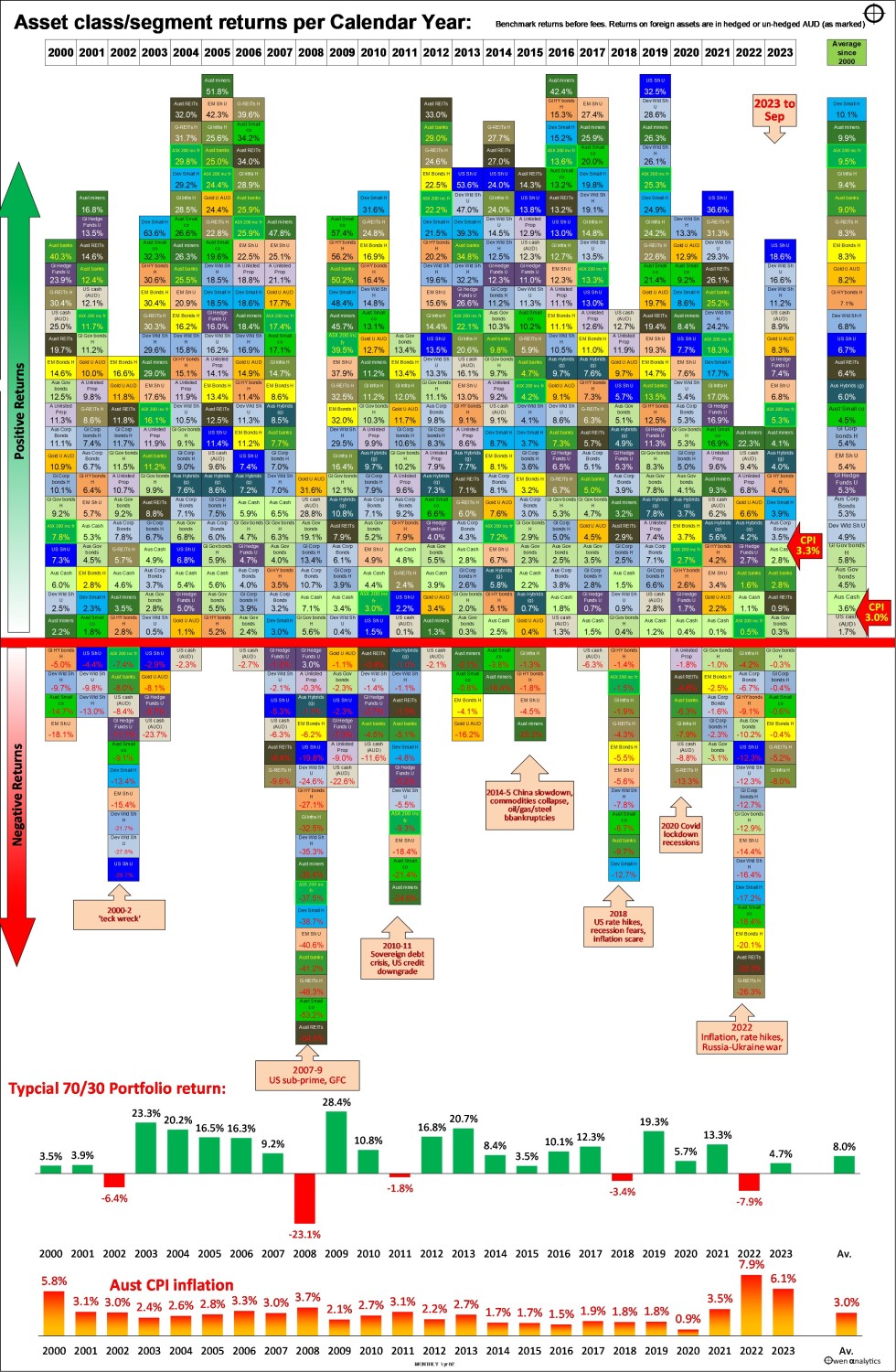

Despite constant doom and gloom in the media headlines this year, most asset classes are actually ahead in 2023. More importantly, most are ahead of inflation.

Returns from all types of assets, including cash, vary widely from year to year. All types of assets, even so-called ‘defensive’ assets go through periods of negative returns, and sometimes several negative years in a row.

Today’s chart shows total returns (i.e., including income) from two dozen of the main types of investment assets per calendar year since the start of the century. Returns above the red line are positive, below are negative.

This is designed primarily for Australian investors, so returns from international assets come in two flavors – hedged AUD, and un-hedged AUD, as marked.

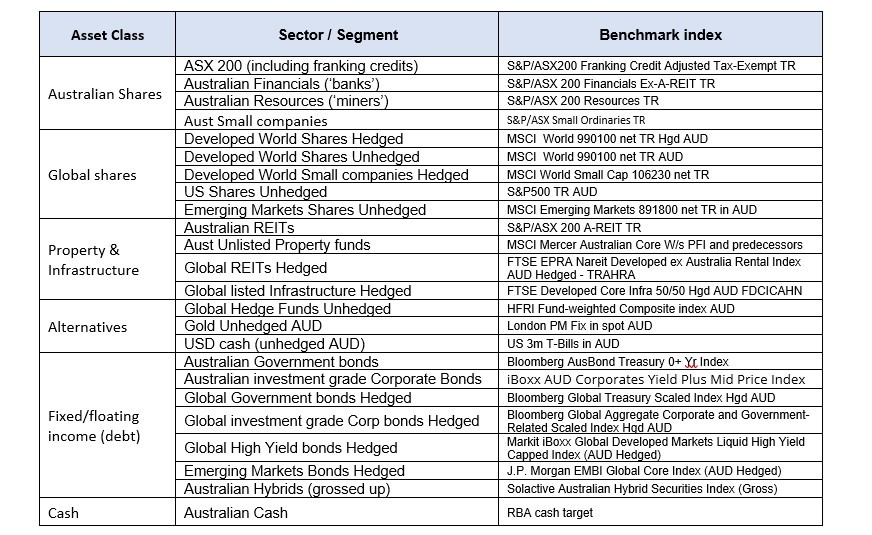

(A table of benchmarks for each asset class/segment is included at the end of this article)

Portfolios and Inflation

Below the main table are returns from a typical simple ‘70/30’ portfolio (35% Australian shares, 35% developed market shares (50% of which is FX hedged), 10% Australian bonds (50/50 government/corporate), 10% global bonds (also split 50/50 government/corporate), and 10% cash, with all holdings rebalanced yearly).

All returns are before fees, so you can deduct a fraction of a percent from returns, as all of these are available in the form of very low-cost ETFs. (Fees on passive ETFs range from around 0.05% for share ETFs, and from around 0.10% for bond ETFs).

At the bottom, we show Australian CPI inflation per year.

table of asset class returns per year since 2000

2023 score card – to end of September

Most asset classes are positive so far this year, and most are ahead of inflation (marked in red).

Although Australian CPI inflation is running at 6% on an annualized basis, it is around 3.3% for the year to date because the running rate is slowing, after peaking at 7.9% in 2022.

Inflation for the full 2023 year is likely to be in the order of 5%.

The half dozen asset classes with negative returns so far in 2023 are mainly fixed-rate bonds, REITs, and infrastructure – all of which have been hurt by rising interest rates, particularly at the long end (bond yields).

Aussie small companies have also lagged badly this year, with many being hurt by rising short-term interest rates squeezing margins, without the pricing power of many large companies.

Asset class returns since 2000

The overall table looks like a random patchwork quilt of returns, with no apparent rhyme or reason. There are different winners and losers each year, with returns from every type of asset jumping around from year to year.

Some quick observations:

- In most years, most types of investments post positive returns, and ahead of inflation.

- There are occasional years when everything is positive – like 2005, 2016, and 2019.

- But the rest of the time there are some types of assets that go backward.

- In the big bust years (like 2008 and 2022), most types of assets post negative returns.

- But even in the worst years, several asset types still manage to post positive returns, although the winners are different each time.

Most frequent HIGHEST returning assets

The asset types with the most years with the highest returns are:

- Australian miners = 5 years as the highest returning asset type, courtesy of the post-2000 China boom

- US shares (Unhedged) = 4 years – mainly in the recent tech/online boom

- Australian REITS = 3 years - mainly in the post-GFC QE years of declining bond yields

- Global REITS (hedged) = 2

- Developed world small companies (hedged) = 2

- Developed world shares (hedged) = 1

- Australian banks = 1

- Australian small companies = 1

- Emerging Markets shares (unhedged) = 1

- Emerging Markets bonds (hedged) = 1

- Australian government bonds = 1

- Gold (unhedged AUD) = 1 (2008, the year of the GFC sell-off)

- USD cash (unhedged) = 1

Most frequent LOWEST returning assets

Asset types with the most years with the lowest returns are:

- USD cash (unhedged AUD) = 8 years as the lowest returning asset type – so much for the ultimate ‘safe haven!’

- Global REITS (hedged) = 3 years – mostly in Covid lockdowns and the post-Covid inflation spike

- Australian miners = 2

- Gold (unhedged) = 2

- Emerging Markets shares (unhedged) = 1

- DM shares (hedged) = 1

- US shares (unhedged) = 1

- Global High Yield bonds (hedged) = 1

- Australian REITS = 1

- Developed world small companies (hedged) = 1

- Australian government bonds = 1

- Global infrastructure (hedged) = 1

- Australian cash = 1

Average returns since 2000

The far-right column shows average annualized returns over the period since the start of 2000.

So far this century:

- every type of asset has generated positive total returns

everything except USD cash has beaten inflation

- 1st place with the highest average total returns = Developed world small companies (hedged)

- 2nd = Australian miners

- 3rd = Australian shares (ASX200 including franking credits)

- 4th = Global infrastructure (hedged)

- 5th = Australian banks

It is notable that global corporate investment grade bonds (hedged) beat development market shares (unhedged). So too did Aussie Hybrids (grossed up). This is mainly because of the poor performance of US, European, and Japanese shares in the 2001-2 ‘tech-wreck’.

Portfolio construction

Good portfolio construction is not about trying to pick the best asset classes each year or trying to avoid the worst.

Nor is it about chasing last year's winners (hoping for a momentum effect), or last year's losers (hoping for a contrarian or reversion effect). These strategies almost always destroy wealth.

Good portfolio construction is about selecting the right mix of assets so that the portfolio as a whole has the greatest probability of achieving each investor’s long-term goals, within their tolerance for risk and volatility (ups and downs along the way), and liquidity requirements.

Inflation

To the far right of the table, we see that over the whole period, every type of asset has beaten CPI inflation, except for USD cash (in Australian dollars).

Sample portfolio returns

On the pro-forma returns from the simple 70/30 portfolio, these returns are before fees, and they assume no ‘alpha’ and no asset allocation changes, just setting the initial ‘strategic’ asset allocation and then re-balancing back to this each year.

Key outcomes for portfolios:

Overall average returns of 8.0% pa this century (before ETF fees)

- With inflation averaging 3.0% pa, this simple 70/30 portfolio would have returned CPI+5% pa, which is a typical long target return for long term ‘growth’ portfolios.

- There have been five years of negative portfolio returns this century (2002, 2008, 2011, 2018, and 2022), but four out of five of these were followed by very strong rebound years.

Asset classes and sectors, and benchmark index for each:

table of asset class benchmark indexes

We will report on full-year returns for 2023 in January.

Thank you for your time – please send me feedback and/or ideas for future editions!