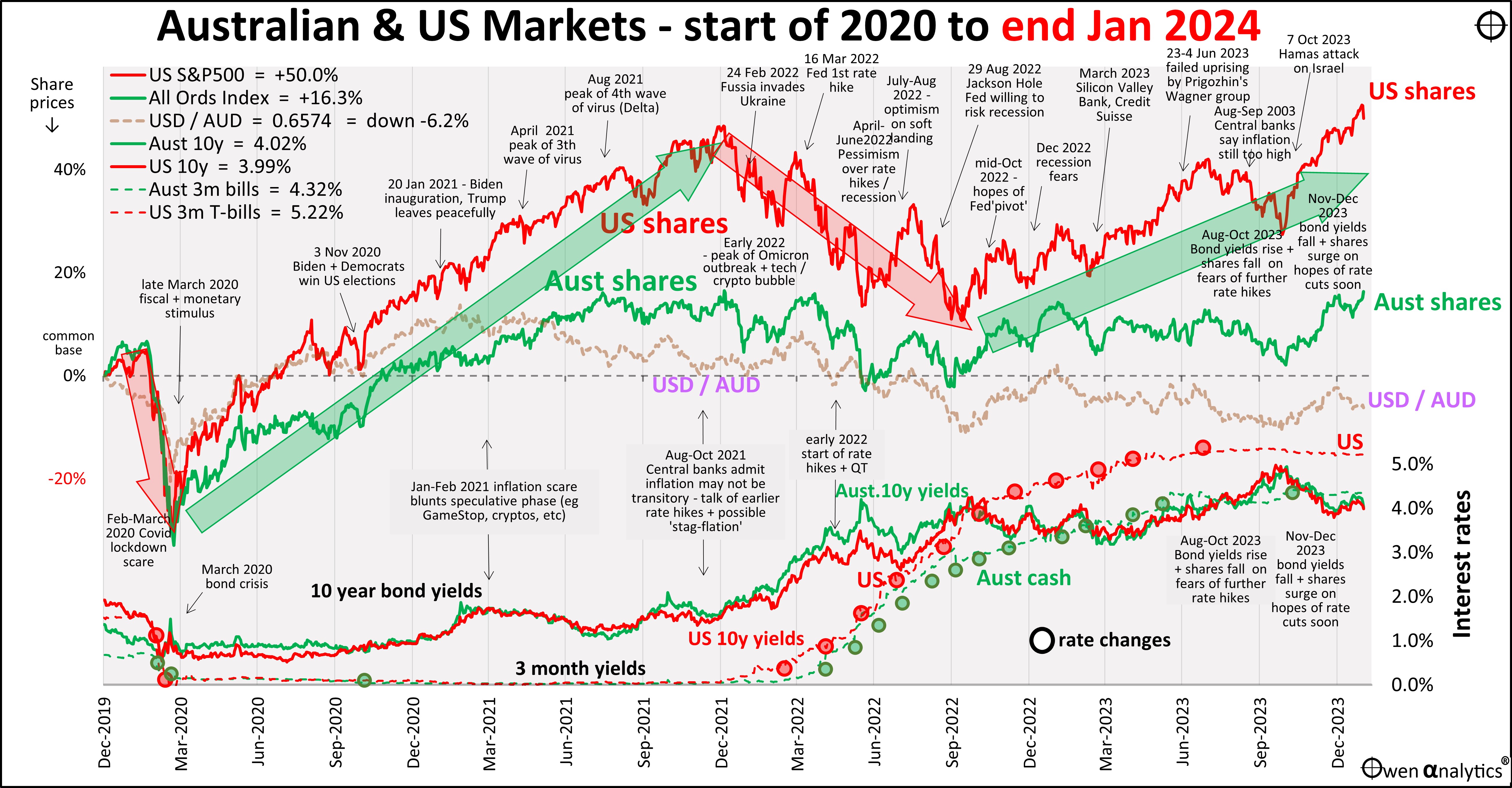

Here is my essential 1-page snapshot for Aussie investors – covering Australian and US share markets, short- and long-term interest rates, inflation, and the USD/AUD exchange rate - since the start of 2020.

There are two versions – first is the traditional version on a single chart:

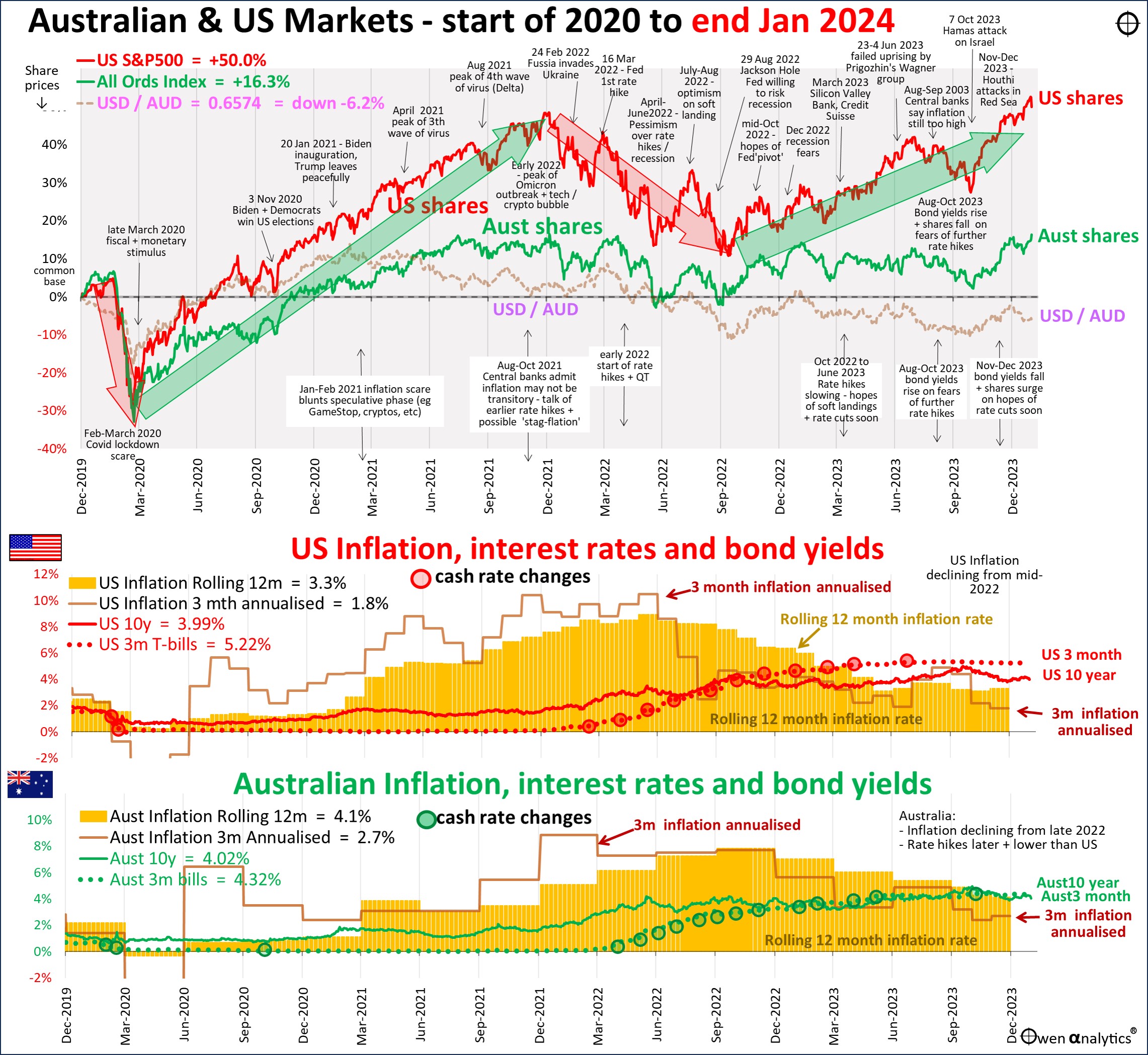

Also the alternate version requested by several advisers - showing inflation (rolling 12 month annual rate, and annualised rolling 3-months) in Australia and US -

Main developments affecting investment markets in January

The key factor affecting investment markets was inflation continuing to fall back toward target ranges. Investors continued to pile into shares on hopes of early rate cuts, despite central bankers warning that hopes of several rate cuts in the coming year were probably premature.

Our view remains that investment markets are being over-optimistic about how soon and how far cash rates are likely to fall this year. If central banks do cut rates several times in the coming months, as markets imply, it will be because of deep economic recessions. That is the only way inflation will return to zero, or below target, allowing rates to be cut.

- Most share markets were up a fraction in January (except UK and China).

- US ‘big-tech’ continued to dominate global indexes: Nvidia +24% offset Tesla down-25%, Meta/Facebook +10% (before surging another +15% on 1st Feb on the announcement of its maiden dividend), Microsoft +2%, Amazon +2%, but Apple down -5%, and Alphabet/Google flat.

- Outside of the US leaders - cyclicals were mostly down (industrials, materials, discretionary, energy), while defensive were mostly up (staples, healthcare).

- In the local Australian share market – most of the majors were up except BHP and RIO on lower iron ore prices on continued absence of big stimulus announcements from China, despite the worsening property construction/ finance crisis.

- CSL was back above $300, but still below its 2020 highs.

- Big falls for Domino’s (pizza chain), Appen (tech), Worley (oil/gas), Evolution (gold).

- On commodities markets - oil up +5%, but natural gas down -15%, and coal down -20%. Gold down -1%, iron ore down -3%, and the battery metals bubble continued to deflate.

- The federal government took two more backward steps in January. The first was reversing its election promise of implementing the ‘stage three’ tax cuts, which would have gone a long way to reduce bracket creep. The second was Workplace Relations Minister Tony Burke patting himself on the back for personally championing the militant Maritime Union’s 23% pay rise claim. Extraordinary stuff.

- Bond markets posted small rises in January, as long term yields remained more or less flat for the month, following two strong months with yields and inflation falling.

- Australian Housing – price and rents continued to rise, with buyer confidence being driven by hopes of imminent rate cuts from the RBA. There is still no sign of the much heralded ‘mortgage cliff’. We have thus far avoided a major outbreak of widespread foreclosures, but the stores of spare cash from the Covid stimulus handouts are being run down. Jobs markets remain extremely tight in Australia and the US.

- Commercial property – more cuts to prices & valuations, more funds freezing redemptions or defaulting on interest payments. REIT prices rose a fraction in January, as bond yields remained flat.

- China – Not even a Hong Kong court order to liquidate Evergrande (to try to repay US$300b in debts) was enough to convince Xi Jinping to announce major stimulus measures to rescue the collapsing property construction/finance markets. Several small measures have been announced in recent months, but nothing like the huge stimulus programs in 2009-10 or 2016-17. Meanwhile, China has become the world's biggest EV exporter, but that will not replace construction, which was once 30% of GDP during the growth years.

- In January, the Chinese government announced a fanciful economic growth rate of 5.2% for the 2023 calendar year, but it might have actually been anything between zero and -5%. Given Xi’s goal was 5%, if officials came up with anything below that, they knew they would mysteriously disappear like so many of their comrades.

- The Israel-Palestine war continued, as well as Iran-backed Houthi attacks on red sea shipping, and the conflict has also extended into red sea shipping lanes and into Lebanon. Thus far, Iran appears willing to wage war via its proxies in the region (Hamas, Hezbollah, Houthi), but remains reluctant to engage Iranian forces directly. Iran has Biden to thank for filling Iran’s coffers with oil money to fund these wars. Russia pressed on in Ukraine, assisted by an increasingly apathetic Europe and war-weary US.

- In Taiwan, the ruling anti-China Democratic Progressive Party won the January elections, but with reduced power. China had secretly brokered a coalition between the pro-China Nationalists and pro-China Taiwan People’s Party, but it was not enough to win government.

- In the US, Trump is rampaging through the Republican nominations. If he wins in November, it may pave the way for Xi to act on his plan to invade Taiwan. Meanwhile, the US is hastily building chip factories in the US, and Taiwan’s TSMC (which makes more than half of all semiconductors globally) is accelerating a shift to manufacture in Japan. Military build-ups are great for Aussie miners.

- Economic growth has remained relatively strong, but starting to soften a little in the US, Europe, and Australia – thus far defying widespread predictions of deep recessions.

- Crypto fans got a shot in the arm in January when the US SEC finally approved eleven Bitcoin ETFs in the US. Bitcoin prices surged on the news but promptly fell back to end the month square. While crypto speculators were delighted with the news, true believers were horrified as the shift to ETFs just increases the dominance of intermediaries and big finance. This goes against the whole idea of a Bitcoin market without platforms, brokers, exchanges, custodians, intermediaries, big finance, regulations, or governments.

Stay tuned for separate stories about specific topics.

Thank you for your time – please send me feedback and/or ideas for future editions!

See also:

· Australia v US share markets – it’s our turn next!

· Australian shares since 1900 – annual return pyramid

· Australia – Lucky Country for investors!