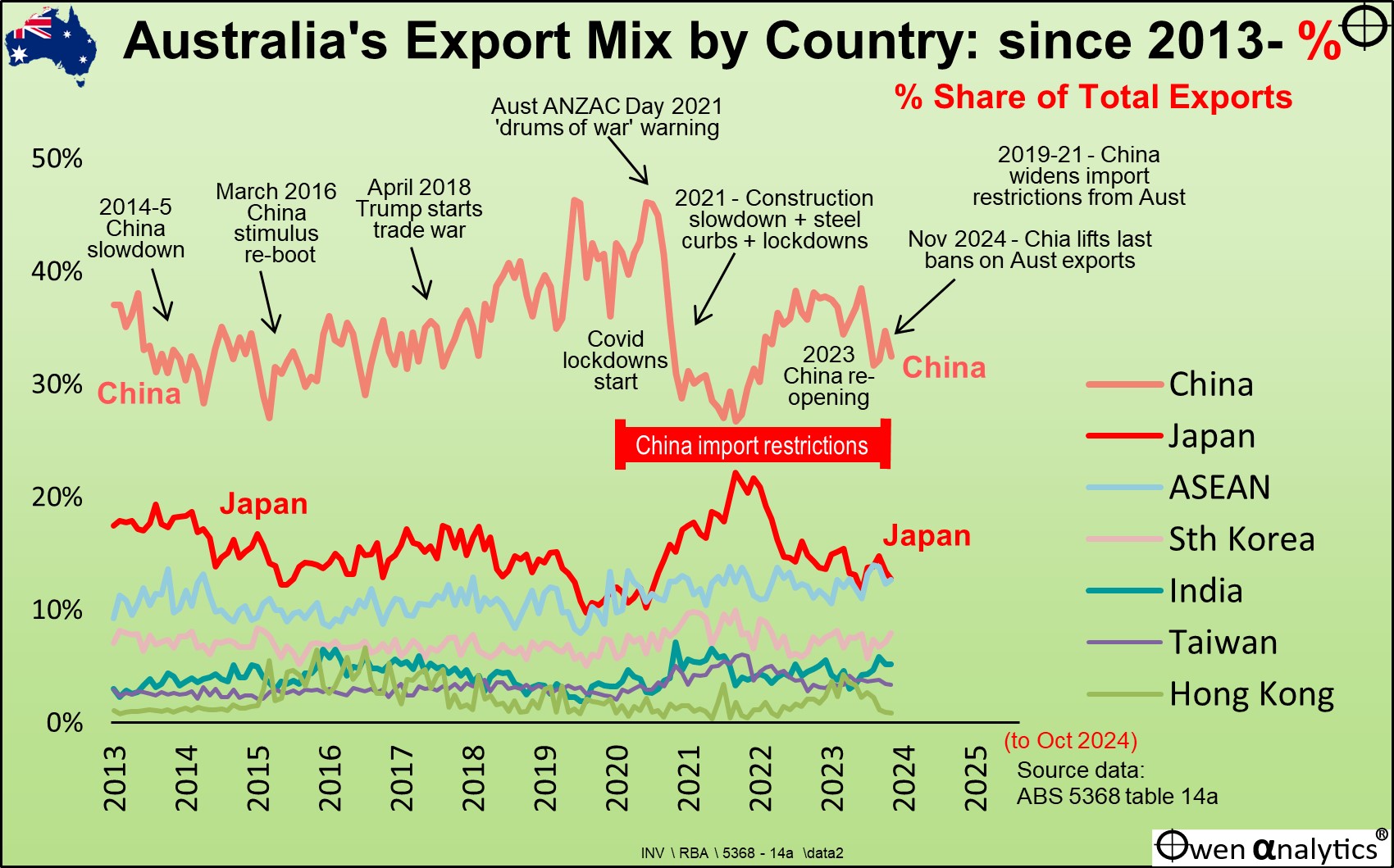

The first chart shows export volume shares to Asian countries since 2013 (70% of our exports go to Asia):

China has been our largest export buyer since it overtook Japan in 2010, and China had been increasing its dominance of our export mix until hit by Covid and the 2020-24 trade war. Since then, China’s share of our exports has reduced significantly, while the share of exports to the rest of Asia has risen.

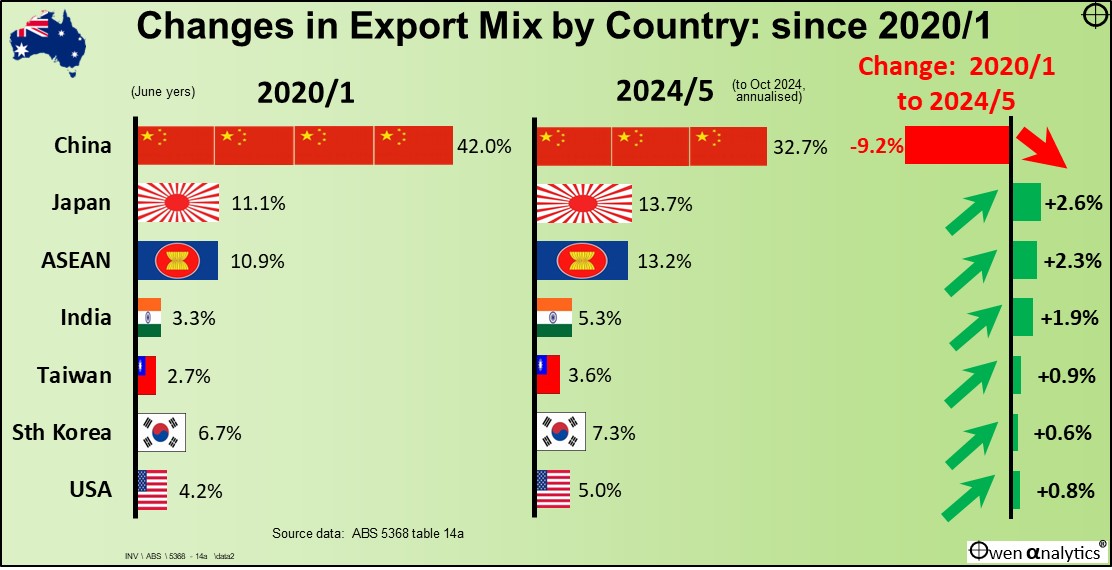

The second chart shows how the share of exports to our major export buyers has changed from 2020/1 to now.

(Here I use June years as this aligns with the main economic measures in Australia – eg. federal budget, GDP etc. Data is to October 2024, annualised for the current 2024/5 year.)

China’s share of our exports has declined from 42% to 33%, but the export shares to the rest of Asia have risen. (ASEAN includes Malaysia, Thailand, Philippines, and Indonesia).

The other big gainer has been the US of A, and we are only at the beginning of the great American re-on-shoring of industry. This mega-trend was started by Biden, and looks like being accelerated by Trump. Guess what? They need rocks, and we do rocks!

Back to how the story started

Up until Covid and the trade war hit, having one dominant export buyer was seen as a good thing. Exporters just focused on ‘the China trade’ and they didn’t really need to pursue other markets. However, relying heavily on just big customer was risky – and when China attacked our imports it was a rude shock for many un-prepared Australian companies.

Covid impact – unexpected boost for exports!

The Covid lockdowns hit trade volumes around the world. Australia’s overall exports fell, but the impact on exports was less here than in many other exporting nations. Our deepest decline in total export revenues was just -17% between August 2019 and August 2020. This was rather mild in global terms. Why?

Our State governments locked citizens in the cities in their homes and out of their schools and businesses for months on end, but they were smart enough to keep their mines and ports open, to keep exports flowing out and revenues flowing in.

As a result, during the Covid lockdowns in 2020-1, Australia overtook Brazil to become the world’s largest iron exporter, and it also overtook South Africa to become the world’s largest coal exporter. A year later, during the oil & gas crisis following the Russia’s invasion of Ukraine, Australia also overtook Qatar to become the world’s largest LNG exporter.

Never let a good crisis go to waste!

How did the trade war start?

Diplomatic tensions between Australia and China had been escalating rapidly from early-mid 2018 when PM Scott Morrison started echoing and doubling down on Trump’s rhetoric against China when Trump slapped his tariffs on China from April 2018. Just silly and unnecessary.

In addition there were several actions by Australia between 2018 and 2020 that upset China, including:

- Australia’s crackdown on foreign investment from China, on national security fears,

- Investigations by Australia’s Anti-dumping Commission into a range of products and exporters, including China,

- Australia’s foreign interference laws introduced in 2018-2020 – including the National Security Legislation Amendment (Espionage and Foreign Interference) Act, the Foreign Influence Transparency Scheme Act, and the Foreign Relations (State and Territory Arrangements) Act,

- Australia banning Huawei from the new 5G network rollout (August 2018), going further than the other ‘Five-Eyes’ countries,

- Morrison calling for international investigations into origin and cause of the Covid-19 outbreak.

- ‘Drums of war’ comments by a senior Australian security official on ANZAC Day 2021 – warning of impending war with China.

What exports were targeted?

From early 2020, China reacted to what it saw as rising hostility toward it by starting to impose restrictions and bans on a range of Australian exports totalling around $20b per year. (about 5% of exports, or 15% of exports to China).

The exports affected included Australian barley, beef, cotton, lobsters, timber, and wine. In addition there were also unofficial restrictions on other major exports, notably coal. There were also several alarmist announcements within China warning citizens against studying or holidaying in Australia. (Pre-Covid, Sydney streets were full of Chinese tourists. Today, well after borders have been re-opened, Chinese tourists are nowhere near their pre-Covid numbers.)

How did the trade war end?

Trade and diplomatic relations between the two countries started to thaw after the Morrison government was defeated in 2022. China started easing the restrictions progressively during 2023, and the last of the bans were lifted in October 2024 (lobsters) and late November (beef).

Conclusion

- The 2020-2024 mini-trade war with China, although alarming at the start, turned out to be the necessary wake-up call for Aussie exporters to urgently diversify away from their increasingly dominant sole customer – China.

- Never under-estimate the ability of companies and governments to pivot when required by changing global conditions. People (and investors) tend to assume current conditions will continue forever, and they (we) tend to panic when the existing order is disrupted. We tend to underestimate the ability of company boards and governments to pivot in the face of crisis. They are not perfect of course, and there may be a fair bit of ‘trial & error', but it is probably not the ‘end of the world!’

- China needs Australia more than Australia needs China! In response to rising hostilities and rhetoric, China started hitting trivial ‘non-core’ items (wine, lobsters, beef, etc), but made sure it kept importing what it really needed – iron ore and coking coal from Australia, to keep those aging steel mills running and the workers quiet and compliant.

- China has been desperately searching for alternative iron ore suppliers but so far has been unsuccessful (Guinea is still a long way away yet, to be operated by RIO hopefully). Also, China (via its SOEs) is the largest shareholders in its iron ore suppliers BHP, RIO, and FMG. Aussie shareholders in our big exporters are just basically going along the ride, while China calls the shots. Xi knows what is in China’s best interest.

Bottom line – I am bullish medium term on Aussie miners and industrial commodities (beyond the usual short-term cyclical demand-supply cycles), given the global arms build-up, and re-on-shoring / protectionist mega-trend.

Further reading –

For the full picture on Australia’s ability to pivot and prosper from global shifts in economic and military power over the past couple of centuries - Australians have been masters at turning geopolitical shifts and crises into economic advantage!

For the big picture on Australia’s diversity and flexibility in its types of resource exports -

On China’s role in our exports, see also:

‘Till next time – happy investing!

Thank you for your time – please send me feedback and/or ideas for future editions!