Key points:

- Australian and US share markets did well overall, despite heavy loss of life and attacks on our home soil.

- Volatile ride for shareholders, but patient holders ahead.

- Generally good for shares overall, limited only by war-time controls on profits and share prices.

In the first part of this story – ‘World War Two – Part 1 of 2: the outbreak’ we saw how, although the lead-up to the War was negative for share markets, the actual outbreak of war itself was very positive for share prices overall, and especially for mining shares.

The rest of the War was also good for Australian shares, but not as good as it was for US shares. Australian shares would have done even better had they not been restricted by government war-time share price controls, which limited share price gains.

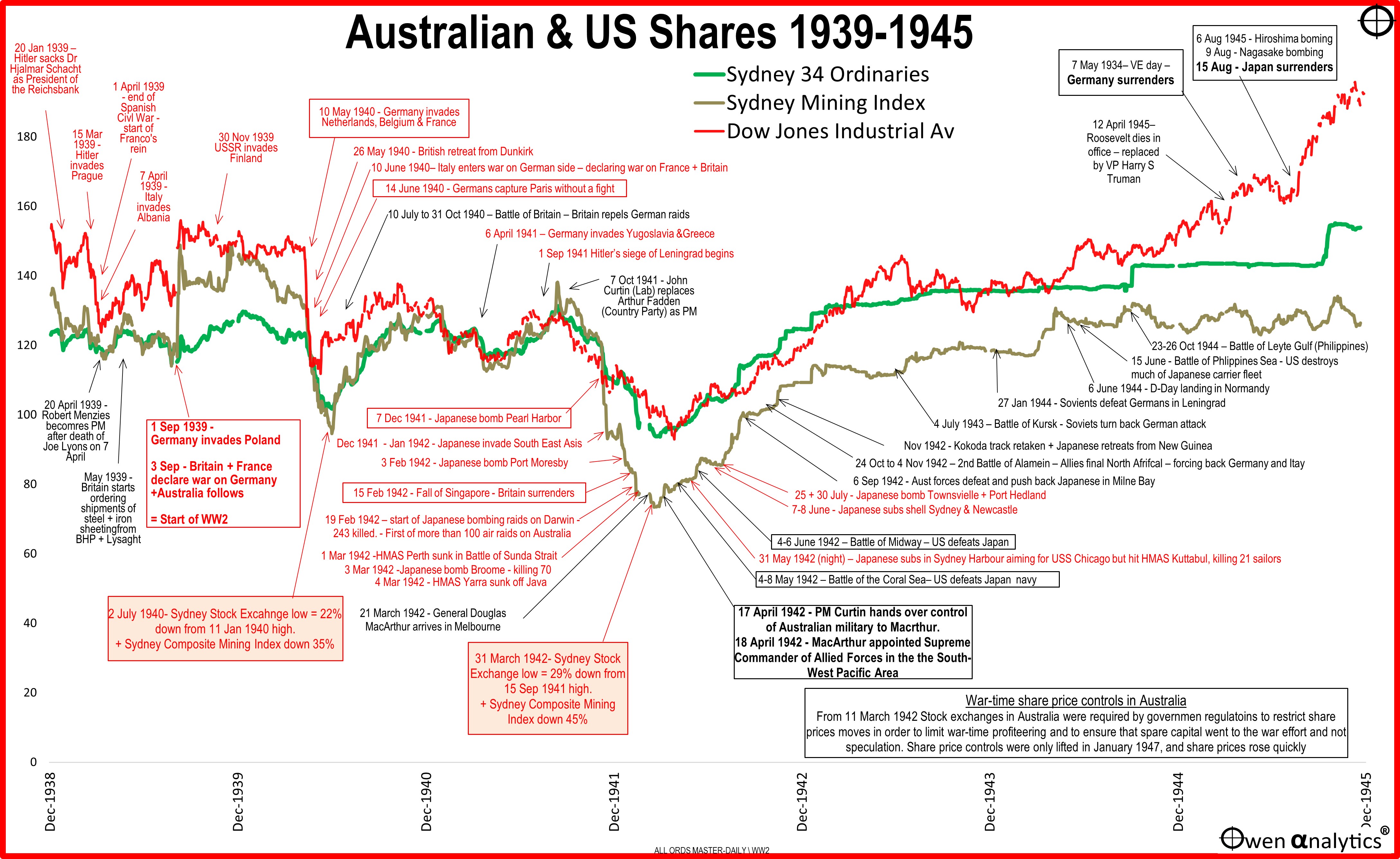

As in Part 1, this chart shows share indexes in Australia (green for the overall market, grey for the Sydney Mining index), and in the US (Dow Jones, in red).

War-time share price controls

From 11 March 1942, the Federal government in Australia directed all stock exchanges in Australia to limit share prices movements in order to limit war-time profiteering and to ensure spare capital went to finance the war effort instead of private speculation.

Profits in all companies were limited to their pre-war levels, and all excess company profits were literally siphoned off by the federal government to finance the war effort. Prices of Commonwealth bonds trading on stock exchanges were also controlled, to ensure that yields remained low so the government could continue to borrow cheaply to finance the war effort.

Labor got a taste for control

The Labor federal government became so enamoured with the war-time controls and the notion of government controlling all economic activity throughout the land, they were very reluctant to wind back government controls after the War ended.

For example, Labor even tried to nationalise all non-government-owned banks in Australia after the War (see Labor’s attempt to nationalise all banks in Australia! (21-7-2024). Although they failed in nationalising the banks, Labor (and also subsequent Liberal governments) retained heavy regulation of the banks for the next forty years.

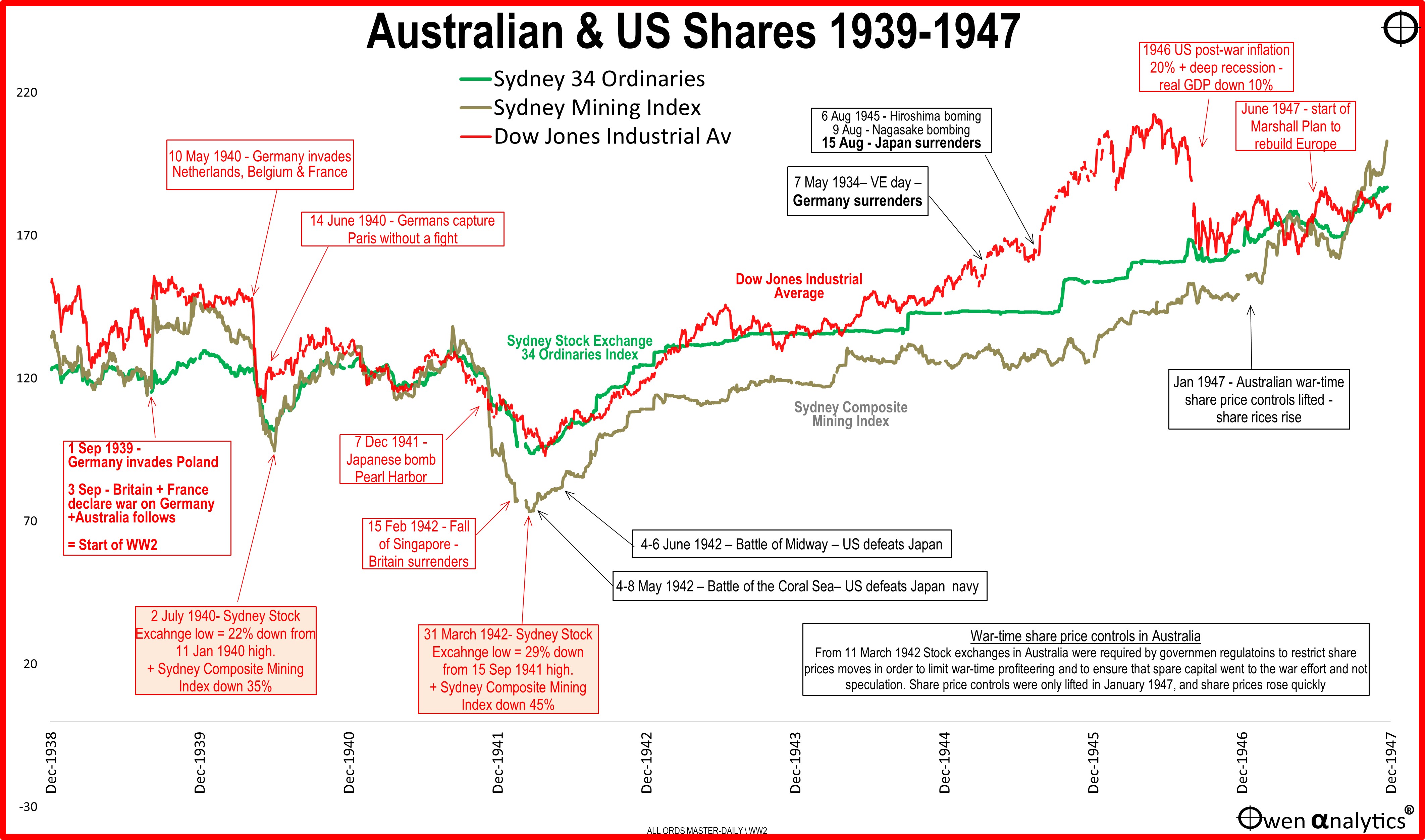

Controls finally lifted

The War ended in September 1945, but government share price controls were only lifted in January 1947. By that time, nearly all shares were sitting on their legal high limits, and prices shot up strongly when the limits were eventually removed. The local market eventually caught up to the US market in the Korean War.

Three phases of the War

Although the War overall was good for company profits and share prices, it was not all plain sailing for the share market. There were three main phases.

In the first phase up until late 1941, share prices in Australia (and the US) were more or less flat, with one sharp sell-off after the German invasion of Netherlands, Belgium and France on 10 May 1940, and the German capture of Paris without a fight on 15 June 1940.

Leningrad, Singapore, Pearl Harbor

In the second phase, share prices fell heavily after the German siege of Leningrad on 1 September 1941, and continued to fall with the Japanese advances down through Asia in late 1941, the bombing of Pearl Harbor on 7 December 1941, and the British surrender of Singapore on 15 February 1942.

The Japanese started bombing Darwin on 19th February 1942 and continued bombing raids across northern Australia for several months. The Japanese also sunk several Australian navy ships in battles in the seas surrounding northern Australia.

The low point for the Australian share market was 31 March 1942, with the overall index down 29% from the 15 September 1941 high, and down a total of 33% from the 11 March 1937 high.

Turning point

The third phase for the Australian share market was the strong rebound from right in the middle of the War. The turning point for the War, and share markets, was US General Douglas MacArthur’s arrival in Australia at the end of March 1942 as Supreme Commander of Allied Forces in the South-West Pacific Area. This was followed quickly by US victories in the Battle of the Coral Sea (4-8 May) and Battle of Midway (4-6 June).

War came right into Sydney on 31 May 1942 when three Japanese mini-subs entered Sydney Harbour and fired torpedos aiming for USS Chicago but hitting HMAS Kuttabul at Circular Quay, killing 21 sailors. It seems incredible looking back now, but confidence in the US command was running so high by that time, that the local share market shrugged off the Japanese submarine attack in Sydney Harbour and surged even higher!

Share prices in Australia and the US moved virtually in lockstep up until the government share price controls were imposed in Australia on 11 March 1942. The share price controls did allow share prices to rise (on government approval), and they remained close to the US market up until the middle of 1944, when US prices surged ahead of the Australian price gain limits.

Post-war share prices

The next chart extends to picture to the end of 1947. In Australia, share prices rose after the war-time share price restrictions were lifted in at the start of January 1947.

However, the US share market rose strongly after the surrender of Germany and Japan, but fell back sharply in the deep economic recession and 20%+ inflation spike at the end of the War. Both markets ended up with more or less the same overall net gains over the full period from the start of 1939 to the end of 1947.

Benefit of hindsight?

It is easy in hindsight to sit back now and say the share market was always going to recover because the US was always going to defeat Japan in Asia and defeat Germany in Europe. However, things would have been very different for Australians (and Australian investors) had Japan invaded Australia, confiscated all Australian assets, including shares and property, and turned Australia into a Japanese colony under Japanese law.

That outcome seems unlikely now, but we can appreciate how that may have been a real possibility at the time.

As it turned out, WW2 had mixed effects on the Australian economy, and was much less damaging than WW1 had been. Before WW1, Australia had been heavily reliant on exports for income, and also heavily reliant on imports of machinery and other essential manufactured goods. The closing of shipping lanes in WW1 was devastating to the local economy.

This experience in WW1 greatly accelerated national policies to protect and subsidise local industries to promote self-reliance. As a result, the local economy was significantly less affected by the time WW2 hit.

Overall, WW2 was very positive for the Australian share market, despite critical Australian shipping lanes coming under pressure from the Germans and Japanese, the Australian mainland coming under heavy bombing from the Japanese, and the devastating human toll for Australia (27,000 killed plus 23,000 wounded), and across the world (at least 70 million died, including some 50 million civilians).

A note on ethics

Investors who remained shareholders in companies through the war were not ‘profiting from human tragedy.’ They were providing essential capital required by companies to carry out manufacturing, mining, services, and supporting infrastructure across the economy to keep the country running when under attack.

See also:

On the impact of WW2 on Australia’s exports – see - Geopolitics case study - China: our largest export customer but also perhaps our greatest potential military threat? Is this a problem?

‘Till next time – stay safe!