With Trump in the White House for another four years it is impossible to predict which of his promised policies he will actually implement, nor even what he will do from one day to the next. Probably the most common piece of advice to investors appears to be along the lines of:

‘Get ready for another bumpy ride!’, or ‘Get ready for more Trump volatility!’

That may be the popular advice, and it makes great headlines - but it is based on media hysteria, not facts.

It felt volatile, but was it?

The Trump years certainly felt volatile. We all remember Trump’s first term. I would wake up every morning wondering what on earth he had said, or done, or ‘tweeted’ overnight. It was a four-year, non-stop, laugh-a-minute, roller-coaster ride that not even the most outrageous or creative comedy or fiction writer could possibly dream up. Who needs Harry Potter when you have Trump and his endless revolving door of opportunistic, sycophant courtiers. We would not even know who would be his press secretary this week!

It certainly was entertaining, but financial markets during Trump’s first term were actually very calm in historical terms.

The exception of course was the Covid lockdown crisis in early-mid 2020, which affected markets everywhere. But apart from that couple of months of extreme global volatility, the rest of the Trump years were actually relatively calm. Let’s look at the facts.

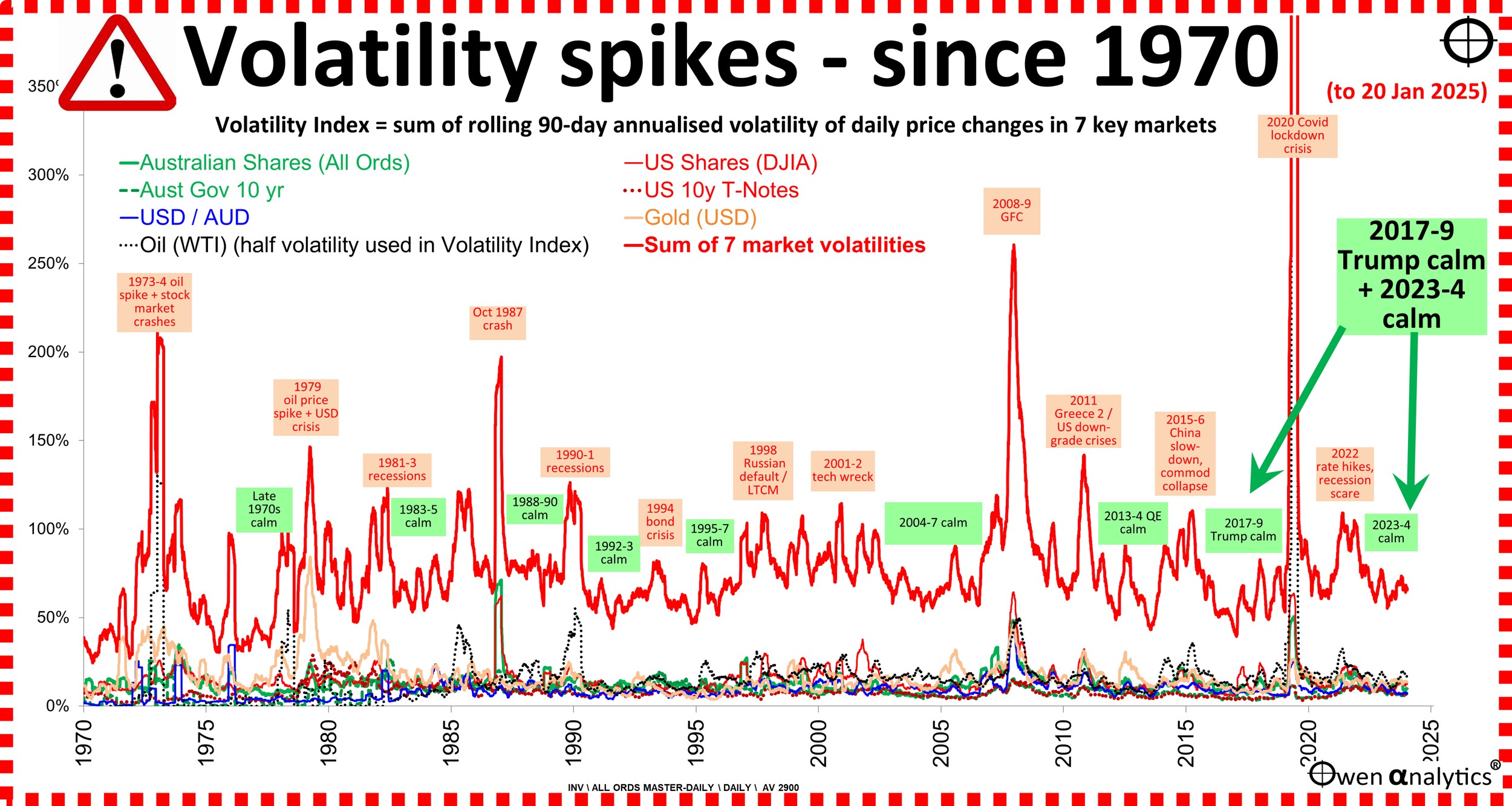

My Volatility Spike index

Today’s chart is my Volatility Spike index – showing the major spikes in financial market volatility since 1970.

This index is the sum of volatilities in seven key financial markets that are most important to Aussie investors - Australian shares, US shares, Australian government 10-year bonds, US 10-year Treasury notes, the USD/AUD exchange rate, Gold, and Oil.

Why gold? – because it is a good proxy for fears over inflation, government debt, political unrest, military conflicts.

Why oil? – because it is a good proxy for outlooks for global growth/recession, and is still a major component in inflation numbers, directly and indirectly.

Why bonds? – because they are good proxies for inflation and interest rate expectations, and they directly affect discount rates on which asset valuations are based.

Why the USD/AUD exchange rate? – because it is a proxy for global 'risk-on / risk-off' sentiment, and it directly impacts values of foreign assets for Aussie investors.

How the Volatility Spike index works

The volatility measure for each of the seven markets is the rolling 90-day annualised standard deviation of daily price changes. Each of the seven markets has equal weight in the index except for oil, which is at half weight so its higher volatility does not unduly skew the overall picture.

The overall Volatility Spike index is the red line, which is the sum of the seven market volatilities.

There have been four major volatility spikes in the past 55 years –

-

-

- 1973-4 - oil price spike after the Yom-Kippur crisis, inflation, crashes in commercial property and share markets

- October 1987 – stock market crash, US dollar crisis

- 2008-9 – US sub-prime, global bank crisis, start of ‘ZIRP’ (Zero Interest Rate Policy), and ‘QE’ (quantitative easing)

- Early-mid 2020 – Covid lockdown crisis. This was the highest spike of all - literally off the chart because of the sharp sell-off (and just as sharp rebound) in share markets, the unprecedented failure of bond markets, and negative oil prices.

In addition, there have also been about nine smaller volatility spikes / market crises over the period. 2022 (in the Biden years) had one of those, caused by aggressive central bank rate hikes which triggered sell-offs in share markets.

These volatility spikes were sharp but very short. The 2020 Covid spike lasted just a couple of months and stock markets quickly rebounded to new highs.

Long periods of calm

In between these short, sharp volatility spikes in these crises, are long periods of relative calm. The problem is that bad news sells papers (and gets clicks) much better than good news, but most of the time it is mostly a sea of good news. During these long stretches of calm, financial media headline writers have to make up stuff because there is not much going on that actually affects markets.

Following the minor volatility spike in late 2015 / early 2016 (oil, gas, and steel bankruptcies from the commodities collapse with the China slowdown), markets were very calm through the Trump election and first term, right up until Covid hit in February-March 2020.

That calm period between mid-2016 and early 2020 included the share market sell-off in 2018 triggered by the Fed’s rate hikes. The 2018 sell-off seemed traumatic at the time, but its hard to spot on the volatility index.

That period of calm was on a par other calm periods of low market volatility– eg:

-

-

- 2003-7 calm (China/credit boom)

- 2012-4 QE calm

- 1995-7 calm - early dot-com years, Clinton boom

- 1992-3 calm – following 1990-1 recessions

‘Calm before the storm’?

It is easy to say: ‘Yes but in each case they were the calm before the storm!’. Of course they were. But the calm periods of great returns always last longer than the storms that follow!

As investors, we need to make sure we enjoy the calm, and not get spooked by endless daily chatter about impending crashes!

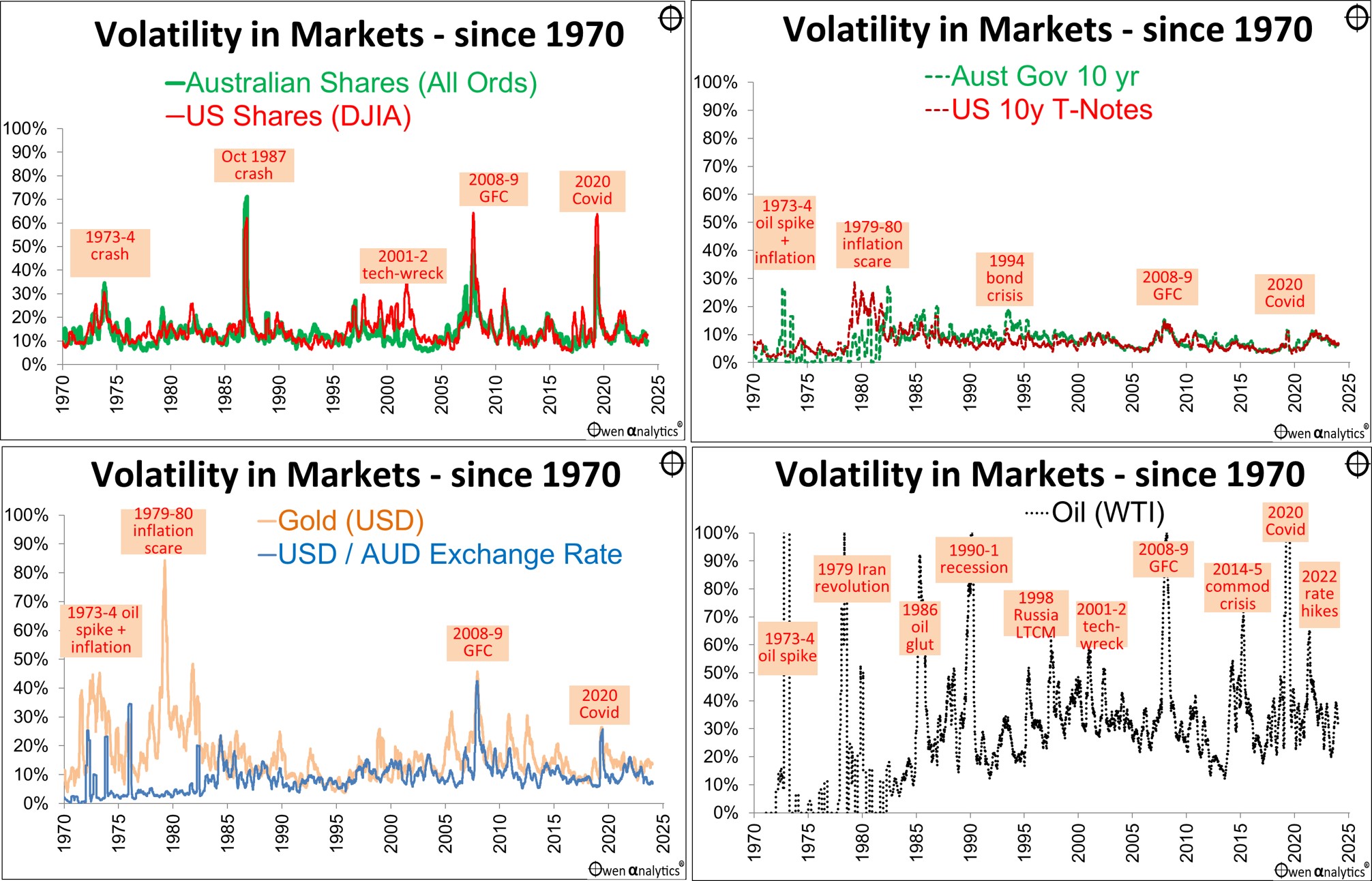

In the next charts I separate the markets to see each of them more clearly -

We can see that the big volatility spikes affected most or all of the individual markets together – because financial markets are so inter-connected.

What to expect?

Trump’s second term is sure to be just as entertaining and unpredictable has his first, and there is probably a good chance it will include another huge volatility spike like last time. But if his second term produces the same kinds of high market returns and low overall volatility as his first term – then bring it on!

‘Till next time, safe investing!

Further reading-

For a fact-based economic report card on Trump -v- Biden:

For my assessment on how Trump is facing different challenges this time -

For my most recent story -

Or visit my web-site for a wealth of fact-based articles on a wide range of relevant topics for inquisitive long-term investors.