Key points:

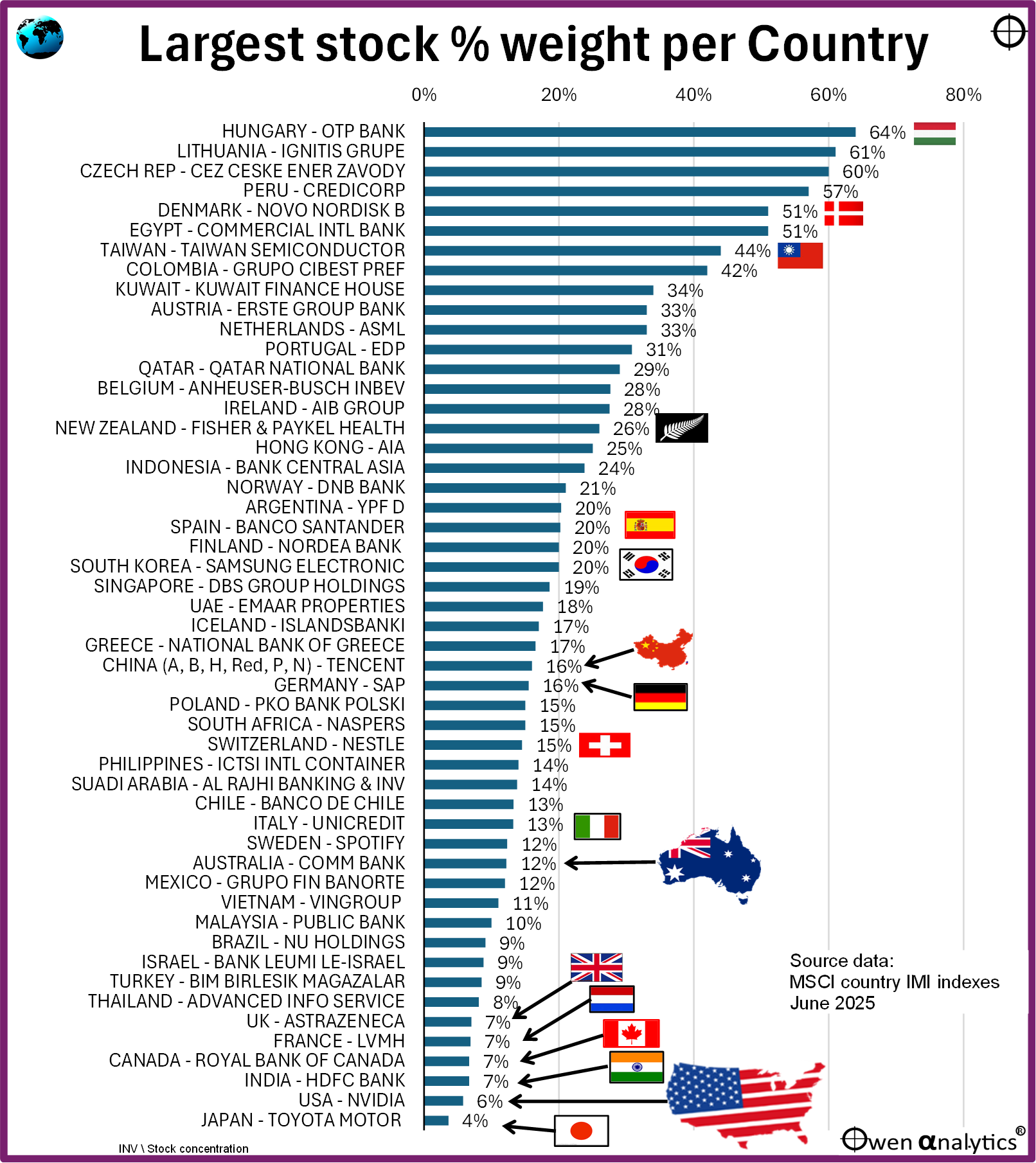

- There has been an increase in alarmist commentaries about ‘concentration’ in the US stock market. Nvidia has shot up to 6% of total US market value. But USA’s Nvidia is actually the second SMALLEST ‘largest stock weight per country’ in the world. The only country with a less concentrated stock market is Japan (with Toyota the largest stock at 4%).

- The 5 largest US stocks comprise 22% of total US market value, but there are 20 countries where more than 22% is in just ONE single stock.

- The 10 largest US stocks comprise 31% of total US market value, but there are a dozen countries where more than that is in just ONE stock.

- In Australia there is also rising concern that CBA is now 12% of the ASX market value. Actually, this is still relatively low, and not my major source of concern.

- What concerns me is NOT the ‘concentration’, but the excessive VALUATIONS, and over-confidence that earnings and dividends will rise to justify the current lofty prices. When (not if) the US bubble bursts, it will drag down the rest of the US market (and economy), and every other stock market, just like in past over-valuation cycles.

How country share markets stack up on weight of their largest single stock

Here are the 50 largest country stock markets in the world – ranked in order of the percentage weight of the largest single stock relative to the overall market value per country:

Apart from the fact that USA is way down at the bottom of the chart – with second least concentrated stock market in the world, my initial observation when I did this exercise today is the sheer number of countries in which banks are the largest listed company.

Banks don’t actually do anything apart from shuffle money around, and charge fees at every turn. Generally, ‘emerging’ or ‘developing’ markets (which are mostly raw commodities exporters that add no value, and are at the mercy of global commodities markets) tend to be the countries where banks are their main stocks. (Australia – this is you!)

US of A

This is where the media are panicking the most. The largest five US stocks now make up 22% of the total US listed market value. Shock – Horror! That may sound like a lot, but there are actually twenty other countries where more than 22% is in just the largest SINGLE dominant stock.

The largest 10 US stocks make up 31% of the total US market value, but there are a dozen countries where more than that is in just the one largest single stock.

The US is the second LEAST concentrated stock market in the world!

Rest of the world

Outside of the US, many of the largest stocks in each country are household name companies that dominate their industries globally. For example –

- Spotify in Sweden,

- Novo Nordisk (insulin and Ozempic) in Denmark,

- Tencent (WeChat, QQ, etc) in China,

- Taiwan Semiconductor (largest producer of computer chips globally) in Taiwan,

- Samsung Electronic in South Korea,

- ASML (specialist semiconductors) in Netherlands,

- Anheuser-Busch (Budweiser beers, etc) in Belgium,

- Nestlé in Switzerland.

In most cases, the sheer size of these global giants tends to over-shadow what's going on in other companies on their local stock markets.

In contrast, the US stock market is home to dozens of global household name companies beyond the 'Mag-7' giants. Companies like Visa, Mastercard, American Express, Johnson & Johnson, McDonalds, Coca-Cola, Starbucks, Nike, Cisco, Salesforce, Exxon Mobil, Chevron, Walt Disney, Boeing, Pfizer, Merck, Chubb, Colgate Palmolive, PayPal, Moody's, S&P, Motorola, Air BNB, FedEx, UPS, Phillips, Uber, 3M, Hilton Hotels, Marriott, Ford, eBay, Carnival Cruises, Hewlett Packard, Kraft Heinz, and countless others.

Not only is the US stock market the second least concentrated, it is the broadest and deepest stock market in the world.

What worries me

So-called ‘concentration’ of the US market does NOT concern me. What does worry me is the astronomical VALUATIONS, and the level of over-confidence that earnings and dividends (yes cash dividends!) will rise to justify their lofty prices.

When (not if) the US over-valuation bubble bursts, it will drag down the rest of the US market (and US economy), and also every other stock market around the world, just like in every past over-valuation bubble.

The current US tech bubble is actually only around half as over-priced as the late 1990s ‘dot-com’ bubble, which ended with the 2000-2 ‘tech-wreck’, which dragged the rest of the US market down (and every other stock market in the world), and caused a general US and global recession.

However the daddy of all concentration/over-priced bubbles was ultra-bubble stock NTT in the Japanese market at the end of 1989. 35 years later and we are still waiting for a recovery from that one!

I personally have remained bullish on US/global shares in my own long-term portfolios, and in advised portfolios. But the time for shifting to a more cautious stance is certainly getting closer!

Australia and CBA

The local media here in Australia have also had a field day over the past year, milking the self-created hysteria over the rise and rise of our largest ASX stock, the Commonwealth Bank of Australia (CBA).

(Personally, I am horribly overweight Aussie bank shares, mostly bought in the early-mid 1990s. I have not bought any more bank shares since the emergency deep-discounted GFC capital raisings in 2009.)

Unlike the US tech giants, CBA is the opposite of a ‘growth stock’. Its a century-old dinosaur from a bygone era. Its asset growth rates and returns on equity have been declining for 25 years. Earnings per share and dividends per share have fallen in real terms over the past decade, but CBA has more than doubled in market value to 12% of the ASX. It is horribly over-priced on any number of metrics.

For my take on CBA see – CBA in 7 charts – the ‘Steven Bradbury’ of Australian banking – now suddenly a ‘growth stock’? (29 July 2024)

What to do?

Fortunately, there are plenty of ways to adjust portfolios to reduce exposures to over-priced stocks and sectors using low-cost ETFs:

-

-

- Size ETFs (mid-caps, small caps)

- Equal -weighted ETFs

- Fundamentally-weighted ETFs

- ‘Factor’ ETFs (eg Quality, Value, Yield, etc)

- Sector ETFs

Ok – time to get back to my end-of-financial-year review of my own investments, and writing up my quarterly reports for Investment Committees.

'Till next time - safe investing!